Definition & Meaning

The "Anzeige eines Erwerbs von Todes wegen" is a legal form required under the German Inheritance and Gift Tax Act, specifically § 30 of the ErbStG. It serves as a notification of acquisition by inheritance, confirming the transfer of assets from a deceased individual to one or more beneficiaries. This form is essential for legal documentation and tax purposes, ensuring proper reporting of inherited assets. The form requires detailed information about the deceased (known as the erblasser), the inheritor (erwerber), and the nature of the assets inherited. It also accounts for any debts related to the estate. The primary purpose is to facilitate accurate taxation and legal compliance in matters of inheritance.

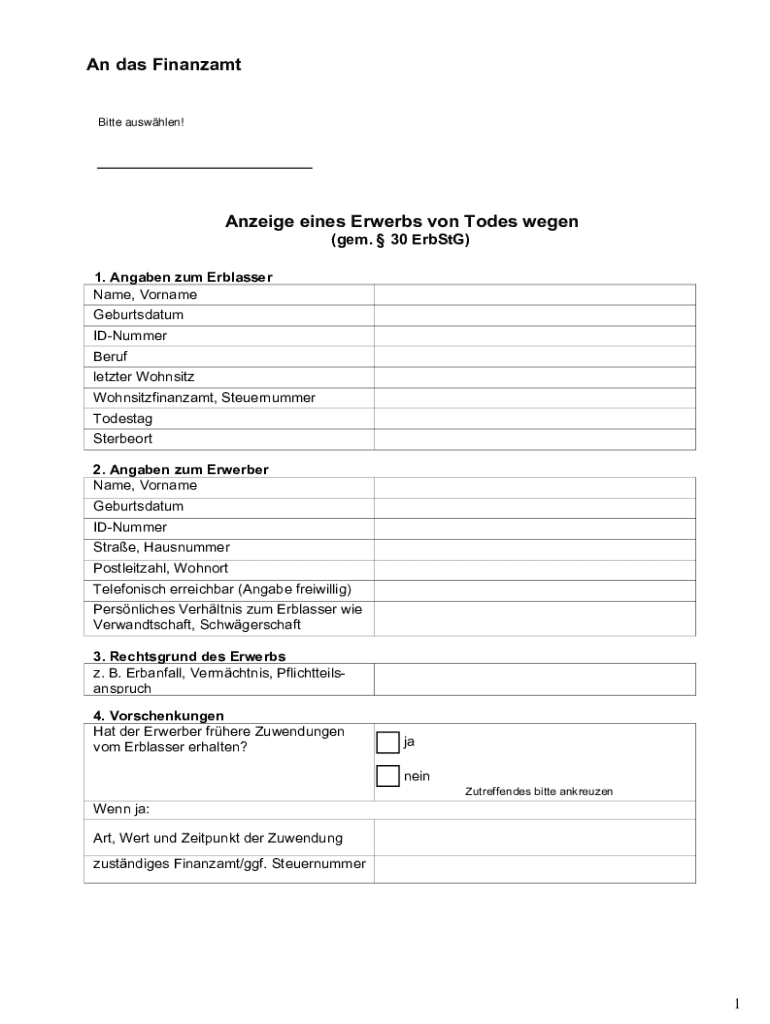

Key Elements of the Anzeige eines Erwerbs von Todes wegen

Understanding the components of the "Anzeige eines Erwerbs von Todes wegen" is crucial for its correct completion. The form includes several vital sections:

- Deceased Information: This section includes personal data about the deceased individual, such as name, date of birth, and date of death.

- Inheritor Details: Here, the inheritor must provide their personal information, including relation to the deceased.

- Legal Basis: The form requires a description of the legal basis for the inheritance, which could include wills, heirship affidavits, or court orders.

- Asset Description: A detailed breakdown of the inherited assets is necessary. This may include property, monetary assets, stocks, and other valuables.

- Debts and Liabilities: Information about any debts that the estate holds, which can impact the net value of inherited assets.

- Previous Gifts: Details of any prior gifts received from the deceased, as they can affect tax calculations.

How to Obtain the Anzeige eines Erwerbs von Todes wegen

Obtaining the "Anzeige eines Erwerbs von Todes wegen" is the first crucial step in the inheritance process. The form can be procured from a variety of sources:

- Government Offices: Tax offices and other local government bodies often provide this form.

- Legal Services: Law firms specializing in estate planning and inheritance may distribute these forms to their clients.

- Online Platforms: Digital versions of the form can be downloaded from credible legal document websites, ensuring accessibility.

- Translation Services: For individuals who might not be fluent in German, some services offer translations while still maintaining legal compliance.

Steps to Complete the Anzeige eines Erwerbs von Todes wegen

Filling out the "Anzeige eines Erwerbs von Todes wegen" involves multiple steps. Each step requires careful attention to detail:

- Collect Data: Gather all relevant information about the decedent and inheritor, including legal documents, asset lists, and previous tax records.

- Fill Personal Sections: Complete sections concerning personal information for both the deceased and the inheritor.

- Describe the Inheritance: Detail all inherited assets and liabilities accurately. Include valuations where necessary.

- Verify Legal Grounds: Ensure that all necessary legal documents to support the inheritance claim (such as wills or court orders) are in order and cross-referenced.

- Review and Correct: Carefully check each section for accuracy and completeness to avoid delays due to incorrect entries.

- Submit the Form: Once completed, submit the form to the appropriate tax office within the deadline.

Filing Deadlines / Important Dates

Timely submission of the "Anzeige eines Erwerbs von Todes wegen" is crucial to comply with legal requirements. The standard deadline for submission is within three months from the realization of the inheritance. Delays in submission can lead to penalties or potential legal complications. It is advisable to adhere strictly to these timelines and prepare all necessary documentation in advance. In special circumstances, extensions can be requested, but these must be justified and are subject to approval by the tax authority.

Legal Use of the Anzeige eines Erwerbs von Todes wegen

This form plays a critical legal role in the inheritance process. It is used to:

- Facilitate Taxation: Helps in the calculation of inheritance taxes, ensuring the government can accurately assess tax obligations based on the value of the assets.

- Document Asset Transfer: Provides a formal record of the transition of ownership from decedent to beneficiary.

- Prevent Fraud: By formally documenting the inheritance, it reduces the risk of fraudulent claims against the estate.

- Ensure Compliance: Keeps all parties involved compliant with German inheritance laws, protecting both inheritors and estate executors.

Penalties for Non-Compliance

Non-compliance with the submission requirements of the "Anzeige eines Erwerbs von Todes wegen" can lead to several penalties:

- Financial Penalties: Late submission or false reporting can result in fines proportional to the estate's value.

- Legal Repercussions: There may be legal consequences for failing to report accurately or for fraudulent submissions.

- Interest on Late Payments: The tax authority might impose interest charges on unpaid taxes resulting from delayed form submission.

State-Specific Rules for the Anzeige eines Erwerbs von Todes wegen

While the form is guided by federal law, there may be specific differences based on the state (Bundesland) in which the inheritance occurs:

- Tax Rates: Some states might have varying inheritance tax rates or additional stipulations.

- Submission Processes: Different states may have unique procedural requirements or additional documentation.

- Legal Aid Availability: Access to legal aid may differ, affecting how inheritors can seek help with form completion.

Adhering to the state-specific regulations is essential for a smooth inheritance process, eliminating potential delays or complications.