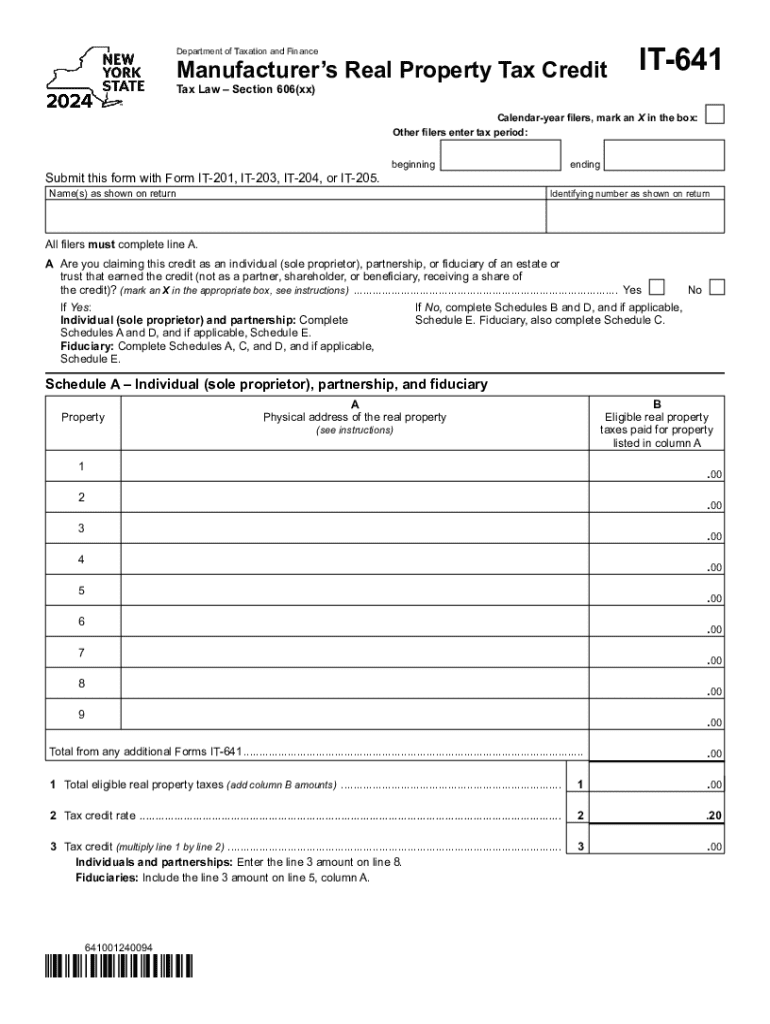

Definition and Purpose of Form IT-641 for Tax Year 2024

Form IT-641, the Manufacturer's Real Property Tax Credit, is established under New York Tax Law Section 606(xx). It is a tax form used by manufacturers operating within New York State to claim a credit on real property taxes. This credit aims to alleviate the tax burden on businesses that own or lease manufacturing property in the state, thereby promoting economic growth and competitiveness. Manufacturers can use this credit to reduce their state tax liability, provided they meet specific eligibility criteria.

Eligibility Criteria for Form IT-641

To qualify for the Manufacturer's Real Property Tax Credit, entities must fall under New York Tax Law's definition of a manufacturer. Eligible manufacturers must own or lease real property in New York that is actively used for manufacturing. Key criteria include:

- The property must be predominantly used for manufacturing activities.

- The business must be classified per NAICS codes that define manufacturing.

- Entities like corporations, partnerships, and fiduciaries can apply, provided they conduct qualifying operations.

It is crucial for businesses to verify their eligibility before applying to avoid penalties and improper claims.

Steps to Complete Form IT-641

Successfully completing Form IT-641 requires precise adherence to instructions tailored for individual, partnership, or fiduciary filers:

- Gather Required Information: Collect documentation related to real property taxes paid during the tax year.

- Determine Eligible Property: Verify that all listed properties meet the criteria for manufacturing use.

- Calculate Credit: Follow the form's instructions to accurately calculate the tax credit.

- Complete Applicable Sections: Fill out sections relevant to the entity type (individual, partnership, or fiduciary).

- Review and Submit: Proofread for accuracy and completeness, then submit via the appropriate submission method.

Following these steps ensures compliance and maximizes the chance of a successful application.

Important Terms Related to Form IT-641

Understanding the terminology associated with Form IT-641 is vital for accurate completion:

- Real Property Tax: Taxes levied on real estate by local governments, essential for calculating eligible credits.

- NAICS Codes: Numerical system used to classify businesses by industry, identifying eligible manufacturers.

- Tax Liability: The total amount of tax owed by an entity; the credit directly reduces this amount.

Clear comprehension of these terms can prevent errors and omissions in form filing.

State-Specific Rules for New York's Tax Credit

New York has unique guidelines for claiming the Manufacturer's Real Property Tax Credit. Registrants must adhere to state-specific provisions:

- Exclusive Benefit to New York Manufacturers: Only entities operating within New York can claim this credit.

- Supporting Documentation Required: Proof of property usage and tax payments must be maintained and submitted if requested.

- Annual Reapplication: Businesses must apply each tax year; credits are not automatically renewed.

These rules emphasize New York's commitment to fostering a manufacturing-friendly environment.

Form Submission Methods for IT-641

Form IT-641 can be submitted through various channels, offering flexibility for different taxpayer needs:

- Online Filing: Using New York State's online tax filing systems is often the most efficient method.

- Mail: Traditional submission via mail is an option; ensure postmarked by the deadline.

- In-Person: For those preferring direct interaction, in-person submissions can be made at designated tax offices.

Choosing the optimal submission method can reduce processing time and potential errors.

Filing Deadlines and Important Dates

Timeliness is crucial when dealing with tax credits:

- Filing Deadline: Typically aligns with the business's state tax return due date, with extensions possibly available.

- Payment Confirmation: Ensure that all real property taxes eligible for credit are paid by the end of the tax year.

Meeting these deadlines ensures the credit is applied to the current tax year, aiding in financial planning and cash flow management.

Reporting Requirements and Documentation for Form IT-641

Accurate and complete reporting enhances the credibility of the tax credit application:

- Real Property Tax Bills: Must provide copies as evidence of payment.

- Proof of Manufacturing Activity: Operations documentation to verify that the property aligns with manufacturing criteria.

- Entity Details: Full disclosure of company information and tax identification numbers.

Maintaining organized records is crucial for verification and audit processes.

Legal Use and Compliance for Form IT-641

Proper use of Form IT-641 ensures compliance with New York Tax Law:

- Audit Preparedness: Entities claiming the credit should stay prepared for potential audits by maintaining detailed records.

- Legitimate Claim: Only legitimate manufacturing properties and tax payments qualify for credit.

Compliance safeguards against future legal and fiscal complications, ensuring the smoother operation of the business's financial obligations.