Definition and Meaning

Excess and Surplus Lines Insurance refers to a specific segment of the insurance market that covers risks that standard insurance companies decline. This type of insurance is particularly relevant for beauty shops, barber shops, and day spas given the unique liabilities associated with these businesses. It provides coverage for situations that fall outside standard underwriting guidelines, allowing businesses to secure protection where they otherwise might face gaps.

- Unique Risks: Beauty shops, barber shops, and day spas may encounter specific risks such as accidental injuries from equipment or allergic reactions to products, which require specialized coverage.

- Higher Risk Acceptance: This form of insurance accepts risks that are typically not covered by traditional policies, which can be beneficial for businesses that face unusual circumstances or operate in unique niches.

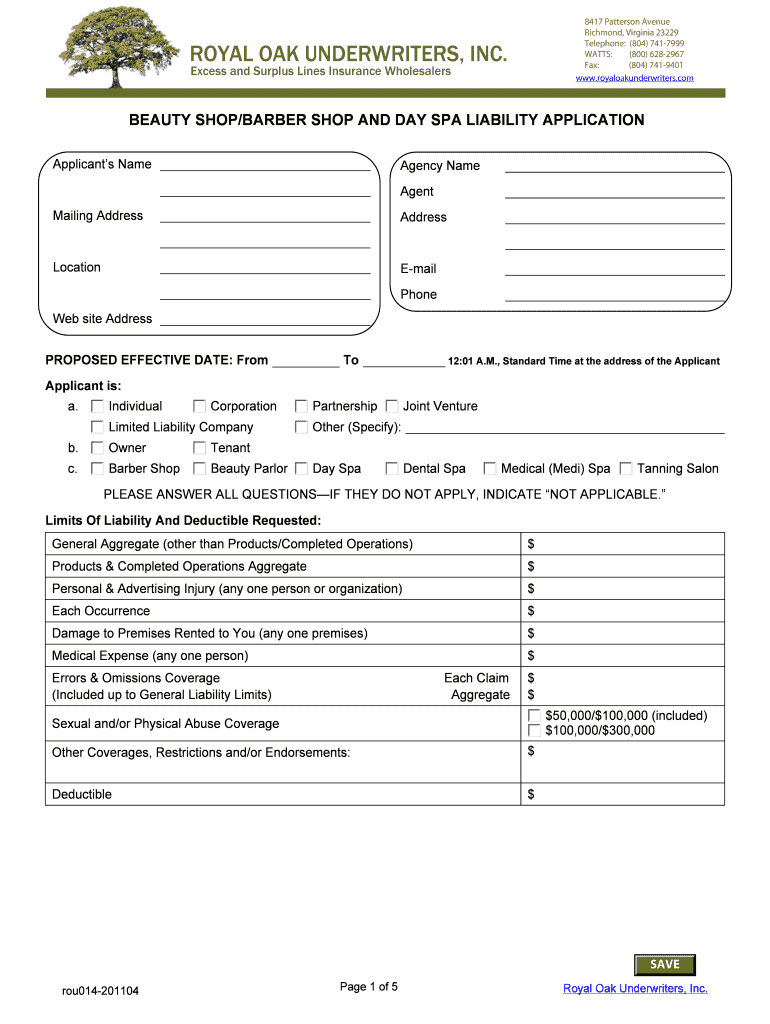

How to Use the Excess and Surplus Lines Insurance Wholesalers Beauty Shop Barber Shop and Day Spa Liability Application

The liability application form is a crucial tool for obtaining the necessary insurance coverage for salons and spas. To use this form effectively:

- Gather Information: Collect all pertinent business details, including ownership information, operational history, and any prior claims.

- Complete Each Section: Provide comprehensive answers in the application, including specific details about services offered and equipment used.

- Review for Accuracy: Ensure all information is correct to avoid any delays in processing or issues with coverage.

Steps to Complete the Excess and Surplus Lines Insurance Wholesalers Beauty Shop Barber Shop and Day Spa Liability Application

To fill out the application, follow these detailed steps:

- Applicant Information: Enter basic business contact information, including name and address.

- Business Details: Outline the services your business offers and any specializations.

- Insurance Coverage: Specify the limits and types of coverage you seek.

- Operational Questions: Answer questions about daily operations, staff qualifications, and safety protocols.

- Loss History: Detail any past claims or incidents to provide the insurer with a complete risk profile.

Important Terms Related to Excess and Surplus Lines Insurance

Familiarity with the terminology used in the application can streamline the process:

- Underwriting: The process by which insurers assess the risk they are being asked to cover and decide if they will provide coverage.

- Premium: The amount you pay for your insurance policy.

- Endorsement: An amendment to an insurance policy that changes the policy’s terms or coverage.

- Deductible: The amount a policyholder must pay out-of-pocket before the insurance company covers the remaining costs.

Key Elements of the Liability Application

To optimize the application, a thorough understanding of its key elements is crucial:

- Applicant Identification: Ensures that all basic business information aligns across all documents.

- Type of Coverage: Details the various coverage options that protect against industry-specific risks.

- Risk Assessment Factors: Information on safety protocols, staff training, and previous claims history to assess operational risks.

Legal Use of the Liability Application

The application serves as a legal document that ensures you receive appropriate coverage. Understanding its legal implications is important:

- Binding Contract: Upon approval and premium payment, the application becomes part of the insurance contract.

- Disclosure of Information: Full and honest disclosure is legally required to guarantee coverage validity.

- Fraud Warnings: Acknowledgment of potential penalties for submitting false or misleading information.

Eligibility Criteria

Understanding who qualifies for this form of insurance is essential:

- Types of Businesses: Primarily beauty and barber shops, and day spas.

- Risk Levels: Businesses with unique or high-level risks due to the services offered.

- Location: Businesses operated in specific states may have different eligibility requirements.

State-Specific Rules for Excess and Surplus Lines Insurance

Regulations can vary from state to state:

- State Filing Requirements: Ensure your business complies with local insurance regulations.

- Surplus Lines Broker Licensing: A surplus lines broker's involvement is often required for these policies due to state-specific legislation.

- Coverage Limits and Exclusions: Varying coverage limits and exclusions may apply depending on state laws.

Required Documents

Submit a complete package of supporting documents along with the application for a smooth approval process:

- Business Licenses: Proof of legitimate business operation.

- Financial Statements: Demonstrates business stability and risk levels.

- Safety Protocols: Documentation of safety measures in place to mitigate risks.

- Previous Insurance Policies: Provides context for past coverage and claims history.

Examples of Using the Liability Application

To illustrate how this liability application benefits businesses, consider these scenarios:

- New Business: A new day spa can use this application to secure insurance right from the start, ensuring protection against a broad spectrum of potential incidents.

- Established Beautician: An established salon could leverage the application to reassess their coverage needs and adjust their policy to cover new services they begin offering.

By understanding each of these elements in detail, businesses can effectively navigate the application process, improving their ability to secure comprehensive liability coverage tailored to their specific operational needs.