Definition & Meaning

Form IT-251, Credit for Employment of Persons with Disabilities Tax Year 2024, is an essential tax form used primarily by employers in New York. It facilitates the claiming of tax credits provided under New York Tax Law Section 606(o) to incentivize the hiring and continuous employment of individuals with disabilities. This form enables employers to deduct a portion of the first and second-year wages paid to eligible employees, thus acting as a financial stimulus for supporting disabled persons in the workforce.

Key Components

- Eligibility Requirements: Details on which employees qualify as disabled under federal and state guidelines, often requiring certification from an accredited agency.

- Credit Calculation: Methods for computing credits based on qualified wages, typically split into first-year and second-year payments.

- Reporting Procedures: Instructions for documenting the claim on appropriate state tax returns.

Eligibility Criteria

For employers to utilize Form IT-251, they must ensure the employees in question meet specific definitions of disability and employment status. Important conditions include:

- Employee Certification: Employees must be certifiably disabled by recognized agencies, such as the Social Security Administration or New York's Department of Labor.

- Employment Duration: The individual must be employed for a minimum period corresponding to eligibility for first-year and subsequent second-year wage credits.

- Wage Requirements: Only wages paid during the first and second year of employment qualify for the credit calculation, focusing on incentivizing long-term hiring.

Steps to Complete the Form IT-251

Filling out Form IT-251 requires attention to detail to ensure compliance and eligibility. Here is a step-by-step guide:

- Gather Required Documents: Obtain employee certification, wage records, verification of employment duration, and other related documentation.

- Calculate Qualified Wages: Sum up the wages paid during eligible periods and check against thresholds for the first and second-year credits.

- Complete the Form Sections: Enter concise information in designated fields. Ensure clarity in employee information and employer identification sections.

- Attach Supporting Documents: Include necessary verifications and documentation to substantiate claims, as missing attachments can delay processing.

- Double-Check Accuracy: Re-evaluate entries for mathematical errors, omissions, or inconsistent data.

- Submit Compliantly: File the completed form using approved methods—either by mail, in-person, or electronically via New York's state tax submission systems.

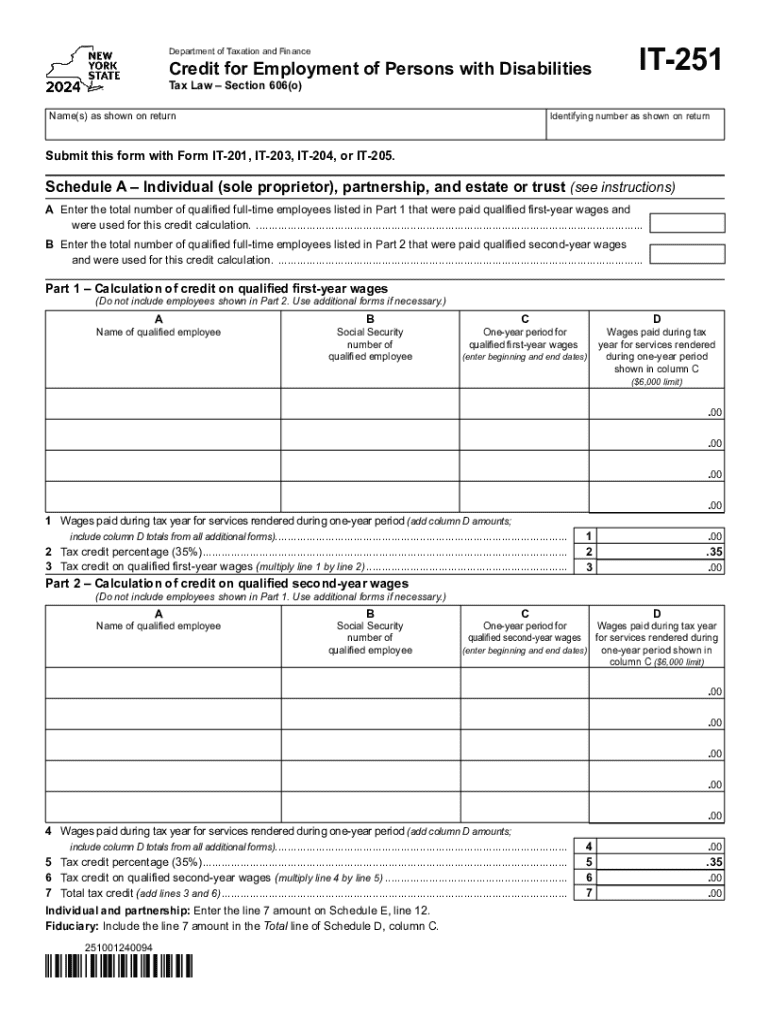

Key Elements of the Form IT-251

The form consists of several critical elements that ensure proper documentation and eligibility for the credit:

- Employer Identification Sections: Identifying information of the filing entity, including name, address, and tax identification numbers.

- Employee Information Fields: Data fields for each qualifying employee, including Social Security numbers, employment start dates, and related identifiers.

- Credit Calculation Areas: Spaces for computing the credit amounts based on specified wage conditions, separated into first and second-year calculations.

- Certification and Signatures: A section confirming that all information is accurate and complete, requiring a signature from an authorized representative of the business.

Filing Deadlines / Important Dates

Meeting the filing deadlines for Form IT-251 is critical to receiving tax credits without penalties. Typically, the form should be submitted by the employer's annual tax filing deadline. Key dates often include:

- Quarterly Filing Deadlines: Align with estimated tax payments if applicable for small businesses or varying fiscal years.

- Annual Filing Date: Often corresponds with the general New York income tax return deadline, typically mid-April.

- Extension Dates: If eligible, employers may file extensions but should ensure the form and accompanying documentation comply with adjusted deadlines.

Legal Use of the Form IT-251

Employers must strictly adhere to state guidelines when using Form IT-251. Engaging in fraudulent or inaccurate claims can result in:

- Legal Penalties: Enforcement actions by state tax authorities, resulting in fines or further legal action for non-compliance.

- Audit Risks: Increased likelihood of being audited, particularly if the credits claimed appear disproportionately large compared to the total workforce.

- Credit Denials: Inaccurate or fraudulent submissions could lead to outright denial of claimed credits and potential retroactive actions.

Examples of Using the Form IT-251

Illustrative scenarios where Form IT-251 is beneficial include:

- Small Businesses: A local shop employing three certified disabled workers can file for credits on wages capped during their first-year employment.

- Large Corporations: A multinational with a New York branch can benefit from the credits by fulfilling the necessary year-of-employment and wage criteria.

- Non-Profits: Organizations utilizing this form to claim credits as a means of enhancing inclusive employment practices in their communities.

State-by-State Differences

While Form IT-251 is designed for New York, variations may exist in other states with similar incentives or programs. Key points of comparison include:

- Credit Amounts: Differing maximum eligible credits may apply in states with similar programs.

- Eligibility Conditions: Variations in what constitutes a "qualified employee" could alter state-to-state requirements.

- Submission Protocols: Some states allow similar credits to be submitted electronically via centralized tax portals, differing from New York's filing process.