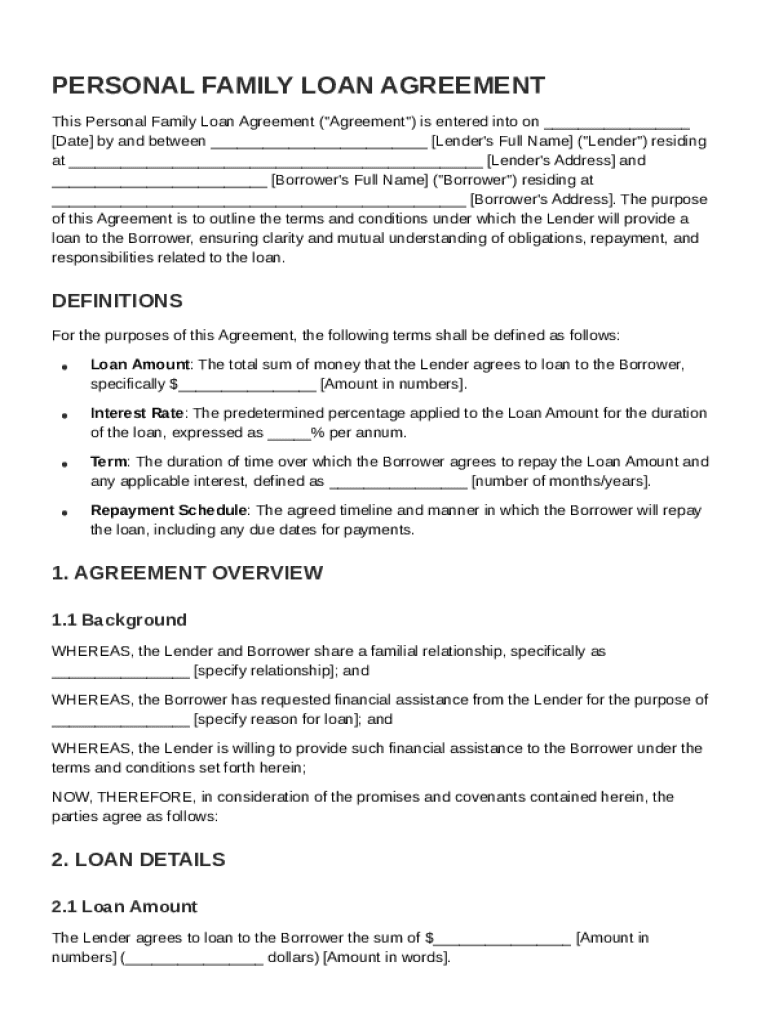

Definition & Understanding of a Personal Family Loan Agreement

A Personal Family Loan Agreement, also known as a family loan contract, is a legal document that defines the terms and conditions agreed upon by family members in the lending and borrowing of money. It typically outlines critical components such as the loan amount, interest rate, repayment terms, and any consequences associated with defaulting on the loan. This agreement ensures clarity and helps maintain trust, as it legally binds both parties to their commitments.

Family loan agreements serve to mitigate potential misunderstandings and disputes, promoting financial accountability between relatives. By providing a structured format, they facilitate open conversations about financial transactions within a family setting. This document is particularly useful when significant sums of money are involved, where either party might benefit from legal protection or clarity in financial obligations.

Examples of Using the Personal Family Loan Agreement Template

Real-world scenarios illustrate the importance of employing a Personal Family Loan Agreement. Consider a family situation where one sibling wishes to support another by lending money for a house down payment. By utilizing the agreement, the lender and borrower benefit from a formalized framework which can help preserve their sibling relationship by preventing future disagreements regarding repayment.

Another example could involve parents lending money to their children to support higher education expenses. By specifying repayment terms and conditions in the agreement, parental lenders can help their children feel responsible for managing their acquired debt while still providing support.

Key Elements of the Personal Family Loan Agreement

The core elements of a Personal Family Loan Agreement are designed to foster transparency and ensure legal soundness. Critical components of this document include:

- Loan Amount: The total sum of money being lent to the borrower.

- Interest Rate: Any interest applicable to the loan, set by mutual agreement.

- Repayment Schedule: The timeline for payments, including due dates, installment frequency, and amounts.

- Consequences of Default: Defined penalties or actions if the borrower fails to meet the repayment terms.

- Signatures: Legal authorization by both parties, confirming the agreement's terms.

Additional considerations can include early repayment options, co-signers, or amendments to the initial terms. Making these elements explicit provides more robust legal validation and aids in smoothly managing the financial relationship.

Important Terms Related to the Personal Family Loan Agreement

Understanding key terminologies within the context of a Personal Family Loan Agreement enhances comprehension of legal obligations. Important terms include:

- Promissory Note: A written commitment by the borrower to repay the loan.

- Lender: The individual providing the loan.

- Borrower: The person receiving the loan.

- Principal Amount: The original loan amount before any interest.

- Amortization: The process of spreading the loan payments over a period of time.

- Collateral: Any asset pledged as security for loan repayment.

Grasping these terms ensures a shared understanding, laying the groundwork for informed agreement on terms and fostering clear communication between parties.

How to Use the Personal Family Loan Agreement Template

To effectively use the template, first gather information and consider mutual terms for the agreement. Follow these steps for successful utilization:

- Discuss Terms: Both parties should engage in an open discussion to determine all relevant aspects such as loan amount and repayment timeline.

- Draft the Agreement: Fill in the necessary details in the loan template, ensuring it reflects all agreed terms.

- Review for Accuracy: Carefully review the agreement to confirm that all data is precise and no details are omitted.

- Sign the Document: Both parties should sign the completed agreement to signify their commitment.

- Record Keeping: Ensure both the lender and borrower retain copies for personal records and future reference.

These steps help in formalizing the loan agreement, ensuring due diligence, and providing legal credence to the arrangement.

Who Typically Uses the Personal Family Loan Agreement Template

The typical users of a Personal Family Loan Agreement template are family members seeking to formalize a borrowing arrangement between them. This can include parents and children, siblings, or extended family members wishing to support one another financially.

The document is especially valuable when providing substantial financial support, such as for education costs, real estate investments, or starting a business. The template removes ambiguity and equips family members with legal backing, thereby supporting stronger financial agreements that safeguard relationships.

Legal Use of the Personal Family Loan Agreement Template

The legal enforceability of a Personal Family Loan Agreement is a powerful tool in safeguarding personal loans. To ensure its legal standing in the United States, the document should include:

- Clear documentation of agreed interest rates aligning with applicable state usury laws.

- Full identification of both lender and borrower with valid signatures.

- Comprehensive terms that abide by state regulations and tax implications governed by the Internal Revenue Service (IRS).

Failing to adhere to legal stipulations can render the agreement void or expose parties to legal disputes. Clarity in legal terms and adherence to local laws enable a robust and enforceable contract that is respected in court, if required.

Steps to Complete the Personal Family Loan Agreement Template

Completing the Personal Family Loan Agreement entails specific stages to ensure a thorough and legally binding document:

- Preparation: Collect all parties' information and agree upon all vital loan details, such as amount and interest rate.

- Template Customization: Use the template to personalize sections with specific loan details pertinent to the agreement involved.

- Checking Compliance: Validate that terms reflect state laws and IRS guidelines concerning interest rates and loan documentation.

- Execution: Sign the document with witness or notarization if required for enhanced legal defensibility.

- Distribution: Each party should maintain a signed copy for their records to ensure reference and accountability.

Executing these steps reinforces the legality and clarity of the familial loan, protecting all parties' interests involved.