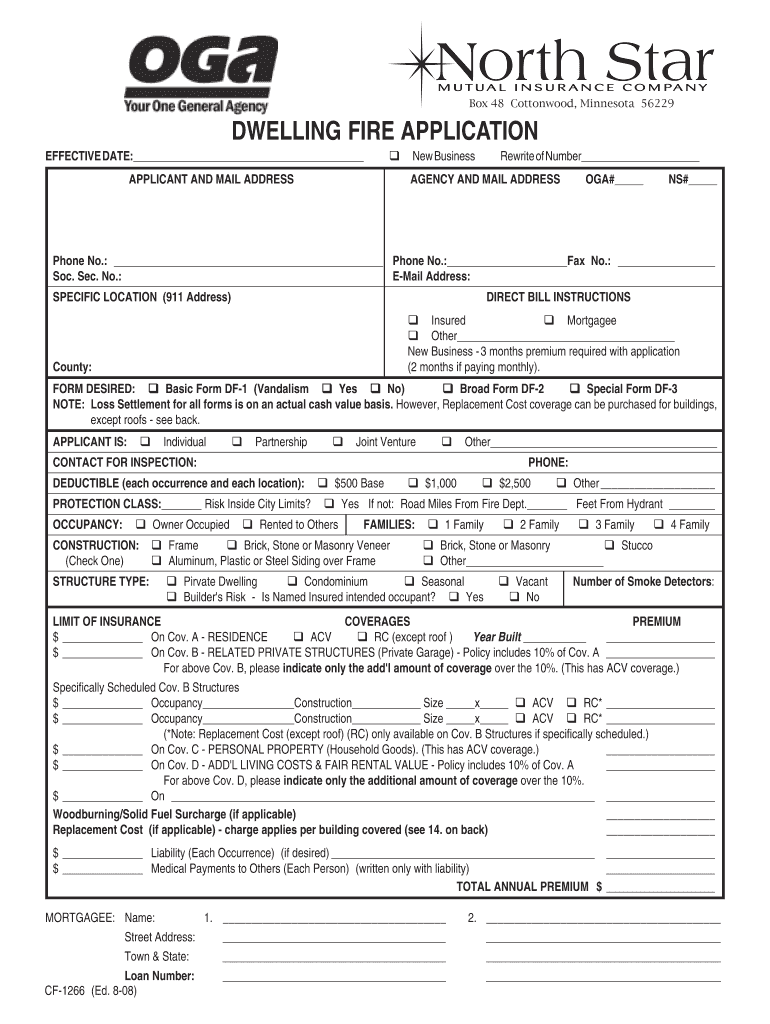

Definition and Purpose of the Dwelling Fire Application

The Dwelling Fire Application is a specialized form used to apply for dwelling fire insurance coverage. This type of insurance is essential for property owners and landlords looking to protect their real estate assets from risks such as fire, smoke, and other specific perils. Unlike a standard homeowners insurance policy, the dwelling fire policy is more focused and often selected for properties that may not qualify for conventional homeowners insurance. It is particularly beneficial for rental properties, seasonal homes, and older residences.

Detailed Coverage Options

- Dwelling Coverage: Protects the physical structure of the home against risks covered under the policy.

- Other Structures Coverage: Includes additional buildings on the property like detached garages or sheds.

- Loss of Use or Rent: Provides coverage for lost rental income if the property is uninhabitable due to a covered loss.

The application's primary purpose is to collect comprehensive information from the applicant to determine eligibility and define the terms of the insurance policy.

How to Use the Dwelling Fire Application

Understanding the Sections

Applicants should familiarize themselves with the various sections of the application to ensure they provide accurate information:

- Personal Information: This section requires the applicant's full name, contact details, and identification number.

- Property Details: Includes the property's address, type, use, and building characteristics such as age and construction materials.

- Coverage and Limits: Applicants must specify the desired coverage limits and any additional endorsements they wish to include.

- Loss History: A record of previous insurance claims related to the property, which helps underwriters assess risk.

Tips for Accurate Completion

- Use the fillable PDF version available online for clarity and ease of submission.

- Ensure all fields are filled out completely; incomplete applications can delay processing.

- Double-check all personal and property details before submission.

Steps to Complete the Dwelling Fire Application

Step-by-Step Instructions

- Prepare Necessary Documents: Collect documents such as current insurance policy details, property tax records, and previous loss history.

- Fill Personal and Property Information: Complete the first sections focusing on applicant and property details.

- Specify Coverage Needs: Indicate required coverage amounts and any additional policy features.

- Review Loss History: Provide accurate details of any past claims or damage incidents.

- Finalize and Submit: Verify information for accuracy, sign the application, and submit to your insurance provider through your preferred channel.

Each step is crucial to ensure a smooth application process.

Important Terms Related to the Dwelling Fire Application

Understanding key terms within the application is vital for clarity and correct completion:

- Endorsement: Additional coverage or modifications to the original policy.

- Peril: Specific risks covered by the insurance, such as fire or theft.

- Exclusion: Items or conditions not covered by the policy, which vary based on the insurance provider.

These terms help applicants better understand their coverage and responsibilities.

Legal Use of the Dwelling Fire Application

Compliance and Binding Agreements

- Dwelling fire applications, once completed and submitted, form a legal contract between the insurer and the insured.

- All information provided must be accurate and truthful to avoid future disputes or claim denials.

Understanding the legal implications ensures applicants are aware of their rights and obligations.

Key Elements of the Dwelling Fire Application

Critical Information to Include

- Applicant Details: Full legal name, contact information, and social security number.

- Property Address: Exact location including ZIP code.

- Insurance Details: Previous insurance history and any existing policy numbers.

- Requested Insurance Types: Clearly defined levels of desired coverage.

Each element is critical in assessing the risk and underwriting the policy accurately.

State-Specific Rules for the Dwelling Fire Application

Insurance regulations can vary significantly from state to state within the United States. Therefore, applicants should:

- Consult state regulations for any specific mandates that affect the application or coverage options.

- Consider local nuances such as regional risks or historical property regulations that may impact coverage.

Understanding these distinctions can influence an applicant's coverage choice and premium costs.

Required Documents for the Dwelling Fire Application

To ensure an efficient application process, applicants must gather and submit several key documents along with their application:

- Proof of Property Ownership: Deeds or mortgage documentation.

- Current Insurance Policy: If applicable, provide details of existing coverage.

- Appraisal or Tax Assessment: Confirms the property's value.

- Loss History Reports: Documents detailing any claims made in the past.

Supplying these documents accurately helps expedite the approval and underwriting process.