Definition & Meaning

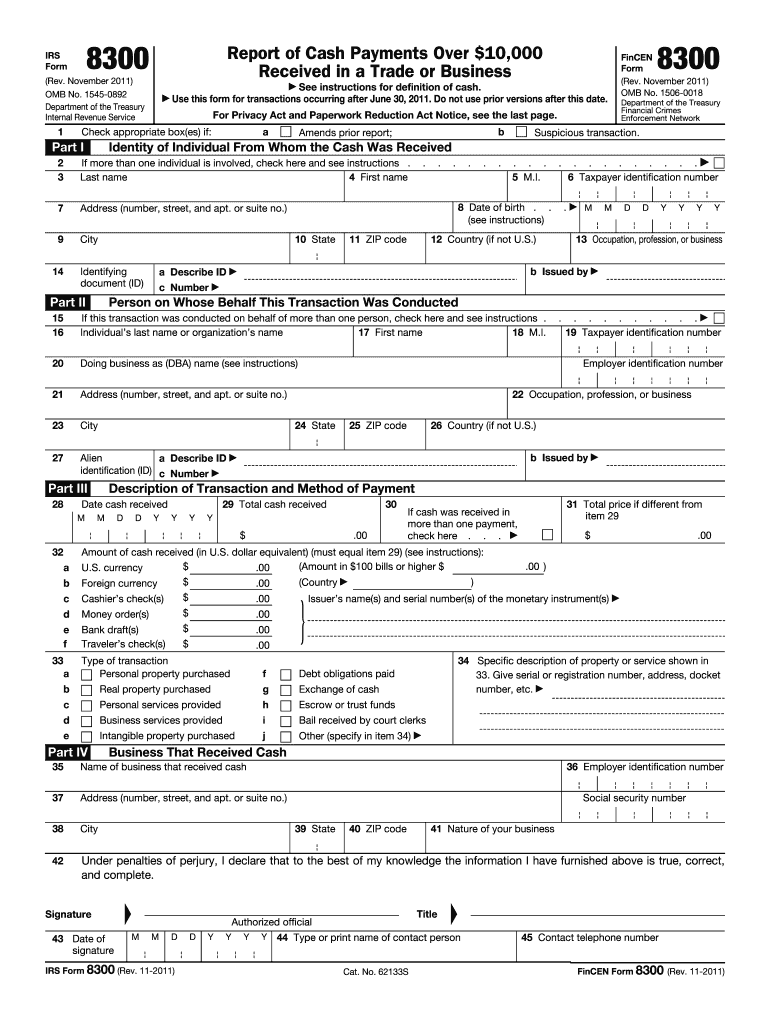

The IRS Form 8300 is a document used to report cash payments over $10,000 received in a trade or business. This form helps the Internal Revenue Service (IRS) and the Financial Crimes Enforcement Network (FinCEN) monitor large cash transactions to detect potential money laundering and tax evasion. Businesses that receive substantial cash payments must file Form 8300 to comply with federal regulations, thereby aiding law enforcement in its efforts to combat financial crime.

How to Use the Form 8300 (Rev July 2012) - Internal Revenue Service

Form 8300 is primarily used by businesses to report any cash transaction that exceeds $10,000 to the IRS. Businesses must provide detailed information about the payer and the transaction itself. The form is structured to capture essential details that help identify and scrutinize high-value cash exchanges. Primary areas of focus include the amount received, the date of the transaction, and the nature of the trade or business concerned.

Steps to Complete the Form 8300

- Payer's Information: Collect and input the customer's name, address, and taxpayer identification number.

- Business Information: Ensure your company's name and federal identification number are filled out correctly.

- Transaction Details: Specify the date and location of the transaction, as well as the amount received.

- Nature of Payment: Clarify if the payment was related to a loan, sale, insurance proceeds, or investment.

- Sign and Date: Confirm the accuracy of all information by signing and dating the form before submission.

IRS Guidelines

The IRS has established clear guidelines for filing Form 8300, emphasizing the importance of accurate and timely submission. Businesses are required to file the form within 15 days post-transaction. Failure to adhere to these guidelines can result in penalties. The IRS also offers guidance on what constitutes a reportable transaction, including multiple payments that aggregate to over $10,000 in a single event.

Filing Deadlines / Important Dates

Form 8300 must be filed within 15 days after the transaction date. It’s crucial for businesses to track cash payments meticulously to ensure compliance. If the 15-day deadline falls on a weekend or federal holiday, the deadline extends to the next business day. Filing late can attract penalties, highlighting the need for prompt action.

Penalties for Non-Compliance

Non-compliance with Form 8300 filing requirements can lead to significant penalties. Businesses may be fined if they fail to file the form on time, provide incomplete information, or neglect to notify the payer about the form’s filing. Penalties increase for businesses that intentionally disregard filing obligations, emphasizing the importance of compliance.

Examples of Penalties

- Late Filing: A penalty starting at $50 per form, escalating with continued non-compliance.

- Incomplete Form: Up to $100 for each form missing critical information.

- Intentional Disregard: Minimum penalty of $25,000 or the equivalent of the transaction amount, whichever is greater.

Digital vs. Paper Version

Form 8300 can be submitted either digitally or via paper. Digital submission is typically encouraged due to its efficiency and reduced chance for errors. Electronic filings can be done through the BSA E-Filing System, which provides a secure platform for submission. The paper version requires mailing to the appropriate IRS address, with the potential for longer processing times.

Software Compatibility

Filing Form 8300 electronically can be facilitated using various software platforms like QuickBooks or TurboTax. These platforms often include updated templates and can directly integrate with IRS systems, simplifying the process and ensuring accuracy. Businesses using such software must ensure they have the latest versions to accommodate any IRS changes to the form or filing procedure.

Required Documents

When filling out Form 8300, businesses should prepare relevant documentation to support the transaction details provided. This includes copies of payment receipts, customer identification forms, and transaction records. Keeping detailed records is essential not only for compliance but also for potential audits by the IRS.