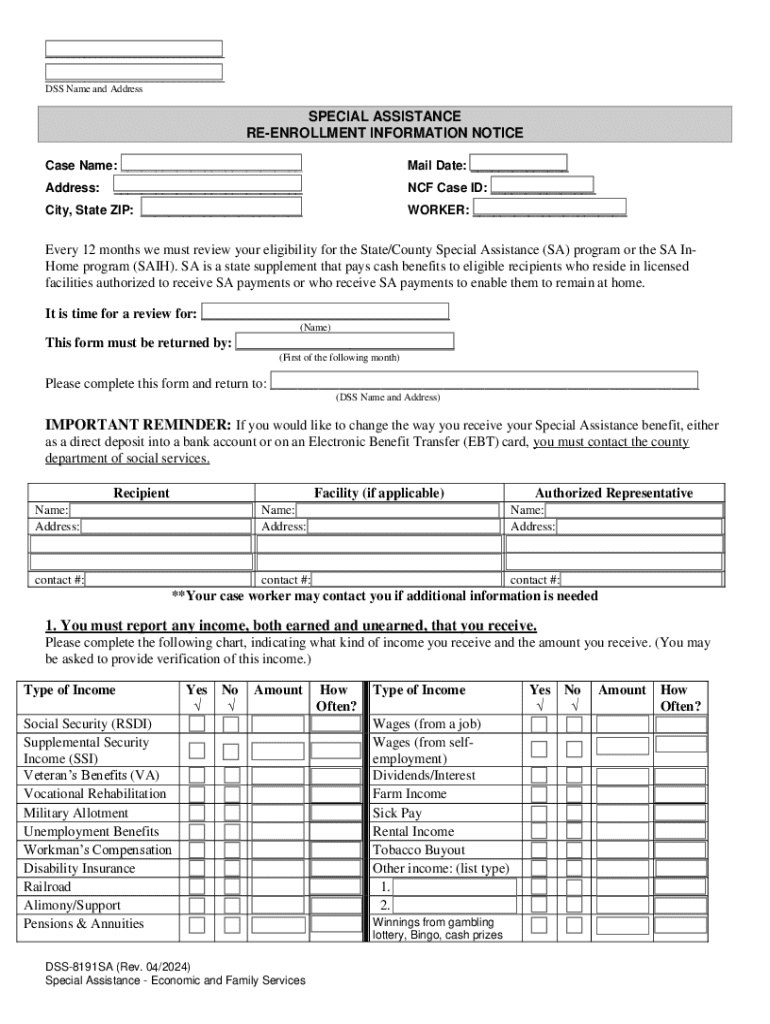

Definition and Meaning

Understanding the phrase "you must report any income, both earned and unearned," is essential for comprehending certain forms, particularly in the context of tax returns and financial disclosures. Earned income refers to wages, salaries, commissions, and tips acquired through employment or self-employment. Unearned income includes interest, dividends, rental income, and other passive sources. This comprehensive statement mandates that individuals must disclose all sources of income, regardless of their nature, in specific documentation, such as tax forms or benefit applications, to comply with legal and financial obligations.

Why Should You Report All Income

Reporting all income, both earned and unearned, is crucial for maintaining compliance with federal and state regulations. These regulations ensure that individuals are taxed appropriately, based on their total earnings. Failure to report income can lead to inaccuracies in tax filings, resulting in potential penalties, fines, or audits from the IRS. Moreover, comprehensive reporting is essential when applying for financial aid programs, loans, or governmental assistance, as inaccurate income disclosure can affect eligibility and benefit determinations.

Steps to Complete Income Reporting

- Collect Income Documentation: Gather pay stubs, W-2 forms, 1099 forms, bank statements, and other documents that record income.

- Identify Income Sources: Categorize your income into earned and unearned to align with reporting requirements.

- Complete Required Forms: Fill out the necessary sections of tax forms or financial disclosures that require income reporting.

- Review Entries for Accuracy: Ensure all income figures are accurate and reflect current earning statuses before submission.

- Submit Forms by the Deadline: Ensure that all forms are filed by stipulated deadlines to avoid penalties and ensure compliance.

Accuracy in Reporting

- Double-Check Figures: Always verify calculations and figures to maintain precision across all forms.

- Use Tax Software: Employ tax software like TurboTax or QuickBooks for guided assistance in accurately reporting all income sources.

- Professional Assistance: Consider hiring a tax professional or accountant for complex income situations or if assistance is needed in categorizing income properly.

Key Elements of Income Reporting

- Earned Income: This includes all wages from employment or self-employment activities. Ensure accurate reporting of all job-related income.

- Unearned Income: Encompasses interest, dividends, rental profits, and more. Documentation should reflect all non-work-related earnings.

- Documentation Requirements: Maintain organized records of all income-related documents for reference during filing.

- Disclosure Requirements: Compliance mandates full disclosure of all income sources, without omission or understatement.

IRS Guidelines for Income Reporting

The IRS sets forth clear guidelines regarding the reporting of income. Individuals must include all forms of income, both domestically and internationally derived, in their federal tax returns. The IRS also provides resources to help taxpayers determine which forms apply based on their financial activities, ensuring that all income is declared appropriately. Adhering to these guidelines is paramount to avoid legal repercussions and to guarantee accurate tax assessments.

Filing Deadlines and Important Dates

Taxpayers must adhere to specific filing deadlines to avoid penalties. For most individuals in the United States, tax returns must be filed by April 15. However, extensions may be requested, granting additional time to compile necessary documents and information. It’s important to also consider state-specific deadlines, which may differ from federal dates, ensuring complete compliance on a state and federal level.

Penalties for Non-Compliance

Failing to report total income can result in severe penalties, including fines, interest charges, and legal action. The IRS assesses penalties based on the degree of non-compliance and the amount of unpaid taxes. Furthermore, deliberate underreporting of income can be classified as tax evasion, which carries more serious consequences, including potential imprisonment. Ensuring full and honest disclosure of all income is essential to prevent these negative outcomes.

State-Specific Rules for Income Reporting

Each U.S. state may have its own regulations and nuances regarding income reporting. Taxpayers must be familiar with both federal and state income tax laws to ensure full compliance. Some states have different ratios for earned versus unearned income taxation, or particular deductions and credits, making it necessary to understand how these differences might impact their total tax liability.

Detailed Scenarios

- Residents in States with No Income Tax: Consider how they must still comply with federal requirements.

- States Offering Specific Credits or Deductions: Analyze regional advantages that may affect overall tax strategy.

Examples of Using Income Reporting

Consider a self-employed individual who earns additional income through rental properties. This taxpayer must report all earnings from both sources to remain compliant. Utilizing tax software can simplify this process by guiding users through necessary steps and ensuring that all income is adequately disclosed. Similarly, a student receiving a scholarship that includes a taxable portion would need to understand how to report that income accurately.

Digital vs. Paper Version of Reporting

Modern income reporting offers taxpayers the flexibility to choose between digital and paper submission methods. Electronic filing through platforms like e-File or IRS Free File facilitates speedy processing and immediate confirmation of submission. However, some individuals may prefer traditional paper submissions due to comfort or accessibility. Both methods require thorough attention to detail to ensure accuracy, regardless of the format chosen.

Who Issues the Form

Various government bodies, most notably the IRS, are responsible for issuing forms related to income reporting. These forms, such as the 1040 series for individual tax returns, are pivotal for taxpayers detailing their earnings. Understanding which forms apply to one's personal financial situation is critical for proper completion and submission.