Definition and Meaning of IT-204-CP

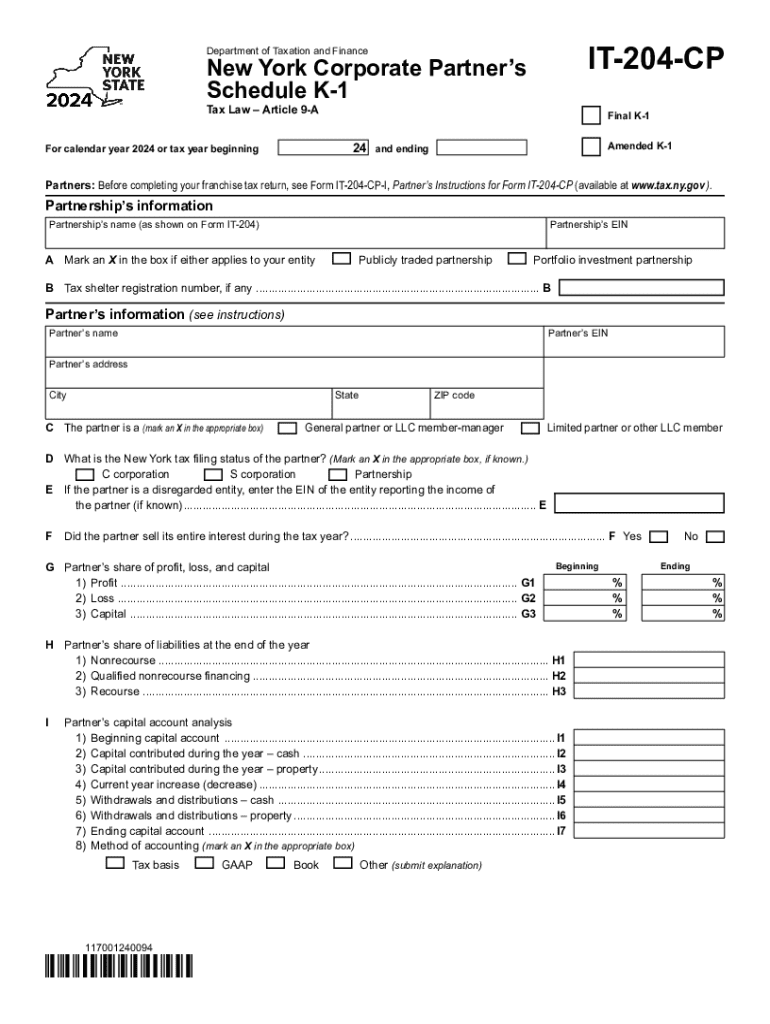

The IT-204-CP is the Schedule K-1 for corporate partners in New York, specifically for the tax year 2024. It is a document that discloses an individual corporate partner's share of profits, losses, and other relevant tax items within a partnership. This form ensures corporate partners accurately report their income on state tax returns by detailing allocations that fall under New York's distinct tax legislation.

Key Components

-

Partnership Information: Provides essential data about the partnership, including names and identifying numbers.

-

Partner Information: Details about the corporate partner, its address, and tax identification number, helping differentiate tax obligations.

-

Profit and Loss Allocations: Specifies the corporate partner’s share of income, deductions, credits, and other ventures from the partnership.

-

Capital Account Analysis: An assessment of the corporate partner's starting balance, contributions, distributions, and closing balance for the tax year.

Steps to Complete Form IT-204-CP

Completing the IT-204-CP properly is crucial for accurate tax reporting. Follow these steps:

-

Gather Necessary Documents: Collect prior year forms, financial statements, and any relevant partnership agreements.

-

Enter Partnership Details: Include partnership name, address, and federal identification number.

-

Fill Out Partner’s Details: Supply corporate partner's legal name, address, and tax ID.

-

Report Profit and Loss: Accurately allocate the corporate partner’s share of income, losses, and credits as outlined by the partnership.

-

Update Capital Account: Provide details of any changes in the capital account including additional capital contributions or distributions.

-

Review and Submit: Ensure all entries are correct, sign the form if needed, and submit by the deadline.

Who Typically Uses the IT-204-CP

The IT-204-CP is predominantly used by corporate partners involved in partnerships based in New York. These entities commonly include:

-

Corporations: Required to report partnership income, gains, losses, and credits via this schedule.

-

Multinational Companies: Often involved in numerous partnerships necessitating thorough documentation of profit allocations.

-

Investment Firms: Engage in collaborative ventures that mandate precise income reporting through partnership filings.

Important Terms Related to IT-204-CP

Familiarity with key terminology is essential for accurately completing the form:

-

Capital Contributions: Investments made into the partnership by the corporate partner during the tax year.

-

Allocable Share: The determined portion of the partnership's income or losses allocable to the corporate partner.

-

Preferred Return: A priority payment to the corporate partner before any distributions of remaining profits to other partners.

Practical Examples of Use

-

Case Scenario 1: A corporation holding a 20% interest in a real estate partnership uses IT-204-CP to declare its distributive share of rental income and specific property depreciation.

-

Case Scenario 2: An investment group incorporated in NY uses this form to document interest income allocations received through various investment undertakings as part of a consortium.

Filing Deadlines and Important Dates

Adherence to deadlines is necessary to avoid penalties:

-

Submission Deadline: Typically aligns with your federal tax return due date, often April 15th, unless extended.

-

Extensions: Partnerships may file for an extension, allowing extra time, generally until October 15th, to submit.

-

Amendment Period: Any corrections to the form should be made within the statute of limitations for filing a claim for a refund.

Form Submission Methods

Partnerships have multiple options for submitting the IT-204-CP:

-

Electronic Filing: Preferred for speed and convenience, can be done directly through tax software.

-

Mail: Hard copy submissions are permissible but must be postmarked by the due date.

-

In-Person: Rarely utilized, but available at certain state tax office locations.

Legal Use and Compliance with IT-204-CP

Understanding the legal implications is vital:

-

Compliance: Aligns with both New York State tax law and the Internal Revenue Code.

-

Auditing: Maintain all related records as the Department of Taxation and Finance may audit partnerships.

-

Penalties for Non-Compliance: Include late filing fees, possible interest on taxes due, and other penalties as determined by New York tax authority.

State-Specific Rules for IT-204-CP

This form reflects unique New York state requirements, vital for compliance:

-

New York Modifications: Must account for varying state-specific deductions, exclusions, and credits not present at the federal level.

-

Apportionment Factors: New York might necessitate a more nuanced approach to income apportionment, uniquely impacting the IT-204-CP.

-

Notification Requirements: Some partnerships need to inform state agencies about certain transactions impacting tax liabilities.

By understanding and correctly applying these elements, corporate partners ensure compliance with New York tax laws, avoid penalties, and clearly ascertain their share in a partnership’s financial outcomes for the tax year 2024.