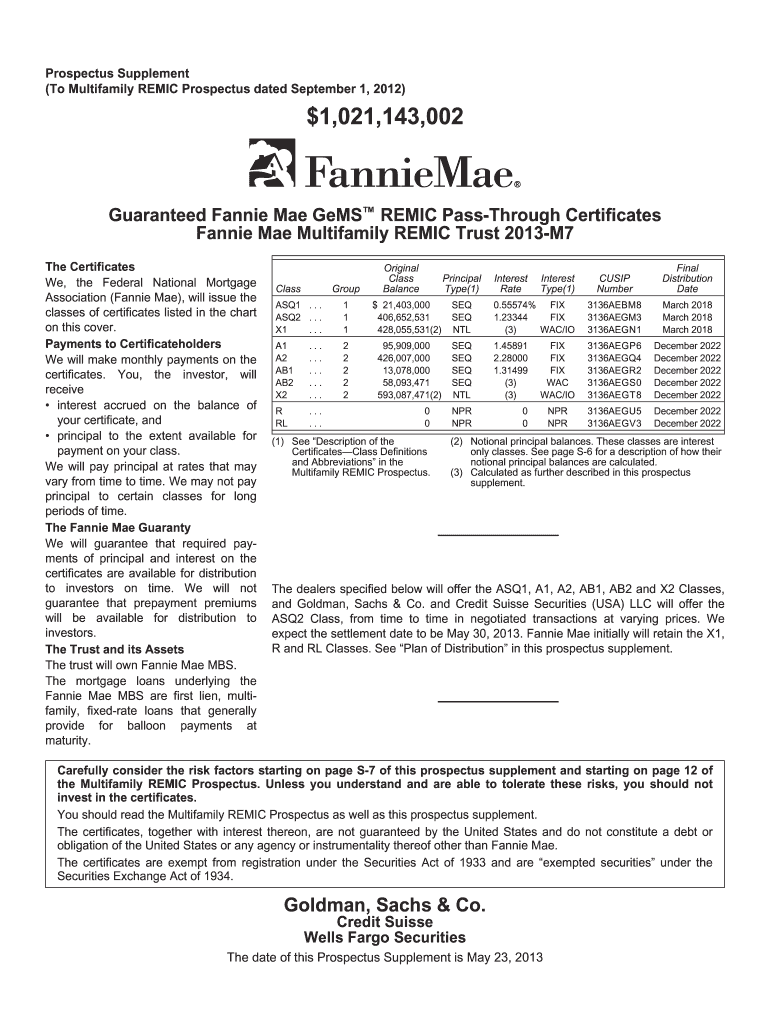

Definition and Meaning of Fannie Mae 2013-M07

The Fannie Mae 2013-M07 refers to a specific issuance of multifamily mortgage-backed securities by Fannie Mae. These are part of the Real Estate Mortgage Investment Conduit (REMIC) trusts, where Fannie Mae acts as a government-sponsored entity providing liquidity and stability to the housing finance system. This particular issuance involves the distribution of pass-through certificates backed by first-lien multifamily mortgage loans, offering monthly payments of principal and interest to investors. The primary purpose of these certificates is to facilitate investment in multifamily residential properties, thereby supporting housing market stability and growth.

Key Elements of the Fannie Mae 2013-M07

- Guaranteed Certificates: The securities are guaranteed by Fannie Mae, ensuring timely payment of principal and interest to investors.

- Underlying Assets: The backing assets are multifamily mortgage loans, which are first-lien loans on apartment buildings and similar properties.

- Payment Structure: Investors receive monthly distributions, which include both interest and principal amounts, based on the cash flow generated by the underlying mortgage loans.

- Risk Factors: The prospectus highlights risks such as prepayment risk, interest rate fluctuations, and economic factors affecting property values, which investors must consider.

How to Use the Fannie Mae 2013-M07

Investors typically use the Fannie Mae 2013-M07 for portfolio diversification and stable income generation. The process involves:

- Reviewing the Prospectus: Analyze the structure, asset backing, and risk factors outlined in the document.

- Assessing Investment Goals: Determine how these securities align with your financial objectives.

- Decision-Making: Based on a risk assessment and financial review, decide whether to include these securities in your investment portfolio.

- Monitoring Performance: Continuously review the performance terms and market conditions that may affect the security's performance.

Important Terms Related to Fannie Mae 2013-M07

- REMIC Trust: A common mechanism for issuing mortgage-backed securities, allowing for tax advantages in the transfer of mortgage loans.

- Pass-Through Certificates: Securities that pass on the income from the underlying mortgages to the investors after deducting fees.

- First-Lien Loans: These prioritize claims over collateral in the event of default, providing additional security to investors.

Steps to Complete Investment in Fannie Mae 2013-M07

- Acquire Investment Knowledge: Familiarize yourself with mortgage-backed securities and REMIC structures.

- Consult Financial Advisors: Seek professional advice to understand the implications and suitability of these securities for your investment strategy.

- Examine Market Conditions: Evaluate economic indicators and real estate market conditions, which influence the performance of multifamily properties.

- Secure Investment Account: Ensure your investment account or brokerage service is capable of purchasing such securities.

Legal Use of the Fannie Mae 2013-M07

The issuance and trading of the Fannie Mae 2013-M07 comply with U.S. securities laws. These securities are primarily for institutional investors with the capacity to purchase large volumes and assess complex financial instruments. Retail investors may access these through investment funds or mutual funds that include mortgage-backed securities.

Who Typically Uses the Fannie Mae 2013-M07

- Institutional Investors: Such as pension funds, insurance companies, and mutual funds, seeking stable, long-term investments with predictable returns.

- Real Estate Investment Trusts (REITs): Organizations focused on investing in income-generating real estate assets.

- Private Investors: High net-worth individuals looking for portfolio diversification and income creation.

State-Specific Rules for the Fannie Mae 2013-M07

While national regulations primarily govern these securities, state-specific rules can influence the underlying properties, including zoning laws, property taxes, and tenant rights legislation. Investors should consider how these local factors might impact the performance of the underlying assets in specific states.

Examples of Using the Fannie Mae 2013-M07

In practice, an institutional investor might utilize Fannie Mae 2013-M07 certificates to supplement their income-focused investment portfolio, benefiting from the diversified risk inherent in multifamily mortgages. A mutual fund may include these securities to provide its investors with exposure to the real estate market without direct property ownership. These examples illustrate the versatility and stability that multifamily mortgage-backed securities offer to various investment strategies.