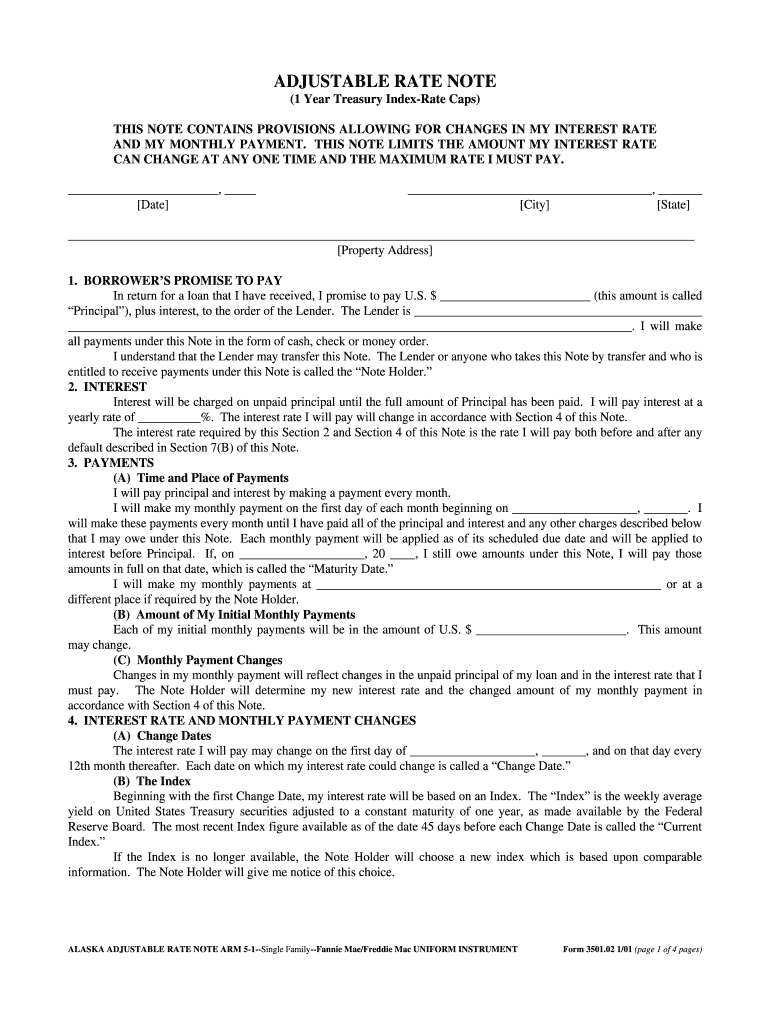

Definition and Meaning of the Adjustable Rate Note

An Adjustable Rate Note is a legally binding document outlining the terms and conditions of a loan agreement with a variable interest rate. This type of financial instrument allows the interest rate on the loan to change at specified intervals, which are often tied to a recognized financial index. In essence, it is a promissory note where the borrower commits to repaying a principal amount along with interest that may vary throughout the loan period. The document includes specifics on how interest rate adjustments are determined, schedules for payments, and stipulations on maximum rate changes.

Key Features and Content

- Interest Rate Adjustments: Details on how the interest rate will adjust over time, linked to market indices.

- Maximum and Minimum Caps: Provisions to cap the maximum and minimum interest rates to protect both lenders and borrowers.

- Borrower and Lender Obligations: Clearly outlines the responsibilities of both parties, including payment schedules and conditions for default.

How to Use the Adjustable Rate Note

The Adjustable Rate Note is primarily utilized during the setup of a loan transaction where variable interest rates can benefit the borrower, particularly if interest rates are expected to decrease. The note offers borrowers flexibility in their financial planning by potentially lowering the starting interest rate compared to fixed-rate loans, sometimes resulting in lower initial payments. However, understanding the intricacies of potential rate increases is crucial.

Practical Application

- Benefit from Lower Initial Rates: Individuals anticipating interest rate declines can take advantage of lower initial payments.

- Payment Fluctuations: Borrowers should prepare for possible payment changes over the loan term as rates fluctuate.

Key Elements of the Adjustable Rate Note

An effective Adjustable Rate Note includes several essential components to ensure clarity and legal enforceability.

Interest Rate Details

- Initial Rate and Adjustments: Precise definitions of the initial interest rate, index references, and adjustment frequency.

- Lifetime Cap: An upper limit on how much the interest rate can increase over the life of the loan.

Payment Structure

- Schedule: Specifics on how often payments are required and potential changes in these payments over time.

- Amortization Details: Information on how much of each payment will be applied to interest versus principal reduction.

Important Terms Related to Adjustable Rate Note

Understanding key terms related to an Adjustable Rate Note is critical for borrowers and lenders alike.

Commonly Used Terminology

- Index: A benchmark interest rate that reflects general market conditions used to adjust loan rates.

- Margin: A fixed percentage added to the index rate to calculate the new loan interest rate.

- Adjustment Period: The frequency with which the interest rate can change, typically annually or bi-annually.

Steps to Complete the Adjustable Rate Note

Completing an Adjustable Rate Note requires careful attention to detail and thorough understanding of its terms.

Process Overview

- Review Initial Terms: Evaluate the starting interest rate and how it compares to expectations for future rate changes.

- Understand Adjustment Mechanics: Familiarize yourself with the index, margin, and adjustment period described in the note.

- Verification of Legal Provisions: Ensure all caps on interest rate changes and any borrower-specific terms are clearly documented.

- Finalize and Sign: Follow proper procedures to execute the document with valid signatures from all necessary parties.

Legal Use of the Adjustable Rate Note

Adjustable Rate Notes are used within the legal framework governing loan agreements in the United States. They provide a flexible financial tool for borrowers but also entail certain risks that need careful legal consideration.

Compliance and Enforcement

- Contract Law Compliance: Ensure the note is drafted in accordance with federal and state laws to avoid disputes.

- Enforceability: Properly structured notes can be enforced in a court of law in cases of default or disputes.

Who Typically Uses the Adjustable Rate Note

The Adjustable Rate Note is commonly used by a diverse group of borrowers, depending on their financial strategies and market conditions.

Typical Users

- Homebuyers and Homeowners: Often utilized in mortgage transactions when buyers anticipate a fall in interest rates.

- Small Business Owners: Used in financing where initial lower payments provide cash flow flexibility.

- Investors: Applied in property investments where short-term holding is anticipated before market conditions shift.