Definition and Meaning

The Estate Planning Inventory is a comprehensive document designed to help individuals organize and document necessary personal, familial, financial, and legal information. This inventory serves as a critical tool for effective estate planning by ensuring that all essential details are readily accessible to the executor or family members following an individual's passing. With sections covering personal and familial details, financial records, and legal documents, the Estate Planning Inventory provides a structured approach to managing one's estate, aiming to facilitate a smooth transition and minimize potential legal or administrative complications.

Key Elements of the Estate Planning Inventory

The Estate Planning Inventory includes several key sections, each serving a specific purpose in the comprehensive organization:

- Personal Information: Includes full name, date of birth, Social Security number, and contact details, providing the foundational data required for legal and administrative tasks.

- Family History: Documents familial relationships and any significant medical history that might affect heirs, helping executors manage personal affairs sensitively and accurately.

- Key Advisors: Lists contact details for lawyers, accountants, and financial advisors, ensuring quick access to professional guidance as needed.

- Important Documents: Identifies locations of essential documents such as wills, power of attorney, and trusts, facilitating efficient retrieval and use.

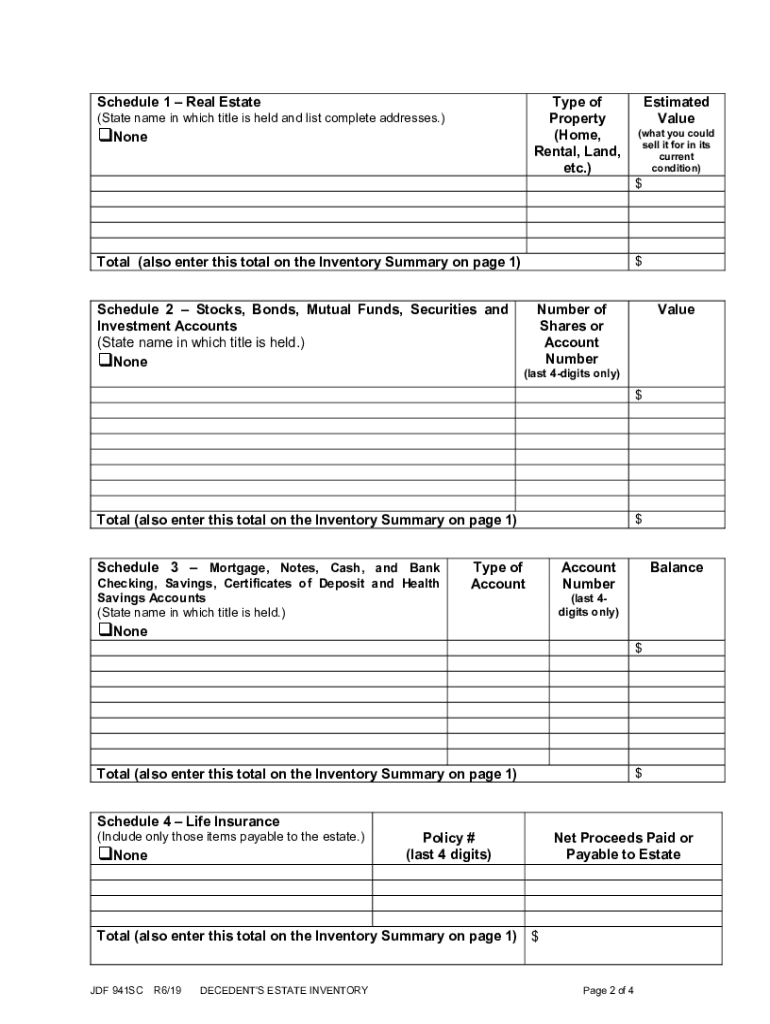

- Financial Holdings: Details real estate ownership, bank accounts, investments, retirement accounts, and business interests, offering a comprehensive overview of an individual's financial landscape.

- Insurance Policies: Catalogs life, health, auto, and property insurance policies, providing a safeguard for beneficiaries.

- Debts and Obligations: Lists outstanding loans and credit card debts, clarifying the liabilities of the estate.

Steps to Complete the Estate Planning Inventory

- Gather Personal and Family Information: Start by compiling personal data, including full names, birthdates, and Social Security numbers for you and your close family.

- Identify and Document Advisors: Record the names and contacts of all advisors, such as lawyers and accountants, to streamline communication.

- Locate Important Documents: Collect and categorize all key documents, ensuring they are updated and stored in a safe, easily accessible location.

- Itemize Financial Assets: List all financial assets, including bank accounts, investment portfolios, and property holdings, to provide a clear financial snapshot.

- Verify and List Insurance Policies: Review all policies and make note of providers, coverage details, and beneficiaries.

- Outline Debts and Financial Obligations: Document all outstanding debts to present a complete financial picture.

How to Use the Estate Planning Inventory

Utilizing the Estate Planning Inventory effectively involves understanding its role in the broader estate planning process. This inventory should be seen as a dynamic document, regularly reviewed and updated to reflect any changes in personal circumstances or asset holdings. Users should ensure that all sections are comprehensively completed, providing a clear guide for executors or family members during the estate settlement process. Regular consultations with legal advisors can also ensure compliance with current estate laws and practices, reflecting the most accurate and beneficial information.

Legal Use of the Estate Planning Inventory

In the context of U.S. legal practices, the Estate Planning Inventory is a non-binding but crucial document that supports estate planning activities. While the inventory itself may not hold legal weight, it acts as a supportive document that guides legal processes such as probate. This inventory assists executors by clearly itemizing the deceased's wishes and holdings, thereby simplifying court proceedings and reducing the likelihood of disputes. Users should consult with legal professionals to ensure their inventory aligns with relevant state laws and complements their broader estate planning documents.

State-Specific Rules for the Estate Planning Inventory

Different states may have varying requirements and recommendations for estate planning documentation. In states like California or Texas, where estate regulations can be complex, particular attention to detail in preparing an Estate Planning Inventory can avert potential legal hurdles. Therefore, it is important to understand local probate laws and consult with a local estate attorney to ensure the inventory complies with specific state mandates. This proactive approach can protect against inadvertent legal oversights and ensure smoother estate management.

Examples of Using the Estate Planning Inventory

Consider a scenario where an individual with diverse assets across multiple states uses an Estate Planning Inventory. By effectively documenting these assets, the person can provide clear and consistent instructions to family and legal representatives. In another example, a person with a complex family structure might use the inventory to outline specific distributions and personal bequests, ensuring all parties understand their intentions. These scenarios underscore the utility of a well-organized estate planning inventory in clarifying wishes and reducing potential family conflicts.

Required Documents

Completion of the Estate Planning Inventory necessitates the compilation of various documents:

- Legal Documents: Wills, trusts, power of attorney, and healthcare directives provide structured instructions for estate management.

- Financial Statements: Bank statements, investment reports, tax returns, and property deeds offer a complete view of financial holdings.

- Insurance Papers: Policy documents for life, health, and property insurance ensure beneficiaries are aware of available benefits.

- Debt and Obligation Records: Documenting outstanding debts and obligations aids in financial planning and settlement.

Who Typically Uses the Estate Planning Inventory

Typically, individuals who are looking to organize their estate affairs comprehensively, regardless of the size of their estate, will find value in using an Estate Planning Inventory. This includes both younger adults beginning their estate planning journey, as well as seniors ensuring their affairs are in order. Additionally, executors and family members tasked with managing an individual's estate will benefit greatly from a detailed inventory, as it can significantly simplify the settlement process and ensure all parties are aware of what documents and information are necessary and available.