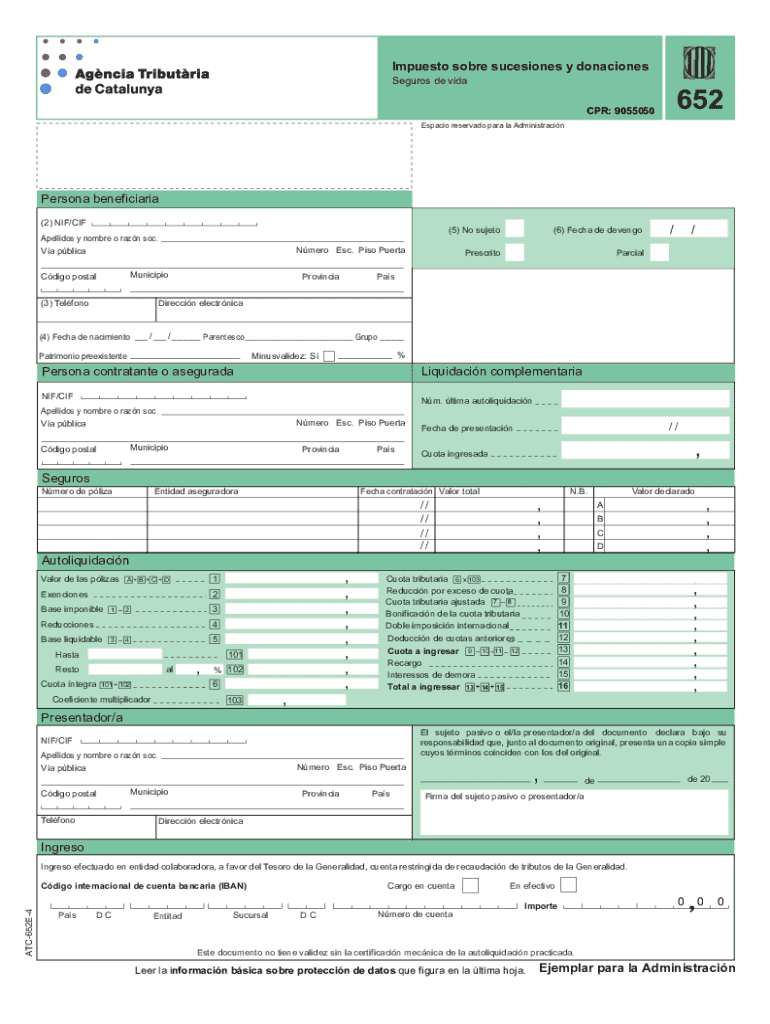

Definition and Meaning

The "Impuesto Sobre Sucesiones Y Donaciones" refers to a tax applied in Spain on the transfer of assets through inheritance or as a gift. It aims to tax the acquisition of wealth through family lines or personal connections, thus preventing an accumulation of untaxed wealth. This tax plays a crucial role in fiscal policy by redistributing wealth and funding public expenditures.

-

Inheritance Tax: This component is levied on the transfer of assets from a deceased individual to their heirs. The tax rate depends on factors such as the heir's relationship to the deceased, the value of the inheritance, and applicable exemptions.

-

Gift Tax: As a complement to the inheritance tax, this tax is levied on gifts made during the giver's lifetime. Similar factors, such as relationship and value, influence the tax rate.

Key Elements of the Impuesto Sobre Sucesiones Y Donaciones

Understanding the key elements of the "Impuesto Sobre Sucesiones Y Donaciones" is essential for accurate calculations and compliance.

-

Tax Base: This refers to the value of the assets received, whether through inheritance or donation. It includes real estate, cash, securities, and personal property.

-

Tax Rates: Rates can vary based on the relationship to the deceased or donor and the value of the acquired assets. Close relatives, such as children or spouses, typically benefit from lower rates.

-

Exemptions and Reductions: Specific exemptions or reductions may apply, such as for primary residences, businesses, or certain monetary thresholds. These can significantly reduce the tax burden.

Steps to Complete the Impuesto Sobre Sucesiones Y Donaciones

Completing this tax form requires precision. Below are the general steps to follow:

- Identify Assets and Values: Start by listing all assets included in the inheritance or gift and assessing their current market value.

- Determine Relationships and Exemptions: Confirm the legal relationship to the deceased or donor, and identify applicable exemptions or reductions.

- Calculate the Tax: Using the tax base and applicable rates, calculate the total tax due on the inheritance or donation.

- Complete the Form: Fill out the required sections of the form, ensuring all details are precise and accurate.

- Submit the Form: Follow the submission guidance applicable to your jurisdiction, whether online, by mail, or in-person.

- Pay the Tax: Ensure that your payment is made by the designated deadline to avoid any penalties.

Required Documents

When dealing with the "Impuesto Sobre Sucesiones Y Donaciones," it is vital to have certain documents ready:

- Proof of Assets: Documentation evidencing ownership and value, such as property deeds or bank statements.

- Probate or Will: The official legal documents detailing the deceased's wishes can be crucial for inheritances.

- Legal Identification: Provide valid identification for both the deceased or donor and all beneficiaries.

- Relationships Evidence: Birth certificates or marriage certificates to validate family ties.

Who Issues the Form

The "Impuesto Sobre Sucesiones Y Donaciones" is typically issued by the local tax authorities within Spain’s autonomous communities. Each community may have specific regulations and requirements, impacting how the form is both issued and processed.

Filing Deadlines and Important Dates

The timeframe for filing the "Impuesto Sobre Sucesiones Y Donaciones" is critical to avoid legal issues:

- Inheritance Tax: Generally must be filed within six months from the date of death. Extensions may be possible under certain conditions.

- Gift Tax: Often requires filing within thirty days of receiving the gift. Prompt filing is necessary to prevent interest charges or penalties.

State-Specific Rules for the Impuesto Sobre Sucesiones Y Donaciones

Each autonomous community in Spain enforces its own interpretations and rules for this tax, leading to state-specific variations:

- Variability in Exemptions: Communities may offer different exemptions, such as for family businesses or agricultural assets.

- Rate Adjustments: Tax rates often differ between regions, potentially influencing the overall tax burden significantly.

Legal Use of the Impuesto Sobre Sucesiones Y Donaciones

The legal application of this tax ensures compliance and transparency:

- Legal Framework: Governed by both national and community-level legislation, ensuring equitable distribution and compliance.

- Tax Evasion Prevention: Stringent laws are in place to discourage and address any attempts at tax evasion or fraud, maintaining fiscal integrity.

Examples of Using the Impuesto Sobre Sucesiones Y Donaciones

Understanding practical applications can clarify how this tax is applied:

- Residential Property Inheritance: When inheriting a family home, beneficiaries might face different tax liabilities based on the region and available reductions.

- Monetary Gifts: Large sums transferred as gifts can be subject to significant tax depending on the proximity of the relationship and existing exemptions.

Penalties for Non-Compliance

Failing to adhere to the requirements for the "Impuesto Sobre Sucesiones Y Donaciones" can result in severe penalties:

- Fines: Monetary fines are imposed for late filing or underpayment of tax due.

- Interest on Late Payments: Unpaid taxes accrue interest, increasing financial liabilities over time.

- Legal Proceedings: Persistent non-compliance can lead to legal action, including investigation by tax authorities.