Understanding the 2024 Form 593 Real Estate Withholding Statement

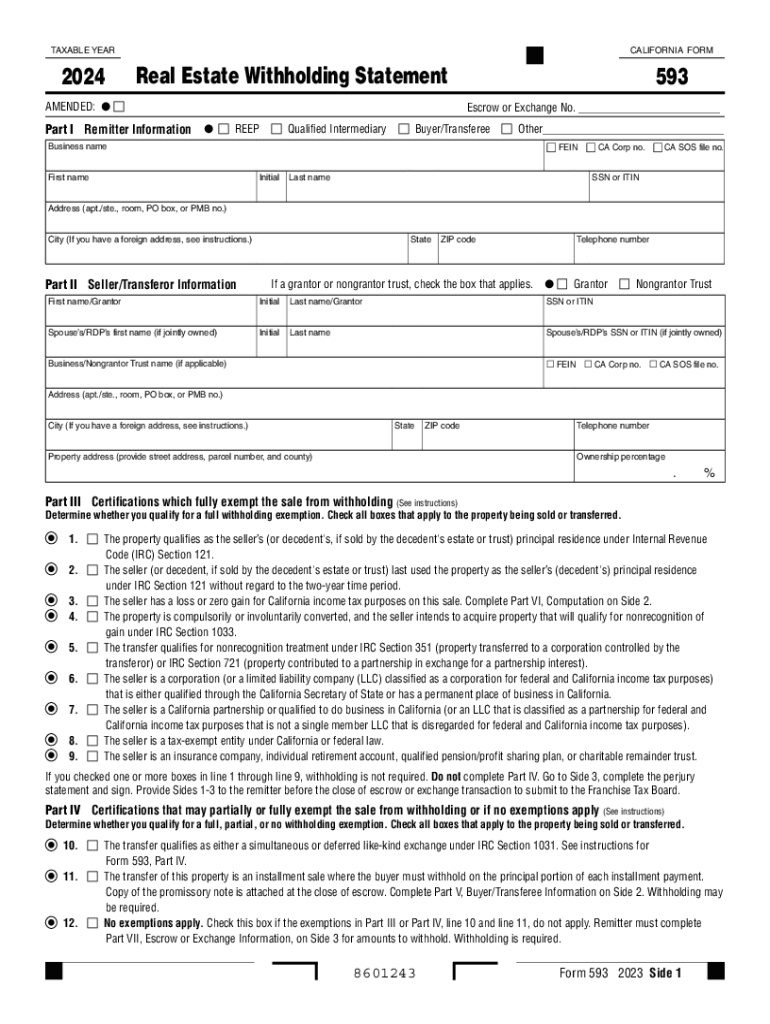

The 2024 Form 593, known as the Real Estate Withholding Statement, is used for reporting and withholding California state taxes on real estate transactions. This form requires detailed information from both the remitter (usually the buyer) and the seller/transferor in a property transaction. The goal is to ensure compliance with California's withholding requirements, which help in collecting taxes upfront from real estate sales.

- Real Estate Transaction Context: Any time real estate changes hands in California, this form generally comes into play. It captures details like the property address, transaction value, and withholding amounts, aiding the California Franchise Tax Board (FTB) in tax collection.

- Withholding Compliance: For sellers, this form is crucial for demonstrating that the correct amount of tax withholding is calculated and reported. This not only prevents future tax disputes but also ensures the state's tax collections are accurate.

Key Components Required in Form 593

Form 593 requires meticulous detailing across several sections to ensure both taxpayer and government requirements are fulfilled:

- Seller and Buyer Information: Fields for seller and buyer names, ID numbers, and contact details.

- Property Details: Specifics about the property involved, including the address and Assessor’s Parcel Number (APN).

- Withholding Calculation: Includes sections that guide users through the withholding tax calculations based on the sale price and applicable exemptions.

- Exemption Certifications: It's crucial to identify whether full or partial exemptions apply, such as if the seller is a government entity.

Eligibility Criteria and Exemptions

Certain parties involved in a real estate transaction may be exempt from withholding requirements:

- Exempt Entities: These include government bodies, and some institutional or corporate sellers.

- Homeowner Exemptions: Sellers who qualify as residents of California may claim reduced or no withholding. Documentation is vital to prove eligibility, often requiring additional attachments to Form 593.

Step-by-Step Completion of the Form 593

Completing Form 593 involves several precise steps:

- Gather Required Information: Before you begin, ensure you have all necessary information, including personal identification numbers and property details.

- Fill Out Seller Information: Start with the seller's details, ensuring accuracy to avoid processing delays.

- Enter Buyer/Transferee Details: This section collects buyer-related information and is crucial for completing transaction details.

- Calculate Withholding Amounts: Use the provided calculation guidelines to determine the correct withholding amount based on the sale price and applicable exemptions.

- Review and Sign: Once filled, the form should be reviewed meticulously for errors, signed by the parties involved, and filed according to state deadlines.

Legal Implications and IRS Guidelines

The Form 593 aligns with broader legal responsibilities governed by both state and federal tax codes:

- IRS Coordination: While primarily a state form, aligning the reported details with IRS requirements helps prevent federal tax issues. The form's details must match those provided in IRS filings to ensure coherence and accuracy.

- Legal Compliance: Failure to withhold the correct amount or file the form properly can result in penalties. Legal consultation might be necessary for complex transactions to ensure full compliance and avoid liabilities.

Common Use Cases of the Form 593

Typical scenarios where the Form 593 is used include:

- Residential Sales: Owners selling their primary residence.

- Investment Property Transfers: Involves sales between investors, often in corporate or partnership formats.

- Partial Ownership Transfers: Sales involving fractional property interests, where specific calculations for the withholding share are necessary.

Important Filing Deadlines for Form 593

Form 593 must adhere to strict state-imposed deadlines:

- Timely Submission: The form should be submitted when the sale closes. State specifics can vary, but generally, it's expected very soon after transaction completion.

- Annual Reporting: Even if no withholding applies, the form serves as part of the year's tax filing requirements, requiring the same adherence to tax timelines as regular income tax filings.

Software and Platform Compatibility

Completing Form 593 can leverage digital platforms and software:

- DocHub and California Franchise Tax Board Compatibility: Specifically supports electronic completion and submission, aligning with tax software used by professionals.

- Integration with Tax Filing Software: Systems like TurboTax and QuickBooks can aid in filing Form 593. These programs can import necessary data, easing the completion process.

Understanding and accurately completing the 2024 Form 593 Real Estate Withholding Statement is essential for ensuring compliance with California's tax regulations. Whether digital or paper, correct filing helps mitigate legal risks and ensures a smooth real estate transaction process.