Definition and Meaning of the Uniform Residential Loan Application

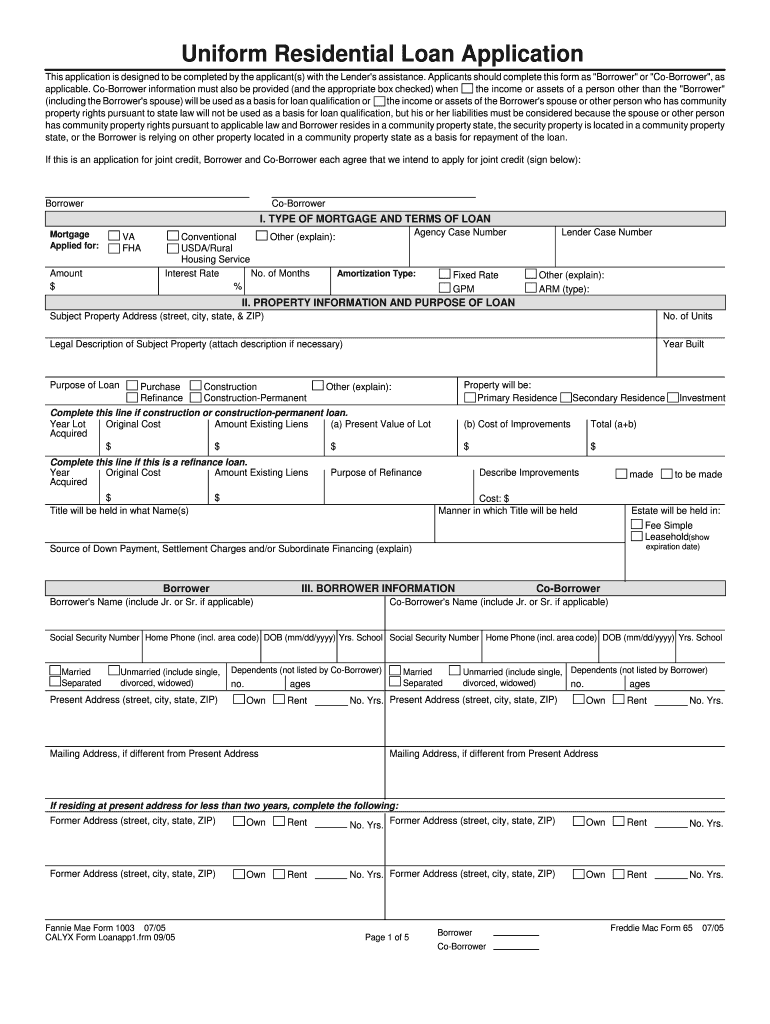

The Uniform Residential Loan Application, often referred to as Form 1003, is a standardized document used by lenders in the United States to collect financial and personal information from those applying for a mortgage loan. This form is crucial because it enables lenders to determine an applicant’s creditworthiness and to make informed decisions about loan approval. The form gathers comprehensive details, not only about the loan being sought but also about the applicant’s assets, liabilities, and employment history, ensuring a thorough evaluation of the borrower’s financial status.

How to Use the Uniform Residential Loan Application

When utilizing the Uniform Residential Loan Application, applicants will fill out a series of sections designed to capture pertinent personal, financial, and property-related details. Some critical components include:

- Personal Information: Name, address, Social Security number, and marital status.

- Income and Employment: Details about current employment, income sources, and history.

- Assets and Liabilities: Listing of bank accounts, debts, and liabilities to paint a clear picture of financial health.

Applicants must be meticulous and ensure accurate information in each part, as any discrepancies can delay the approval process or result in a denial.

Steps to Complete the Uniform Residential Loan Application

- Gather Your Documents: Before starting, collect all necessary documents such as pay stubs, bank statements, and employment details.

- Fill Out Personal Details: Complete sections about personal information, including your identity and contact details.

- Provide Income and Employment Information: List all sources of income and employment history. Supporting documents may be required for verification.

- Declare Assets and Liabilities: Accurately input details of your financial assets and liabilities. Include savings accounts, debts, and loans.

- Detail Property Information: If applicable, information about the property to be purchased is necessary.

- Review and Sign: Carefully review the entire form for accuracy. Both the borrower and co-borrower (if any) must sign.

Key Elements of the Uniform Residential Loan Application

The Form 1003 contains several key elements essential for its completion:

- Borrower Information: Basic identification data.

- Monthly Income and Combined Housing Expense Information: This section lays out expected expenses versus income.

- Assets and Liabilities: A thorough list of financial considerations.

- Declarations: A set of yes/no questions regarding bankruptcy, lawsuits, and any foreclosures.

- Acknowledgment and Agreement: Signifies that all information provided is true and accurate to the best of the applicant’s knowledge.

Legal Use of the Uniform Residential Loan Application

The legal use of the Uniform Residential Loan Application involves the adherence to federal regulations that protect applicants. For example, applicants are protected by the Fair Housing Act and Equal Credit Opportunity Act, which prevent discrimination based on race, color, religion, national origin, sex, familial status, or disability. Additionally, applicants have the right to a copy of their appraisal report if the application involves real estate.

State-Specific Rules for the Uniform Residential Loan Application

While the Uniform Residential Loan Application is used nationwide, some states have additional requirements or disclosures. For example, state-specific regulations might pertain to how information is collected for state tax purposes, or they might influence additional documentation requirements based on local real estate practices. Applicants should check with their loan officer or mortgage lender to understand any local stipulations.

Examples of Using the Uniform Residential Loan Application

The Form 1003 is used in numerous scenarios:

- First-Time Homebuyers: An essential tool for individuals stepping into homeownership.

- Refinancing Existing Loans: Homeowners seeking better interest rates or terms.

- Investment Property Loans: Those looking to invest in real estate using mortgage financing.

- Joint Applications: For co-borrowers applying together, providing a comprehensive view of combined financial data.

Important Terms Related to the Uniform Residential Loan Application

Several terms are intrinsically linked with the Uniform Residential Loan Application, including:

- LTV Ratio (Loan-to-Value): Reflects the ratio of the loan amount to the appraised value of the property.

- PITI (Principal, Interest, Taxes, and Insurance): Represents the total mortgage payment, inclusive of loan repayment and associated expenses.

- DTI Ratio (Debt-to-Income): A critical ratio calculated to assess the risk of lending, based on borrower liabilities versus income.

Understanding these terms is crucial for applicants as they navigate the application process and interact with lenders.