Definition & Meaning

The Solo 401(k) Profit Sharing Plan Adoption Agreement is a critical document for self-employed individuals looking to establish a retirement savings plan that consolidates both elective salary deferrals and profit-sharing contributions. This agreement specifies the employer's commitment to the plan, its operational procedures, eligibility criteria, and funding limits. It serves as the blueprint for administering the Solo 401(k) plan in compliance with IRS regulations, thereby ensuring the plan's qualification for tax benefits.

Key Elements of the Agreement

Employer and Plan Details

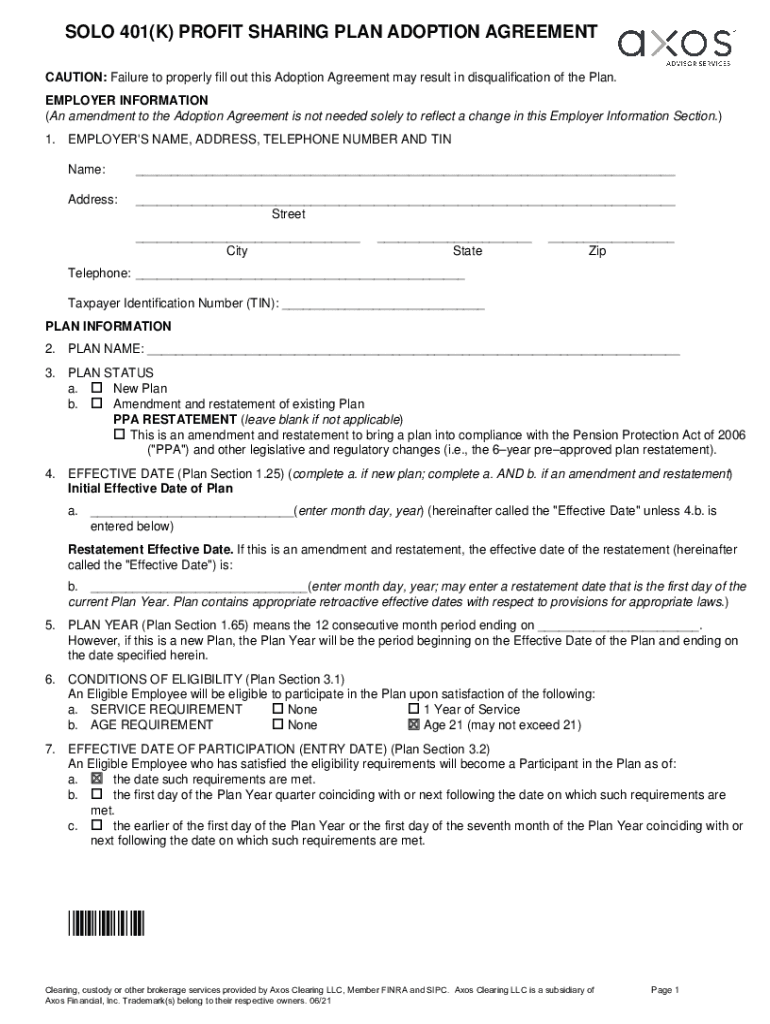

This section requires entering basic details such as the employer's name, the employer identification number (EIN), and the official plan name. These foundational elements are crucial for establishing the legal identity of the plan and its sponsorship.

- Employer Name: The legal name of the self-employed individual or business entity.

- EIN: Typically, this is a nine-digit number used for tax reporting purposes.

- Plan Name: A unique identifier of the Solo 401(k) plan.

Eligibility Criteria

Eligibility provisions outline who can participate in the 401(k) plan. This typically includes any self-employed individual who meets specific requirements, such as having no full-time employees and performing necessary managerial duties.

- Self-employment Requirement: Participation is limited to sole proprietors, partners, and owners who don’t employ others full-time.

- Age and Service Conditions: Minimum age and service requirements may be stipulated, ensuring all conditions align with IRS guidelines.

Contribution Options

Contributions are a central aspect of the Solo 401(k) plan, combining elective deferrals with employer profit-sharing contributions. The agreement details maximum contribution limits and procedures for making contributions.

- Elective Deferrals: Participants can contribute a portion of their earnings up to IRS limits.

- Profit-Sharing Contribution: This allows additional contributions up to 25% of net income (business revenue less expenses), enabling higher savings potential.

- Catch-up Contributions: Individuals over age 50 may make additional contributions to maximize retirement savings.

Steps to Complete the Agreement

- Obtain the Form: Download the form from the Axos Advisor Services website or access it through approved financial service platforms like DocHub.

- Fill in Employer Details: Start with the employer's name, EIN, and address to establish the sponsor's identity.

- Define Eligibility: Specify the criteria that determine employee eligibility to ensure regulatory compliance.

- Outline Contribution Methods: Include options for salary deferrals and profit-sharing contributions; provide the formula for calculating contributions.

- Designate the Trustee: Appoint a responsible party or entity for managing plan investments.

- Review and Sign: Ensure all information is accurate, then sign the document to finalize the setup.

Legal Use and Importance

The adoption agreement serves as a legally binding contract, articulating the plan’s terms and conditions. This document is essential for ensuring the Solo 401(k) plan conforms to IRS regulations and secures favorable tax treatment. Non-compliance can result in disqualification, potentially leading to tax penalties.

- IRS Compliance: Ensures adherence to tax and labor laws.

- Documented Procedures: Establishes formal procedures for contributions and plan operations.

- Protection Against Penalties: Reduces risk of penalties by ensuring all requirements are clearly outlined.

Who Typically Uses the Form

This form is primarily used by self-employed individuals, such as sole proprietors, partners in businesses without full-time employees, and independent contractors, looking to maximize their retirement savings through a flexible and tax-advantaged plan.

- Self-Employed Professionals: Doctors, consultants, and freelancers seeking personalized retirement solutions.

- Small Business Owners: Those operating owner-only LLCs or partnerships without external employees.

Required Documents

Before completing the adoption agreement, gather necessary documents to ensure a smooth setup process:

- Business Entity Documentation: Articles of incorporation, if applicable.

- Employer Identification Number: Verification issued by the IRS.

- Proof of Self-Employment: Relevant tax returns or financial statements demonstrating income.

Eligibility Criteria

Eligibility criteria are straightforward, focusing predominantly on self-employment and the absence of full-time employees. This framework ensures that plans benefit the intended demographic and remain compliant with IRS standards.

- Self-employed Individuals: Must actively work and generate earnings through their business activities.

- Lack of Full-Time Employees: No staff members working over 1,000 hours per year, aside from the business owner.

Examples and Scenarios

- Case Study 1: A freelance graphic designer with fluctuating income utilizes the Solo 401(k) to defer a percentage of income, capturing employer matching through profit-sharing.

- Case Study 2: A partner in a small accounting firm employs the agreement to set up a retirement fund for personal savings, managing contributions through the firm’s profits.

Understanding and accurately completing the Solo 401(k) Profit Sharing Plan Adoption Agreement enables individuals to proactively manage their retirement savings while taking full advantage of tax benefits available through the plan.