Definition and Meaning

The foreclosure worksheet, specifically the JD-CV-77 used in Connecticut's Superior Court system, is an essential document related to foreclosure proceedings. It serves as a detailed record that supports a Motion for Judgment of Foreclosure. This worksheet captures crucial information about the property in question, including financial details such as outstanding debts and existing liens. By thoroughly documenting these elements, the worksheet assists in ensuring that foreclosure actions are conducted accurately and in compliance with applicable laws.

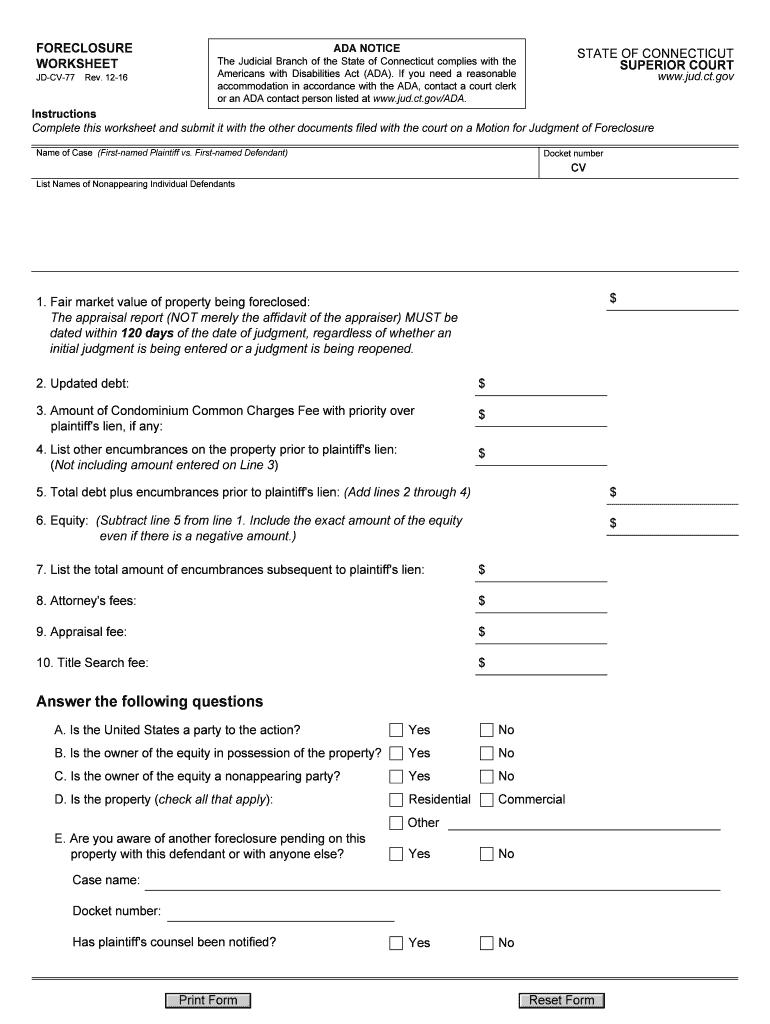

Steps to Complete the Foreclosure Worksheet

Completing a foreclosure worksheet involves several precise steps to ensure an accurate and lawful record. Each section should be filled out meticulously:

- Property Details: Begin by documenting the property's legal description and address.

- Debts and Encumbrances: List all known debts associated with the property, including mortgages, liens, and any junior claims.

- Parties Involved: Identify all individuals and entities holding a financial interest in the property, such as lenders and lienholders.

- Compliance with ADA: Ensure compliance with the Americans with Disabilities Act (ADA), which may require additional information based on the parties' circumstances.

- Review and Verify: Double-check all entries for accuracy before submission to avoid delays.

Key Elements of the Foreclosure Worksheet

The foreclosure worksheet incorporates several key elements that must be addressed:

- Identification of the Foreclosing Party: Clearly state the party initiating the foreclosure process.

- Property Valuation: Provide a current valuation of the property to assess the sufficiency of collateral.

- Payment History and Defaults: Include a history of payments and any defaults, which may affect foreclosure proceedings.

- Lien Priorities: Define the order of claims to ensure proper distribution of proceeds post-foreclosure.

Who Typically Uses the Foreclosure Worksheet

The foreclosure worksheet is primarily used by legal professionals, including attorneys and paralegals, representing clients in foreclosure cases. Financial institutions and lenders also rely on these worksheets to ensure that foreclosure proceedings align with legal requirements. Additionally, property owners facing foreclosure and court officials use the worksheet to track and verify foreclosure details.

Legal Use of the Foreclosure Worksheet

The foreclosure worksheet plays a legal role in foreclosure proceedings, serving as evidence during court hearings. It helps establish the validity of claims and compliance with statutory regulations, thereby assisting judges and legal parties in assessing the legitimacy of the foreclosure action. Properly completed worksheets enable a streamlined legal process, reducing the potential for disputes and appeals.

State-Specific Rules for the Foreclosure Worksheet

Different states may impose unique regulations on foreclosure worksheets. In Connecticut, for instance, the JD-CV-77 form is designed to meet specific state requirements, including disclosures under the ADA. Those involved in foreclosure proceedings must be aware of state-specific instructions and ensure that all information provided aligns with local legal standards.

Digital vs. Paper Version

Foreclosure worksheets are available in both digital and paper formats, each offering distinct advantages:

- Digital Version: Allows for easy editing and sharing among involved parties. It can be integrated with electronic filing systems for convenient submission.

- Paper Version: May be preferred in traditional legal settings where physical documentation is required for records.

Both versions require the same level of detail and accuracy, but the choice may depend on the resources and preferences of the involved parties.

Required Documents

Completing a foreclosure worksheet necessitates several supporting documents, including:

- Promissory Notes: Documenting original loan agreements.

- Mortgage or Deed of Trust: Showing the secured interest in the property.

- Payment Records: Detailing the history of mortgage payments.

- Lien Certificates: Confirming the existence and priority of any attached liens.

Ensuring that these documents are current and accurate is essential for the worksheet's successful completion and acceptance.

How to Obtain the Foreclosure Worksheet

The foreclosure worksheet can be obtained through several avenues:

- Connecticut Superior Court: Directly from the court's website or physical office.

- Legal Representatives: Attorneys may provide the worksheet as part of their legal services.

- Official State Publications: Certain government offices or publications may offer downloadable forms.

Accessing the most current version is crucial to remain compliant with any updates or changes in the legal requirements.

Examples of Using the Foreclosure Worksheet

The worksheet is applied in various real-world scenarios:

- Legal Proceedings: It acts as a core document during foreclosure court cases, providing a detailed record of all necessary data.

- Negotiation with Lenders: Homeowners and legal advisors may use the worksheet to work out alternatives to foreclosure, such as loan modifications.

- Financial Analysis: Lenders use it to evaluate collateral recovery potential and decide on the most feasible foreclosure action.

These examples showcase the worksheet's versatility across different stages of the foreclosure process.