Definition and Meaning of Form IT-636

Form IT-636 is a tax form utilized for claiming the Alcoholic Beverage Production Credit in New York State for the tax year 2024. This form is integral for individuals, partnerships, and fiduciaries involved in the production of alcoholic beverages, allowing them to claim credit based on their production volumes. It details eligibility requirements and sets out specific thresholds for different types of beverages including beer, cider, wine, and liquor. The primary purpose of this form is to facilitate tax benefits for producers within the state, contributing to local industry growth.

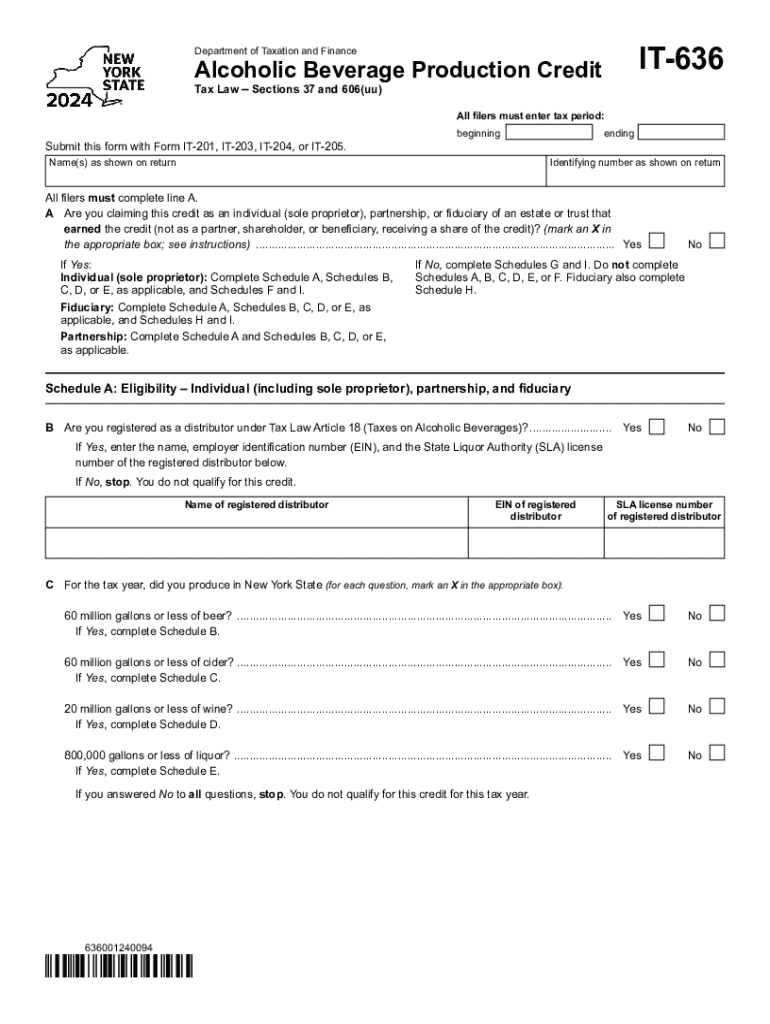

Eligibility Criteria

To qualify for the Alcoholic Beverage Production Credit using Form IT-636, applicants must meet specific production thresholds determined by New York State law. Eligibility is extended to several business types, including:

- Individuals: Solo producers who meet outlined production limits.

- Partnerships: Businesses with multiple stakeholders sharing in production responsibilities.

- Fiduciaries: Entities holding the responsibility of managing production on behalf of others.

Each applicant must produce within the set thresholds for beer, cider, wine, and liquor to qualify for different segments of the credit. Detailed computations based on these values are essential for accurate filing and credit calculation.

Key Elements of Form IT-636

Form IT-636 demands meticulous attention to various components:

- Production Volume Details: Applicants must meticulously document their production volumes for each type of beverage.

- Eligibility Verification: Ensures producers fall within stipulated thresholds.

- Schedule Completion: Detailed schedules help in calculating the accurate credit entitlement.

- Documentation: Records, invoices, and other proofs of production need to be comprehensively maintained and submitted with the form when required.

Steps to Complete Form IT-636

- Gather Necessary Documentation: Compile production records, invoices, and any related correspondence that prove eligibility and production volumes.

- Complete Personal and Business Information: Start by filling out the necessary personal and business details in the form.

- Calculate Production Volumes: Precisely compute and enter the production volumes of each alcoholic beverage.

- Fill Out Credit Schedules: Use provided schedules to calculate the credit amounts based on set thresholds and rates.

- Review & Verify Information: Double-check all entries for accuracy to avoid discrepancies.

- Submit Form with Supporting Documents: File the completed form along with required supporting documents through designated submission channels.

How to Obtain Form IT-636

The Form IT-636 can be accessed through the official New York State Department of Taxation and Finance website. It may also be available at local tax offices for in-person pick-up. Additionally, many tax software suites provide integrated access to the form for electronic filing.

Important Terms Related to Form IT-636

- Thresholds: Specific production limits set for different types of alcoholic beverages that determine qualification for the credit.

- Schedules: Sections within the form used for calculating exact credits based on production amounts.

- Fiduciary: An entity responsible for production management on behalf of others, such as an estate executor or trustee.

Filing Deadlines and Important Dates

Timely submission of Form IT-636 is critical. The form must be filed in alignment with the applicant’s annual tax filing deadline, which typically falls on April 15th unless extensions are granted. It is important to stay aware of any state-specific tax announcements that might affect these deadlines.

Penalties for Non-Compliance

Failure to accurately complete and submit Form IT-636 can lead to several consequences:

- Denial of Credit: Incorrect or incomplete submissions may result in disqualification from receiving the credit.

- Financial Penalties: Late submissions or discovered inaccuracies could incur fines or interest on unpaid tax amounts.

- Audits and Legal Action: Severe discrepancies may prompt state audits or lead to legal enforcement actions.

Software Compatibility for Form IT-636

Most major tax software programs, including TurboTax and QuickBooks, incorporate the Form IT-636 for ease of filing. These platforms often guide you through the eligibility and credit calculation process, ensuring compliance with state requirements while streamlining the document preparation process.