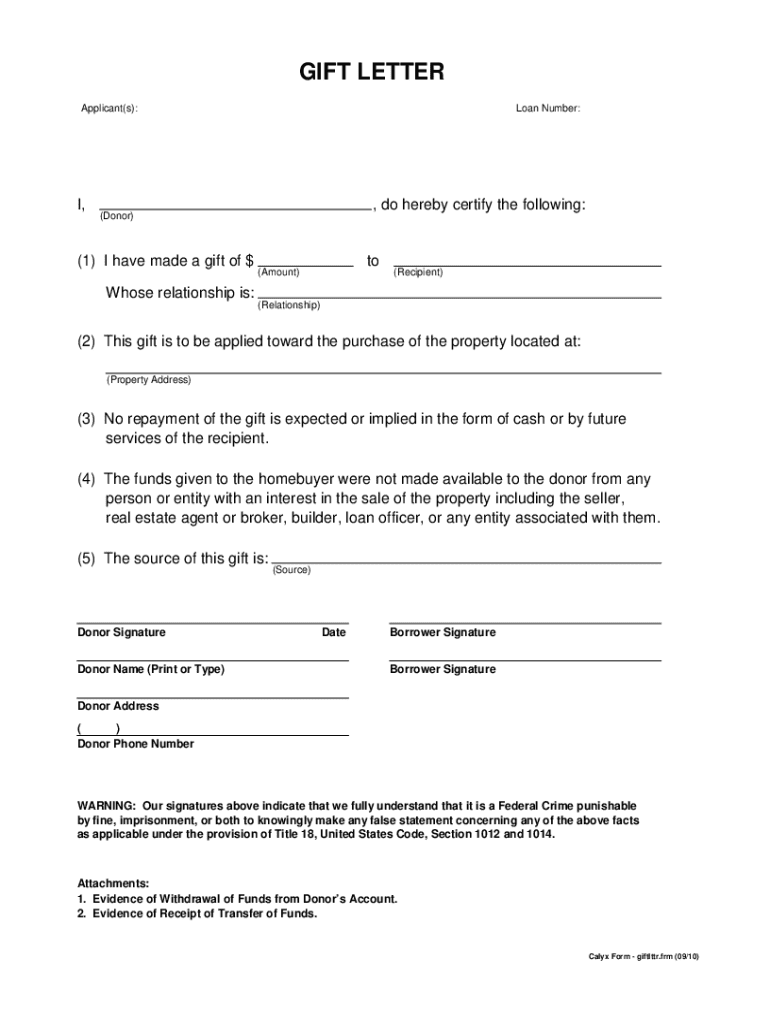

Definition & Purpose of a Gift Letter for Your Mortgage

A gift letter for your mortgage is an essential document used in the home buying process when a borrower receives a monetary gift from a donor, typically a family member, to contribute to the down payment. This letter serves several purposes. Primarily, it confirms that the gift is not a loan and does not need to be repaid, which might otherwise affect the borrower’s debt-to-income ratio. It clearly states that the funds are given freely, without any obligation for repayment, ensuring transparency in financial transactions related to the mortgage.

The letter customarily includes specific details, such as the donor's name, the donor's relationship to the borrower, the exact amount of the gift, and a statement that no repayment is expected. This documentation helps clarify the source of funds, satisfying underwriter requirements and strengthening the borrower's application for mortgage approval.

Key Components of a Gift Letter

A comprehensive gift letter should contain several key elements to ensure it fulfills its purpose effectively. These components include:

- The donor's and recipient's full names and contact information: Precise identification of the involved parties is critical.

- A statement of the donor's relationship to the recipient: This element is important for validating eligibility, as most lenders require the donor to be a family member.

- The exact amount of the gift: It is essential to specify the monetary value to prevent confusion or discrepancies.

- A declaration of no repayment expectation: This clarifies that the donation is not a loan, eliminating concerns of additional financial liabilities for the recipient.

- Details of the account used to transfer the gift: Providing evidence of the funds being transferred, such as a bank statement, enhances transparency and credibility.

- Signatures of both the donor and the recipient: To validate the agreement and the authenticity of the document, both parties must sign it.

Step-by-Step Instructions to Complete a Gift Letter

Writing a gift letter for your mortgage involves careful attention to detail. Follow these steps to ensure the letter meets lender requirements:

- Begin with a formal header: Include the date, the lender's name, and contact information.

- Clearly state the donor's information: Provide full name, address, phone number, and relationship to the borrower.

- Draft the formal statement: Specify the gift amount, reason for the gift, and explicitly mention that the gift does not require repayment.

- Include the recipient's details and mortgage information: State the borrower’s name, the mortgage account number, and the property address.

- Attach supporting documentation: Include proof of the fund transfer, such as bank statements, to verify the transaction.

- Conclude with signatures: Secure the donor’s and recipient’s signatures and print their names beneath for clear identification.

Legal Use and Implications

Gift letters legally affirm that no repayment is expected. This is crucial because undisclosed loans could disqualify a borrower when underwriters assess their capacity to repay the mortgage. Misrepresentation in a gift letter can lead to legal consequences for both the donor and recipient, including potential fraud charges. It is important to ensure that all information provided is accurate, complete, and truthful.

State-Specific and Lender-Specific Requirements

While the basic structure of a gift letter is generally consistent, there may be state-specific or lender-specific requirements to be aware of.

- State regulations: Some states may have specific stipulations on who can be a donor or how documentation should be presented.

- Lender requirements: Individual lenders might request additional details or documentation proofs beyond the standard components of a gift letter.

Always verify with your specific lender or legal advisor if any additional conditions need to be met to adhere to local real estate laws and institutional policies.

Common Examples and Scenarios

Gift letters are utilized in various scenarios where external financial assistance is provided for a mortgage. Some common examples include:

- Parental support: A parent gifts their child money for a first-home purchase.

- Marriage gifts: Newlyweds receive financial support from family members to buy a shared property.

- Retirement assistance: Family members contribute to a retiree's down payment to relocate closer to family.

These instances highlight the personal and relational nature of gift letters, reinforcing their role in facilitating family-assisted property transactions.

Potential Penalties for Non-Compliance

Failing to comply with proper gift letter protocols can lead to severe penalties. These may include:

- Mortgage denial: Incorrect or incomplete documentation could lead to the rejection of the entire application.

- Legal repercussions: Fraudulent claims or undisclosed loans can result in legal action against both parties.

- Revised loan terms: Lenders might alter loans terms if undisclosed debts are discovered.

Understanding the implications of non-compliance stresses the importance of accuracy and transparency in drafting a gift letter.

Importance and Benefits of Gift Letters

Gift letters play a pivotal role in helping individuals and families secure their dream homes when personal savings fall short. They provide:

- Validation for lenders: Ensure lenders that the down payment funds are secure and legitimate.

- Financial support for recipients: Aid borrowers in accessing required funds without acquiring new debt.

- Facilitation of property purchases: Allow for timely transactions by bridging financial gaps.

By using a gift letter, you facilitate a smoother home-buying process while maintaining compliance with lending standards.