Definition and Meaning of ALTA Commercial Endorsements

The ALTA Commercial Endorsements are specialized amendments applied to title insurance policies. These endorsements are crafted by the American Land Title Association (ALTA) to provide additional coverage beyond the standard policy, tailored to commercial real estate transactions. They address various aspects such as zoning laws, access rights, and encroachments, offering protection against potential claims that might arise during property development or ownership. In essence, these endorsements ensure that the insured is safeguarded against specific risks not typically covered in the base title insurance.

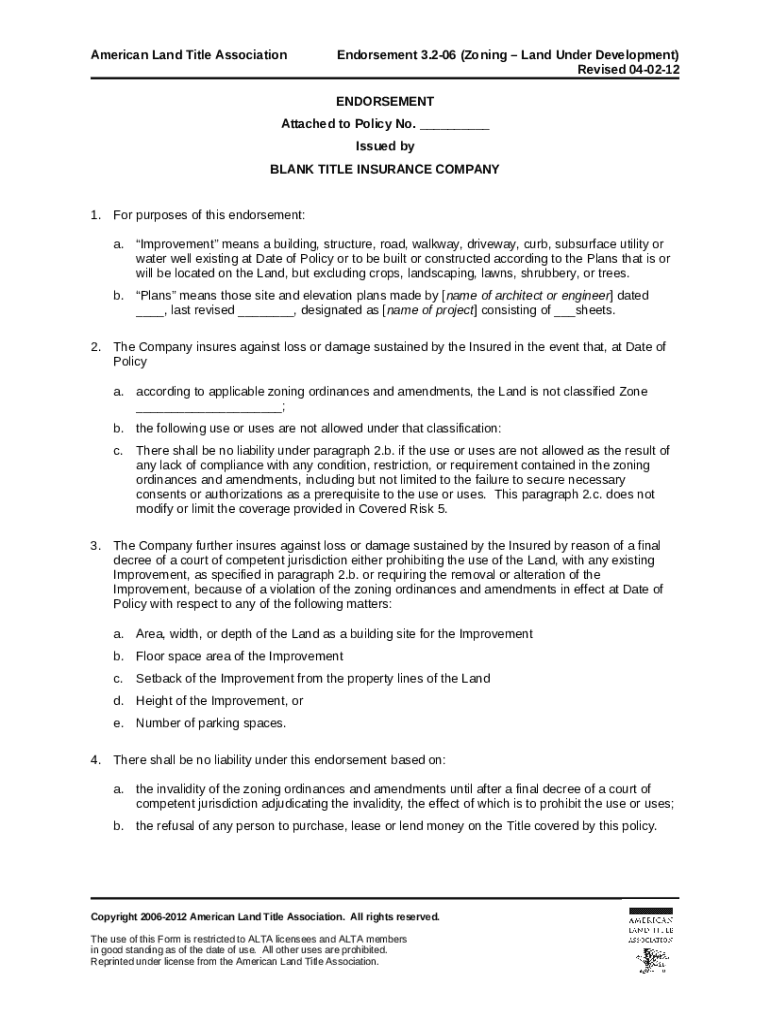

Examples of ALTA Commercial Endorsements

ALTA Commercial Endorsements can take multiple forms, each designed to address distinct real estate concerns. For instance:

- Zoning Endorsement (3.2-06): Provides assurance against losses due to zoning classification disputes.

- Access Endorsement (17-06): Covers loss or damage if there's no legal access to the property as stated in public records.

- Encroachment Endorsement (9-06): Protects against claims resulting from encroachments onto adjoining properties.

These are just a few examples that highlight the specific issues these endorsements can address, providing targeted risk management in commercial real estate transactions.

How to Use the ALTA Commercial Endorsements

Using the ALTA Commercial Endorsements involves understanding the risks associated with a property and selecting appropriate endorsements to mitigate those risks. Here's a step-by-step overview of the process:

- Identify Property Risks: Analyze the property's location, intended use, and surrounding environment to identify potential legal and regulatory challenges.

