Definition and Meaning of Budgetary Accounting - Government Accountability Office

Budgetary accounting, as defined by the Government Accountability Office (GAO), focuses on the tracking and management of financial resources appropriated by the government. It ensures that funds allocated to various federal programs are used in accordance with legislative intent. The GAO plays a crucial role in auditing, evaluating, and reporting on the financial operations of federal agencies, ensuring they adhere to established norms and regulations.

Core Principles

- Accountability: Ensures government funds are used appropriately.

- Transparency: Provides clear reports on financial allocations and usage.

- Compliance: Aligns with statutory requirements and accounting standards.

Importance

Budgetary accounting is vital for maintaining public trust and ensuring the responsible management of taxpayer dollars. It helps in identifying potential areas of inefficiency or misallocation of funds.

Steps to Complete the Budgetary Accounting - Government Accountability Office

Completing budgetary accounting tasks with respect to the GAO involves several structured steps to ensure accuracy and compliance.

Detailed Steps

- Understand the Requirements: Familiarize yourself with GAO's guidelines and requirements for budgetary accounting.

- Gather Necessary Documentation: Ensure you have all required documents such as current and previous fiscal reports, budgetary requests, and financial statements.

- Allocate Funds Appropriately: Distribute funds according to approved budget lines and legislative directives.

- Track Expenditures: Use accounting systems to monitor spending against budgetary limits.

- Prepare Reports: Compile financial reports summarizing the allocation and use of resources.

- Conduct Audits: Regularly audit financial activities to ensure compliance with GAO standards.

Example Scenario

For instance, if a federal agency receives funding for infrastructure, ensure that expenditures such as construction costs and labor are recorded correctly and match the appropriated funds.

Key Elements of the Budgetary Accounting - Government Accountability Office

The GAO's approach to budgetary accounting involves several key elements that guide federal agencies in their financial operations.

Essential Components

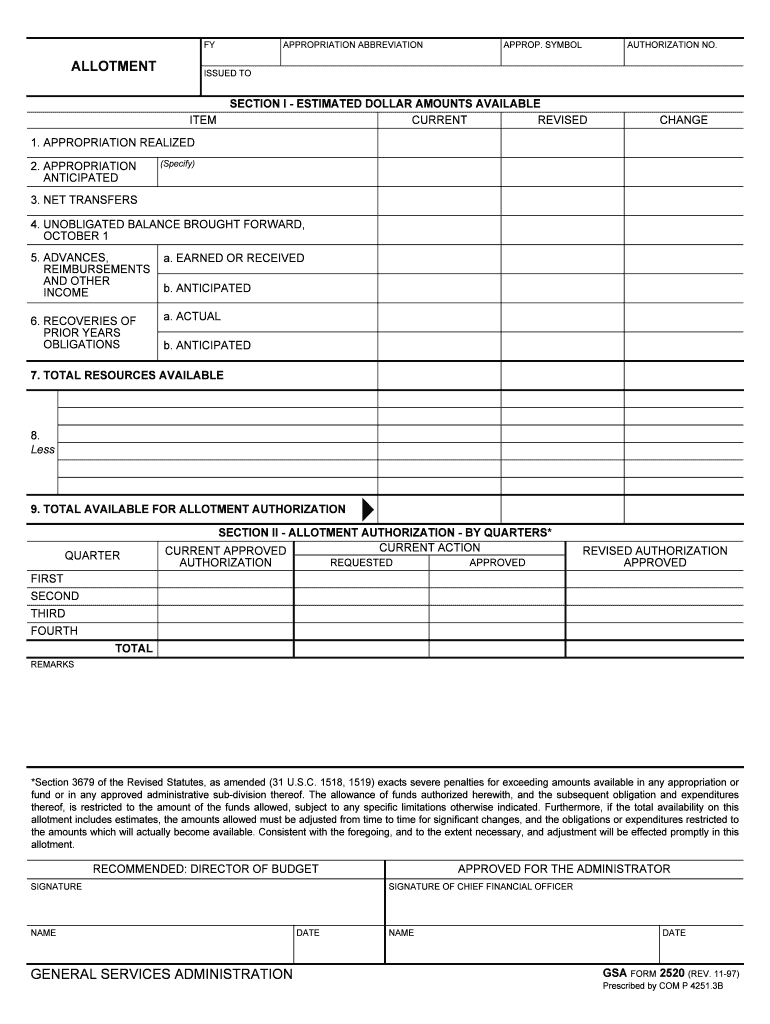

- Appropriations: This is the legal authority granted by Congress for federal agencies to use funds.

- Obligations: As agencies commit to spending, these obligations must be tracked against the appropriated funds.

- Expenditures: Actual spending of funds which needs to be documented and evaluated.

- Reconciliations: Regular comparisons between recorded transactions and actual cash balances to ensure consistency.

Importance

These elements help to ensure that financial activities are properly recorded and that there are no discrepancies in the management of public funds.

Who Typically Uses the Budgetary Accounting - Government Accountability Office

The primary users of budgetary accounting methodologies prescribed by the GAO include various stakeholders within the federal government.

Typical Users

- Federal Agencies: Execute and manage budgetary plans.

- Congressional Committees: Oversee and approve funding allocations.

- Auditors: Conduct audits to ensure compliance.

- Policy Analysts: Evaluate and report on financial effectiveness.

These stakeholders rely on budgetary accounting to make informed decisions regarding policy and financial management.

Important Terms Related to Budgetary Accounting - Government Accountability Office

Understanding specialized terminology is crucial when dealing with budgetary accounting within the context of the GAO.

Glossary of Terms

- Appropriation Act: A congressional law that enables spending of funds.

- Unobligated Balance: Funds that have been appropriated but not yet committed.

- Net Transfers: Movements of funds from one government account to another.

Context and Use

These terms help users navigate the complex landscape of government finance, ensuring clarity in financial documentation and communication.

Legal Use of the Budgetary Accounting - Government Accountability Office

Compliance with legal frameworks is a pivotal aspect of employing budgetary accounting within the GAO framework.

Legal Considerations

- Statutory Compliance: Adherence to laws governing budgetary allocations and expenditures.

- Audit Requirements: Fulfilling obligations for periodic financial audits as mandated by law.

- Penalties for Misuse: Understanding potential legal consequences for non-compliance or misallocation of funds.

Legal compliance ensures that all federal financial operations are within the bounds of federal law and ethical accountability norms.

Examples of Using the Budgetary Accounting - Government Accountability Office

Practical examples highlight the application and implications of budgetary accounting within the GAO.

Application Scenarios

- Infrastructure Projects: Appropriations for public works are monitored and reported for adherence to budgetary constraints.

- Social Programs: Budgetary analysis ensures funds are allocated efficiently to welfare programs.

- Defense Spending: Detailed reporting on defense budgets allows for careful examination of national security expenditures.

Real-World Example

The GAO may report on a federal agency's use of funds for veterans' healthcare, ensuring funds reach intended beneficiaries.

Penalties for Non-Compliance

Understanding the repercussions of non-compliance with budgetary accounting standards set by the GAO is essential.

Penalties Overview

- Financial Penalties: Imposed for overspending or misuse of appropriated funds.

- Operational Penalties: Potential operational restrictions or additional oversight.

- Reputational Damage: Loss of public trust and credibility for agencies involved.

Mitigation Strategies

Adhering to rigorous review and audit processes, alongside training programs for fiscal officers, can minimize risks associated with non-compliance.