Definition & Meaning

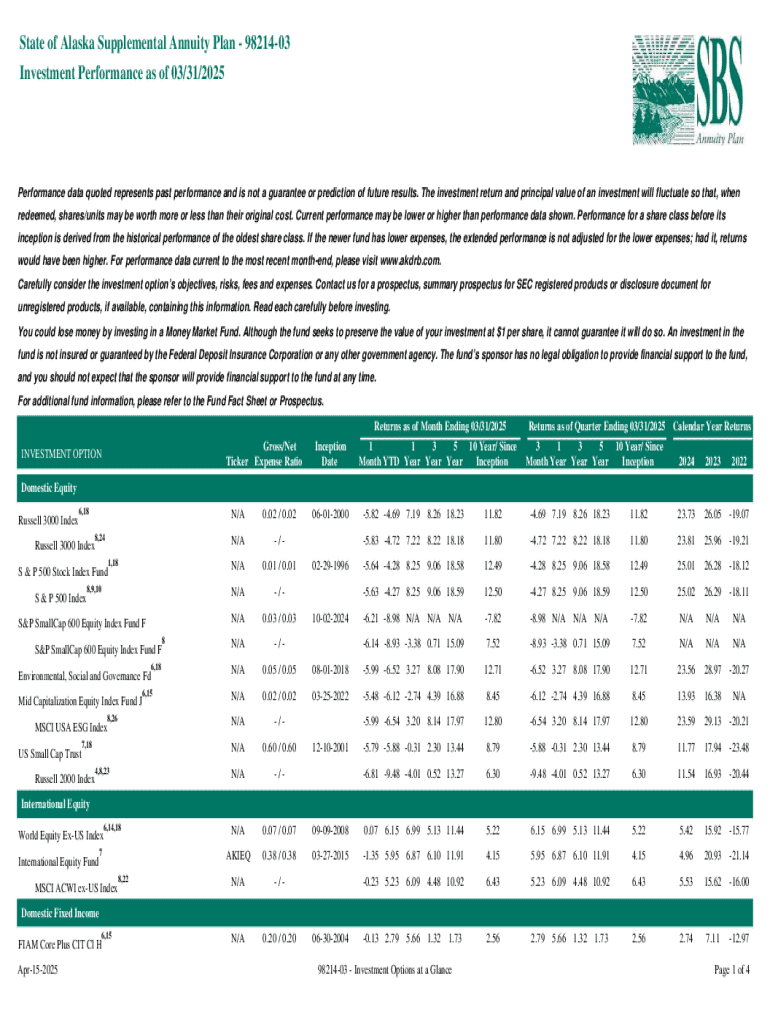

The State of Alaska Supplemental Annuity Plan - 98214-03 serves as a retirement savings vehicle for employees of the state, offering a means to supplement the basic retirement benefits. As an optional plan, it allows participants to invest in a range of funds that can potentially provide additional income upon retirement. Understanding this plan is crucial for employees seeking to enhance their retirement savings, as it offers diverse investment options tailored to different risk appetites and financial goals.

Key Elements of the State of Alaska Supplemental Annuity Plan - 98214-03

-

Investment Options: The plan offers various funds, including money market funds, bond funds, and equity funds. Each option comes with distinct risk levels and expected returns.

-

Expense Ratios and Fees: Participants should be aware of the fees associated with each investment choice, as higher costs can impact overall returns.

-

Contribution Limits: Understanding the maximum allowed contributions is essential for optimizing retirement savings without exceeding IRS limits.

How to Use the State of Alaska Supplemental Annuity Plan - 98214-03

-

Enrollment: To participate, employees must enroll through their human resources department by completing the necessary forms.

-

Contributions: Participants can decide on their contribution level, which can be adjusted periodically based on changes in personal financial circumstances.

-

Investment Adjustments: Employees should regularly review their investment choices and performance to make informed decisions about reallocating funds as needed.

Steps to Complete the State of Alaska Supplemental Annuity Plan - 98214-03

-

Gather Required Documents: Have your employment details, Social Security number, and beneficiary information ready.

-

Fill Out the Form: Complete all sections accurately, ensuring that any selected investment options align with your risk tolerance.

-

Submit the Form: Forward the completed form to the state’s pension office or submit it online through the designated portal, depending on available submission methods.

Eligibility Criteria

The plan is available to employees of the State of Alaska who meet specific employment criteria. Typically, full-time employees are eligible upon hiring, but part-time or seasonal workers may have different requirements or restrictions.

Important Terms Related to State of Alaska Supplemental Annuity Plan - 98214-03

- Vesting: Indicates the length of service required for participants to own the funds contributed by the employer fully.

- Diversification: A strategy to minimize risk by selecting a variety of investments within the annuity plan.

- Return on Investment (ROI): Measures the performance efficiency of the selected investment options.

IRS Guidelines

The IRS provides specific regulations regarding the tax treatment of contributions and withdrawals from the supplemental annuity plan. Contributions may be tax-deferred, allowing employees to lower their taxable income during their working years and defer taxes until withdrawal during retirement.

Legal Use of the State of Alaska Supplemental Annuity Plan - 98214-03

Participants must adhere to legal guidelines concerning the use and withdrawal from the plan. This includes understanding the rules for early withdrawal penalties and required minimum distributions post-retirement. Legal advice may be advisable to avoid penalties and ensure compliance with federal and state laws.

State-Specific Rules for the State of Alaska Supplemental Annuity Plan - 98214-03

Alaska’s specific rules govern how the plan operates, including contribution rates, options for early retirement, and state law compliance. Understanding these can help employees maximize their benefits while ensuring compliance with state regulations.

Who Typically Uses the State of Alaska Supplemental Annuity Plan - 98214-03

The plan is primarily utilized by state employees, including teachers, administrative staff, and other public sector workers seeking to increase their retirement savings beyond the basic state pension plan.

Penalties for Non-Compliance

Failure to adhere to the plan’s regulations, such as exceeding contribution limits or improper withdrawal, may result in financial penalties and possible tax implications. It’s important for participants to stay informed about changing guidelines to avoid such outcomes.