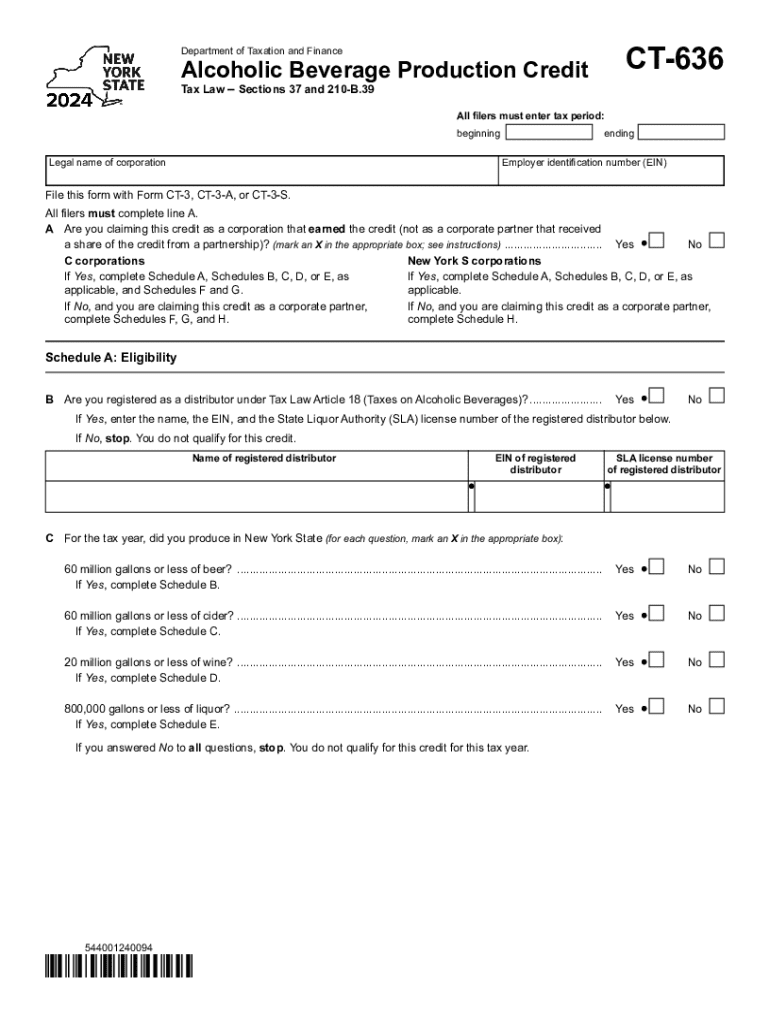

Definition and Purpose of Form CT-636 Alcoholic Beverage Production

Form CT-636 is designed to facilitate New York corporations in claiming the Alcoholic Beverage Production Credit. This tax credit is applicable specifically to corporations involved in producing alcoholic beverages such as beer, cider, wine, and liquor. By using this form, businesses can calculate the credit owed based on their production levels, thus potentially lowering their tax liability. Understanding the purpose and application of this form is crucial for businesses aiming to maximize their eligible tax benefits.

Steps to Complete Form CT-636

- Gather Required Information: Collect all necessary data, including corporate identification details, tax periods, and production figures for alcoholic beverages.

- Calculate Production Levels: Determine the amount of beer, cider, wine, or liquor produced in the tax year. This information will directly impact the credit calculation.

- Fill Out Each Section: Complete the multiple sections of the form, ensuring that each part accurately reflects the production and financial data.

- Review for Accuracy: Double-check all entries to verify accuracy; any mistakes could delay processing or result in incorrect credit calculations.

- Submit the Form: Once completed, submit the form according to the preferred method, ensuring it meets the filing deadlines to avoid penalties.

Eligibility Criteria for Form CT-636

The eligibility to claim the Alcoholic Beverage Production Credit through Form CT-636 is primarily extended to New York corporations engaged in producing alcoholic beverages. Key criteria include:

- Location: The production facility must be situated within New York State.

- Type of Beverage: Eligible beverages are limited to beer, cider, wine, and liquor.

- Volume of Production: There might be thresholds or caps on the production volume eligible for credits, so verifying these details is essential.

Legal Use of Form CT-636

Utilizing Form CT-636 appropriately requires understanding its legal implications. Companies must ensure compliance with New York State tax laws, accurately report their manufacturing activities, and retain supporting documentation to substantiate the credit claimed. Proper legal use of the form also involves adhering to the submission timeline and verifying that any amendments to tax legislation have been incorporated into the form's completion.

Important Terms Related to Form CT-636

- Tax Credit: A reduction in tax liability due to specific qualifying expenditures on alcohol production.

- Qualified Production Facility: The facility must meet certain standards and regulations to be eligible.

- Filing Period: The designated timeframe when the form must be submitted for the tax credit to be claimed for that year.

Filing Deadlines for Form CT-636

Timeliness in filing Form CT-636 is crucial to avoid potential penalties. Generally, the form should be submitted alongside the business's annual tax return. Filing deadlines will align with New York State corporate income tax deadlines, typically due within 30 days of filing the federal return. Companies should verify any specific dates applicable for the current fiscal year to ensure compliance.

Examples of Using Form CT-636

To illustrate effective use, consider a mid-sized brewery in New York with a production line dedicated to craft cider. By meticulously tracking their production output and utilizing Form CT-636, the brewery is able to claim significant tax credits for their beverage production, aiding in their expansion and operational scaling. Another scenario involves a winery maximizing its eligible tax savings by claiming credits for both wine and spirits produced within the state.

State-Specific Rules for Form CT-636

New York imposes specific regulations governing the usage of Form CT-636. These rules may include stipulations on the percentage of locally sourced materials used in production or compliance with state manufacturing laws. Additionally, businesses should be aware of any updates or changes in tax legislation that could impact their eligibility or credit calculations.

Key Elements of Form CT-636 Instructions

The instructions accompanying Form CT-636 provide detailed guidance on accurate completion. Key components include:

- Line-by-Line Instructions: Guides for each section of the form, detailing what information is required.

- Computation of Credits: Specific methods to calculate the credits based on production.

- Supporting Documentation: Lists of documentation needed to substantiate claims, such as production logs and financial statements.

Software Compatibility and Related Tools

Companies utilizing Form CT-636 can leverage various software solutions to streamline the filing process. Programs like QuickBooks or TurboTax can facilitate data collection, organize financial records, and ensure accuracy in reporting. Integration with accounting software ensures seamless data transfer, reducing manual entry errors and saving time.