Definition & Meaning

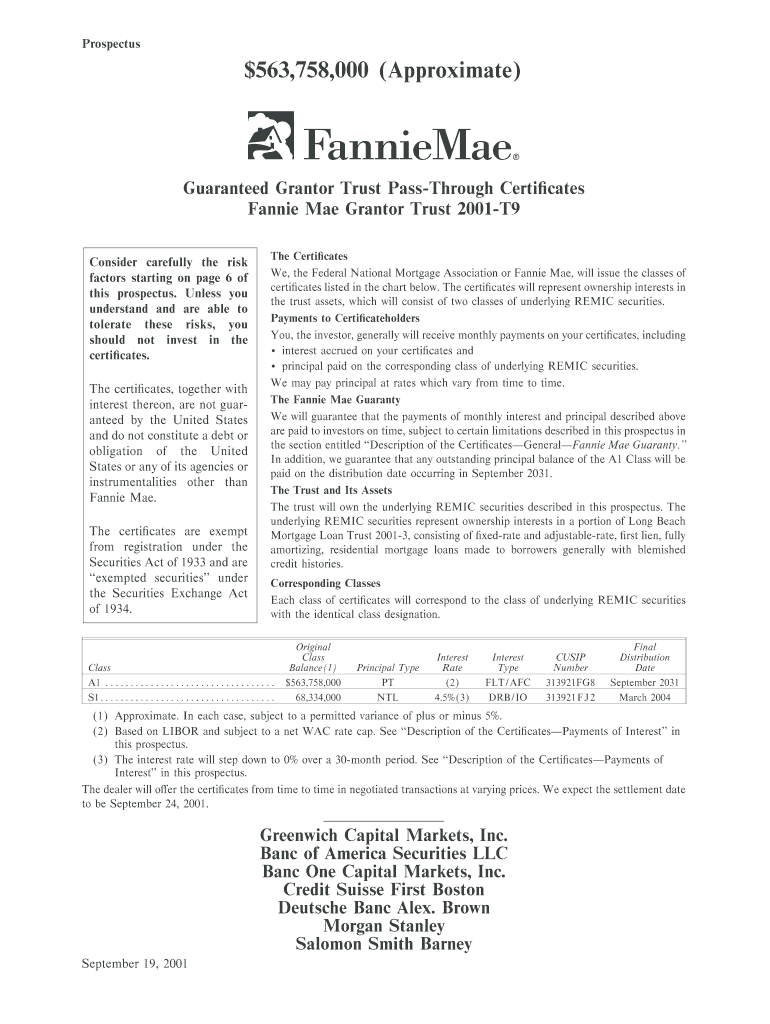

Understanding the specifics of the "563758000 (Approximate) - Fannie Mae" involves grasping its purpose and application in the financial landscape. This is a prospectus for the Fannie Mae Grantor Trust 2001-T9, which involves the issuance of approximately $563,758,000 in Guaranteed Grantor Trust Pass-Through Certificates. These certificates are intricately linked to the underlying mortgage loans they represent. As part of a trust that Fannie Mae guarantees in terms of timely interest and principal payments, these certificates hold no guarantee from the U.S. government. Securities of this nature are exempt from federal securities laws registration.

Key Elements of the 563758000 (Approximate) - Fannie Mae

Significant components of the prospectus include detailed information on the structure of these certificates, the specific mortgage loans they correspond to, and the various risks associated. It highlights pivotal features like:

- Monthly payments to investors derived from the performance of the underlying mortgage loans.

- A guarantee provided by Fannie Mae for the timely receipt of interest and principal on specific classes of the certificates.

- Considerations of varying risk factors such as market conditions, prepayments, and delinquencies which could potentially affect yields.

Who Typically Uses the 563758000 (Approximate) - Fannie Mae

This documentation primarily concerns investors and financial analysts who are scrutinizing or considering investment in mortgage-backed securities. The information contained within serves as a critical guide for those involved in financial planning, investment strategy formulation, and risk management, facilitating informed decisions.

- Investors: Utilize this prospectus to assess the viability and risks of investing.

- Financial Advisors: Aid clients in understanding these investment vehicles.

- Analysts: Evaluate market trends and forecast investment outcomes.

How to Use the 563758000 (Approximate) - Fannie Mae

This form, serving as a detailed financial prospectus, is utilized by investors and analysts to understand the specifics of the Fannie Mae Guaranteed Grantor Trust Pass-Through Certificates. Users can:

- Review the structure and terms of the certificates.

- Analyze underlying mortgage loans tied to these certificates.

- Assess risk variables mentioned in the prospectus.

- Calculate potential returns based on market conditions detailed.

Legal Use of the 563758000 (Approximate) - Fannie Mae

The legal application of the 563758000 (Approximate) - Fannie Mae is paramount for compliance and legitimacy in financial operations.

- Issued certificates are not backed by the U.S. government but are supported by Fannie Mae's assurances.

- The prospectus outlines necessary compliance with federal securities laws, though the certificates themselves are exempt from registration due to specific stipulations.

- Users must ensure adherence to all relevant laws and regulations surrounding mortgage-backed securities.

Examples of Using the 563758000 (Approximate) - Fannie Mae

Practically, investors might utilize the prospectus in scenarios such as:

- Portfolio Diversification: Using these certificates to diversify investment portfolios with guaranteed returns.

- Risk Assessment: Employing the document for a thorough risk analysis of potential investments.

- Strategic Planning: Leveraging its details to form strategic investment plans catering to client needs.

Important Terms Related to 563758000 (Approximate) - Fannie Mae

Key terminologies within the prospectus include:

- Pass-Through Certificates: Securities that collect monthly mortgage payments distributed to certificate holders.

- Guaranteed Grantor Trust: A trust ensuring payments by leveraging Fannie Mae's backing.

- Prepayment Risk: The chance mortgage payments occur more swiftly than anticipated, affecting yield.

Risks Associated with the 563758000 (Approximate) - Fannie Mae

Understanding risk factors is essential for investors and advisors:

- Prepayment Risk: Early payoff of underlying loans resulting in a shorter investment period and reduced interest income.

- Market Conditions: Economic fluctuations can significantly impact the reliability of scheduled payments.

- Delinquency: Non-payment of underlying loans poses potential risks to expected returns.

How to Obtain the 563758000 (Approximate) - Fannie Mae

For investors or entities interested in these financial instruments, acquiring the prospectus requires engaging with financial institutions that facilitate mortgage-backed securities.

- Brokerage Firms: Offer insights and access to these securities.

- Direct Inquiry: Contacting financial institutions such as those directly involved with Fannie Mae can provide necessary information.

State-by-State Differences

Regulatory and taxation differences can affect the utility and treatment of these certificates:

- Variations in state-level regulations may impact the tax treatment of earnings from the certificates.

- Local laws could influence investor obligations or eligibility to invest in certain financial securities.

Required Documents for Engaging with 563758000 (Approximate) - Fannie Mae

Potential investors should prepare:

- Financial Statements: Proof of financial status necessary for solidifying investment arrangements.

- Identification Documentation: Standard compliance requirements ensure verified identity.

- Investment Portfolio: Current investment holdings to ascertain compatibility with new investments.