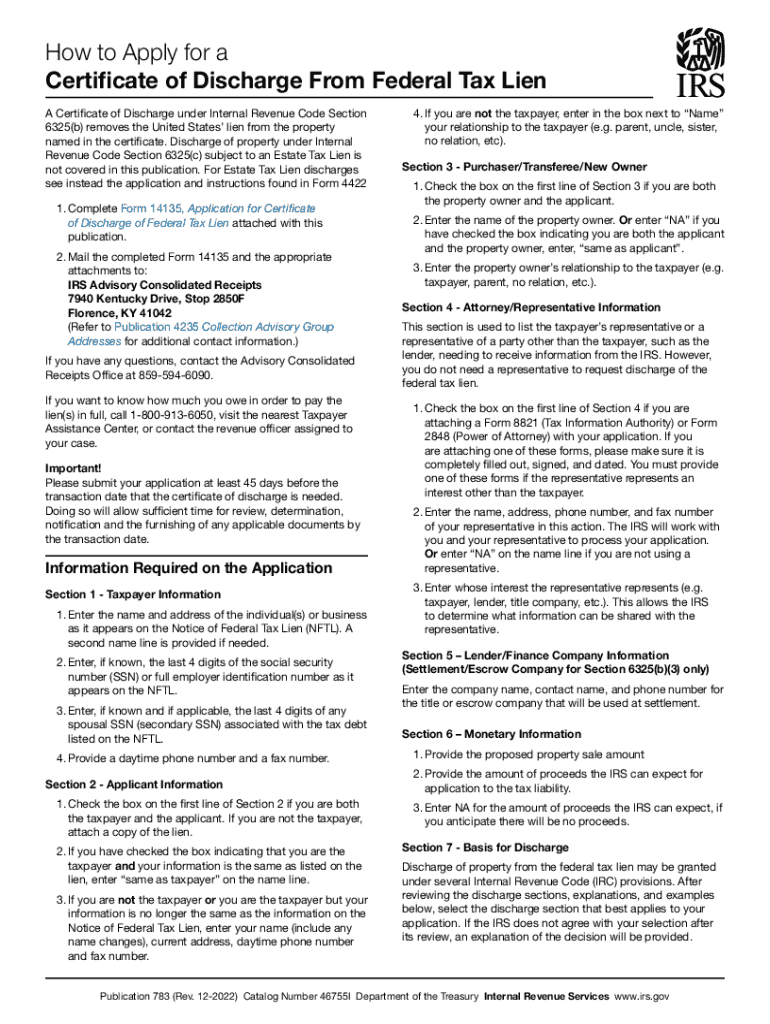

Understanding the Application for Certificate of Discharge of Federal Tax Lien

The Application for Certificate of Discharge of Federal Tax Lien is a formal document submitted to the Internal Revenue Service (IRS) to request the release of a federal tax lien from a specific property. Under Internal Revenue Code Section 6325, this application is utilized when a taxpayer wants certain property released from the lien's burden, which may enhance their ability to sell or refinance a property. Understanding the nuances of this application is essential for taxpayers looking to manage or mitigate the effects of a federal tax lien on their assets.

Definitions and Terms

- Federal Tax Lien: A legal claim by the government on a taxpayer's property due to unpaid tax debts.

- Certificate of Discharge: A document issued by the IRS that frees specific property from a federal tax lien.

- Discharge Provisions: Specific conditions under which the IRS may grant a discharge, such as the sale of the property with proceeds going to the IRS.

Steps to Complete the Application

Completing the Application for Certificate of Discharge of Federal Tax Lien involves a systematic approach to ensure all necessary information and documentation are correctly provided. Below is a detailed guide on filling out the application form:

-

Gather Required Information:

- Taxpayer identification number.

- Details of the federal tax lien, including its identification number.

- Description and value of the property subject to the discharge request.

-

Complete the Form:

- Fill out personal and property details accurately on the application form.

- Specify why you seek the discharge and under which discharge provision your request falls.

-

Obtain Necessary Documents:

- Appraisals, sales agreements, or escrow instructions if applicable.

- Proof of other liens or encumbrances on the property.

-

Mail the Application:

- Send the completed application, along with all attachments, to the appropriate IRS office as instructed. Ensure you retain copies for your records.

Common Errors to Avoid

- Incomplete information or incorrect tax lien identification numbers can delay processing.

- Failing to include necessary supporting documents, such as appraisals or legal agreements.

Purpose and Use Cases for the Application

The primary purpose of the Application for Certificate of Discharge of Federal Tax Lien is to enable the unencumbered sale or transfer of property tied to a federal tax lien. Here are some scenarios where the application is critical:

- Property Sale: A taxpayer wants to sell property but needs to discharge the lien to clear the title for buyers.

- Refinance Opportunities: To refinance a mortgage, clear title and release of lien may be required.

- Improving Cash Flow: Releasing liened property can provide liquid assets to settle tax debts.

Eligibility Criteria and Approval Process

Not all properties or situations qualify for a discharge. Eligibility is determined based on specific criteria outlined by the IRS:

- Sufficient Payment to IRS: Proceeds from the sale of the property must adequately cover the tax owed, or other arrangements may suffice.

- Existence of Funds in Escrow: Funds may be held in escrow for settlement if immediate full payment is not possible.

Approval Timeframe

Approval can vary but typically might take several weeks to months. The timeframe largely depends on the complexity of the application and the timely submission of all required information.

Filing Deadlines and Important Dates

Timely filing is essential to avoid delays in the discharge process:

- Submit at least 45 days before the proposed sale or transfer of the property.

- Be aware of federal holidays or tax deadlines that could extend processing times.

Legal Implications of the Certificate

Obtaining a Certificate of Discharge is a legal relief mechanism that affects both current and future asset management:

- Title Clearances: Essential for any legal transfer of property where liens are involved.

- Potential Penalties: Misrepresentation or late submission may lead to penalties or rejection of the application.

Comparing Digital and Paper Submissions

The IRS allows both digital and paper submissions for the Application for Certificate of Discharge of Federal Tax Lien, each with its pros and cons:

- Digital Submission: Faster processing, immediate confirmation, and reduced mailing costs.

- Paper Submission: May benefit those who prefer traditional documentation or lack digital access.

Each submission method is designed to accommodate a wide range of taxpayer needs, ensuring broad accessibility for all applicants.

State-Specific Rules

Federal tax liens are nation-wide, but certain states may have additional rules or considerations regarding property and lien management:

- State Notification Requirements: Some states require notification of local tax authorities.

- Additional Recordings: Certain states require additional lien satisfaction recordings at the county level.

These state-specific rules necessitate careful research and compliance by applicants to ensure full alignment with both federal and state regulations.

By thoroughly understanding these varied aspects, taxpayers can efficiently navigate the intricacies of the Application for Certificate of Discharge of Federal Tax Lien, thereby effectively managing their property and tax obligations.