- Consult with a Title Insurer: Work with a qualified title insurance provider to discuss potential endorsements that align with identified risks.

- Select Relevant Endorsements: Choose the specific ALTA Commercial Endorsements that offer the necessary coverage for the anticipated risks.

- Review Terms Carefully: Examine the terms and conditions of each endorsement to understand coverage limits, exclusions, and requirements.

- Incorporate into Policy: Ensure the selected endorsements are formally incorporated into your title insurance policy.

Practical Application

Consider a commercial developer planning to build a shopping center. The developer would consult with their insurer to obtain relevant ALTA endorsements such as zoning and access, ensuring protection against zoning disputes or access issues that could impede construction or operation.

Key Elements of the ALTA Commercial Endorsements

The ALTA Commercial Endorsements contain several key elements designed to offer comprehensive protection:

- Definitions: Clear definitions for terms like 'Improvement' and 'Plans' are specified to outline what is covered.

- Coverage Provisions: Detailed descriptions of what losses or damages the endorsement will cover.

- Exclusions and Conditions: Specific conditions or scenarios where the endorsement will not apply or where liability is excluded.

- Legal Compliance: Assurance that the endorsement does not alter the primary insurance policy's terms, maintaining compliance with existing regulations.

Real-World Consideration

For instance, in a zoning endorsement, 'Improvement' may include any new constructions or alterations to existing structures. The policy provides coverage if zoning laws adversely affect these improvements.

Who Uses the ALTA Commercial Endorsements

The primary users of ALTA Commercial Endorsements are entities involved in commercial real estate transactions. This includes:

- Developers: Protect against potential issues that could affect project timelines and budget.

- Investors: Mitigate risks related to property value and usability.

- Lenders: Ensure their financial interests are secured against unforeseen title issues.

- Legal Professionals: Advise clients on the necessary endorsements to include in transactions.

Case Study

A real estate investment firm purchasing land for a new office park might use ALTA zoning and access endorsements to safeguard against zoning use disputes and guarantee essential property access routes.

Legal Use of ALTA Commercial Endorsements

These endorsements must be used in compliance with legal and regulatory requirements, ensuring they are applied correctly to protect both the insurer and the insured. The endorsements are restricted to use by ALTA licensees and members, ensuring standardization and reliability across all commercial transactions.

Compliance Scenarios

Legal professionals often guide clients on ensuring endorsements are used within the scope of federal, state, and local laws to avoid legal complications and maintain coverage validity.

Obtaining ALTA Commercial Endorsements

To obtain these endorsements, engage with a licensed title insurance provider. The process typically involves:

- Consultation: Discuss with the insurer to identify necessary endorsements.

- Documentation: Prepare and provide any required documentation related to the property.

- Review and Approval: Insurer reviews the request, and upon approval, issues the endorsements as part of the title insurance policy.

Steps in Practice

A commercial real estate broker may work closely with a title company to gather relevant property documents and negotiate necessary endorsements, ensuring a client's transaction proceeds with reduced risk.

State-Specific Rules for ALTA Commercial Endorsements

While ALTA sets the primary framework, individual states may have additional rules affecting the applicability and coverage scope of these endorsements. State-specific variations can arise from differences in local real estate laws, zoning regulations, and practice standards.

Examples of State-Specific Variations

- California: Stringent environmental regulations may necessitate additional environmental risk assessments.

- New York: Unique zoning laws could influence the provisions included in zoning endorsements.

Understanding these nuances is essential for ensuring endorsements are tailored effectively to meet local requirements.

Software Compatibility and Integration

Modern technology facilitates the integration of ALTA Commercial Endorsements into digital workflows, streamlining their application and management:

- Software Platforms: Many real estate software solutions are compatible with ALTA standards, facilitating easier management and tracking of endorsements.

- Cloud Storage Integration: Platforms like DocHub and Google Workspace can help in managing documents related to endorsements securely.

Technological Edge

Real estate professionals often leverage such software to ensure all documented endorsements are accessible, up-to-date, and aligned with client needs, enhancing efficiency and accuracy in real estate transactions.