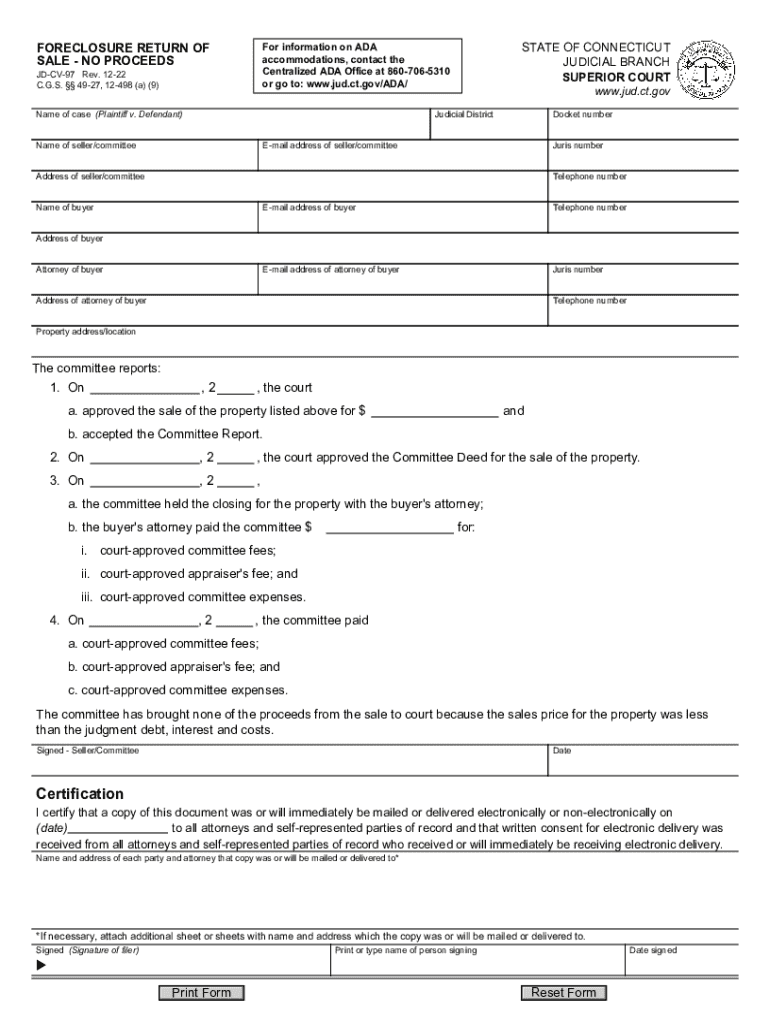

Definition & Meaning

The "Foreclosure Return of Sale - No Proceeds" is a formal document used primarily within the judicial systems of certain states, like Connecticut, to report the outcomes of property foreclosure sales where the sales price is less than the amount owed on the mortgage debt. Typically, such a document provides documentation of the foreclosure process completion, confirms a deficiency where no surplus funds are available for distribution, and legitimizes the sale and internal financial transactions in adherence to court approval processes.

How to Use the Foreclosure Return of Sale - No Proceeds

-

Review the Form's Purpose: Understand that this document is for communicating the lack of proceeds following a foreclosure sale.

-

Gather Financial Data: Collect details about the sale, including the sales price and the outstanding mortgage balance, to ensure the accuracy of submission.

-

Document Court Approval: Include confirmation of sale approval from the court, ensuring the process complies with judicial requirements.

-

Certification of Parties: Certify that necessary documentation has been delivered to all involved parties, meeting both legal and procedural obligations.

Steps to Complete the Foreclosure Return of Sale - No Proceeds

-

Complete Personal and Property Information:

- Enter the names and addresses of involved parties.

- Provide a legal description of the property in question.

-

Enter Financial Details:

- Include specifics about the sale price versus the existing debt.

- State the absence of proceeds clearly.

-

Include Required Signatures:

- Obtain signatures from mandated parties, such as court officials or commissioners overseeing the sale process.

-

Ensure Court Filing and Approval:

- File the form with the relevant judicial office, and wait for formal acknowledgment of receipt and approval.

Key Elements of the Foreclosure Return of Sale - No Proceeds

- Court Verification: Reflection of court authorization of the sale.

- Appendix of No Proceeds: Clearly documented evidence that no funds remain for disbursal.

- List of Fees and Charges: Itemized accounting of any fees related to the sale.

Legal Use of the Foreclosure Return of Sale - No Proceeds

- Judicial Compliance: Ensure the document meets legal standards as per state requirements and judge's orders.

- Public Record: Acts as an official record, validating the terms of the foreclosure sale.

- Financial Accountability: Supports transparency in foreclosure processes, providing accurate financial disclosures.

Important Terms Related to Foreclosure Return of Sale - No Proceeds

- Deficiency Judgment: A legal declaration that the sale did not meet the total debt owed.

- Commissioner's Return: Report by a court-appointed officer managing sale proceedings.

- Lienholder: The entity holding rights to the property's equity.

- Surplus Funds: Any remaining proceeds usually absent in no-proceed scenarios.

State-Specific Rules for the Foreclosure Return of Sale - No Proceeds

- Connecticut: Requires specified court forms, detailed procedural compliance, and deadlines in line with state civil procedures.

- Legal Variations: Adjustments based on jurisdictional mandates, emphasizing local law considerations in form preparation and submission.

Examples of Using the Foreclosure Return of Sale - No Proceeds

-

Connecticut Case Study: A property in Guilford sold for $150,000, while the mortgage debt was $200,000, leading to a foreclosure return with no available proceeds and a deficit condition.

-

Judicial Review Scenario: A court in Fairfield County reviews a foreclosure sale where competing lienholders are notified, and procedural justice requires a no-proceeds filing within a specific timeline.

Steps to Obtain the Foreclosure Return of Sale - No Proceeds

-

Visit Judicial Websites: Access relevant legal forms through the official websites of judicial departments.

-

Contact County Clerks: Request templates or guides directly from court offices or legal professionals.

-

Utilize Legal Platforms: Access documents via legal document management platforms such as DocHub for form previews and collaboration.

Penalties for Non-Compliance

-

Legal Repercussions: Potential for court sanctions, including fines or mandatory compliance sessions, if the filings are incomplete or untimely.

-

Financial Liabilities: Misreporting could result in financial penalties or return processes, demanding additional fees or repossession in severe cases.

Filing Deadlines and Important Dates

-

State-Specific Deadlines: Adherence to filing dates, subject to each state’s foreclosure processing schedule.

-

Court Mandated Timelines: Compliance with dates set forth by judicial officers overseeing foreclosure matters, ensuring procedural integrity.