Definition and Meaning

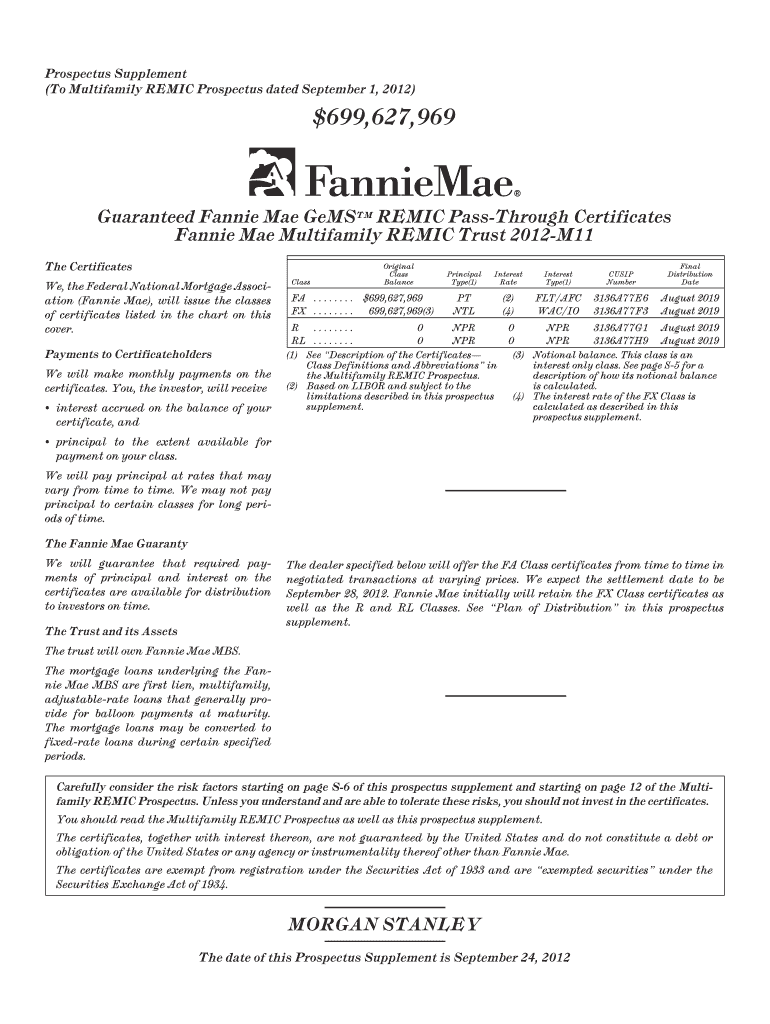

The phrase "We, the Federal National Mortgage Association (Fannie Mae), will issue the classes" pertains to Fannie Mae's role in issuing classes of securities. Fannie Mae, a government-sponsored enterprise, plays a crucial part in the secondary mortgage market by purchasing mortgages from lenders, pooling them, and issuing mortgage-backed securities. The "classes" refer to tranches of securities that differ in terms of risk and return, catering to varied investor preferences. Investors acquire these certificates, backed by property mortgages, offering a blend of security and returns.

Importance of Understanding Issuance

Understanding the issuance of these classes is vital for investors to evaluate the potential risks and returns associated with each tranche. The process impacts both the liquidity and stability of the secondary mortgage market. It also involves specific legal and financial implications that must be recognized to ensure informed investment decisions.

How to Use the Issued Classes

Navigating Securities Tranches

To effectively use the issued classes of securities by Fannie Mae, investors should assess the different tranches offered within a given issuance. Typically, these tranches are differentiated by their credit ratings, maturities, and coupon rates.

- Assess Risk Levels: Each tranche carries a unique level of risk based on its position in the repayment hierarchy. Senior tranches are generally less risky, receiving priority on interest and principal payments.

- Determine Investment Goals: Align investment strategies with suitable tranches. For example, risk-averse investors might prefer senior tranches, while those seeking higher returns might opt for subordinate tranches.

Monitoring Performance

Once the securities are acquired, monitoring their performance is crucial. Investors should stay updated with interest rate changes, payment schedules, and Fannie Mae's creditworthiness, which can affect security performance.

Steps to Complete the Issuance Process

-

Analyze the Prospectus: Before engaging in transactions, thoroughly review the prospectus supplement for detailed information on the trust's structure, payment distributions, and underlying mortgage characteristics.

-

Determine Investment Suitability: Consider personal financial goals, risk tolerance, and investment timeline to determine appropriate tranches and investment amounts.

-

Consult Financial Experts: Engage with financial advisors or brokers when necessary to understand complex aspects of securities investment and to tailor strategies accordingly.

-

Acquire Securities: Utilize brokerage accounts to purchase desired tranches. Ensure compliance with all regulatory requirements during this process.

-

Track and Report: Keep detailed records of all transactions and monitor any communications from Fannie Mae or financial advisors regarding changes in market conditions.

Legal Use and Compliance

Understanding the legal framework of Fannie Mae's issuance is imperative for maintaining compliance.

Adhering to U.S. Securities Regulations

- Abide by ESIGN Act: Electronic financial documents, including purchase agreements, should comply with this law ensuring legality and legitimacy.

- AML and KYC Regulations: Certain transactions may necessitate adherence to Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols to verify the identities and financial standing of investors.

Tax Implications

Be aware of tax obligations relating to interest income from securities and any capital gains taxes applicable upon selling securities.

Who Typically Uses These Classes

- Institutional Investors: Pension funds, insurance companies, and mutual funds frequently invest in Fannie Mae securities for their relatively stable returns and significant market size.

- Individual Investors: Wealthy individuals seeking long-term, mortgage-backed investment opportunities might also find these securities attractive.

- Financial Institutions: Banks and credit unions use these securities as part of their portfolio to diversify risks and capitalize on stable returns.

Examples of Usage

Case Study: Institutional Investment

A pension fund invests in Fannie Mae securities' senior tranches, targeting low-risk, stable returns. By staggering investments across varying maturities, the fund aligns with its long-term payout obligations while maintaining security.

Scenario: Individual Investor Strategy

An individual investor, seeking higher returns, opts for subordinate tranches with a higher yield. By allocating a portion of their portfolio to different tranches, they manage risk while pursuing potential gain.

Key Elements of Issued Classes

Structure and Characteristics

- Adjustable-Rate Mortgage Loans: Many Fannie Mae securities are backed by these loans, which can affect payment stability based on interest rate fluctuations.

- Underlying Property Types: Tranches are often backed by multifamily properties, providing diverse exposure to real estate markets.

Payment Distributions

- Scheduled Principal and Interest Payments: Understand the schedule for these payments as outlined in the securities' terms.

- Prepayment Risks: Familiarize with the impact of borrowers prepaying mortgages, which can affect cash flow to investors.

Software Compatibility and Integration

While specific securities transactions might not require software integration like tax forms, investors should maintain financial software applications such as:

- QuickBooks: For tracking investments, recording transactions, and maintaining a comprehensive financial overview.

- Portfolio Management Tools: Offer real-time tracking and performance analysis, essential for evaluating returns.

Focus on software that enhances operational efficiency while providing detailed reporting and investment insights.