Definition and Meaning

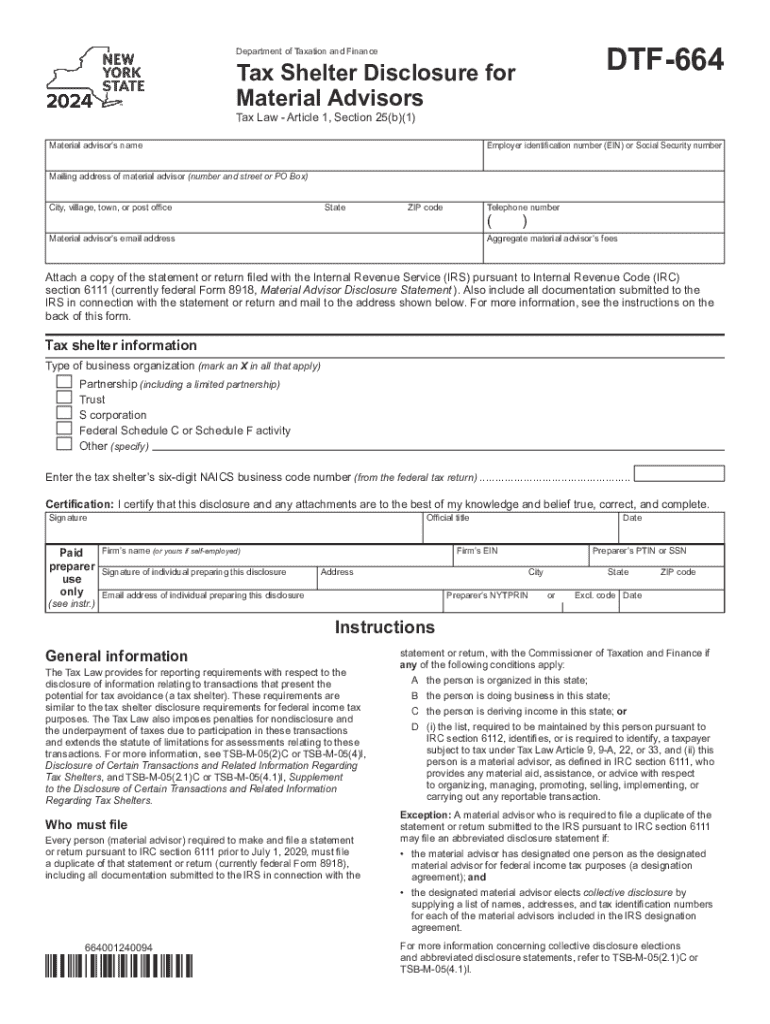

The Form DTF-664 Tax Shelter Disclosure for Material Advisors Tax Year 2024 is a mandatory documentation for material advisors involved in reportable transactions that could potentially result in tax avoidance. This form serves as a declaration to the New York State Tax Department, ensuring that the advisor's dealings are in compliance with tax regulations. The aim is to increase transparency and reduce the potential for tax evasion schemes. Advisors must report specific details about the transactions, their role, and any potential outcomes that could influence tax obligations.

How to Use Form DTF-664

Material advisors use Form DTF-664 when disclosing transactions that meet specific IRS criteria for reportable transactions. To properly utilize the form, advisors should:

- Identify Reportable Transactions: Determine if the transaction requires disclosure based on its characteristics and potential tax implications.

- Gather Necessary Information: Compile comprehensive details about the transaction, including involved parties, transaction structure, and anticipated tax outcomes.

- Complete Form Accurately: Fill out each section of the Form DTF-664 with meticulous attention to accuracy, particularly regarding transaction details and advisor information.

- Submit as Required: Provide the completed form to the New York State Tax Department, ensuring it aligns with both federal and state regulations.

Steps to Complete Form DTF-664

To effectively complete Form DTF-664, follow these steps:

- Review Instructions: Prior to filling out the form, thoroughly review the instructions to understand what constitutes a reportable transaction.

- Advisor Information: Enter personal and professional details, including name, address, and Preparer Tax Identification Number (PTIN).

- Detail Transaction Information: Accurately describe the transaction, specifying the nature, involved parties, and expected tax implications.

- Affix Signature: Sign and date the form to certify that all information provided is true and correct to the best of your knowledge.

- Retain Copies: Keep a duplicate of the completed form for your records, as you may need to refer back to it for audits or future filings.

Disclosure Requirements and Penalties

Material advisors are compelled to disclose their involvement in certain reportable transactions to ensure compliance with IRC section 6111. Failure to disclose these transactions or provide false information can lead to penalties. These penalties can be substantial, including financial fines and potential legal consequences. It is crucial for advisors to adhere strictly to disclosure requirements to avoid such repercussions.

Who Typically Uses Form DTF-664

The form is predominantly used by material advisors who participate in certain transactions that could potentially shelter income from taxation. This includes tax professionals, accountants, and legal advisors who facilitate these transactions as part of their services. Businesses engaging with these advisors for transaction structuring also rely on disclosures to maintain compliance.

Key Elements of Form DTF-664

- Advisor Information: Identifies the material advisor responsible for the transaction.

- Transaction Details: Outlines the specifics of the transaction, including the nature, purpose, and expected tax outcomes.

- Compliance Certification: The advisor certifies that the information provided is accurate and complete.

Important Dates and Filing Deadlines

Advisors must be attentive to critical deadlines to ensure the timely filing of Form DTF-664. Generally, the form must be submitted to the New York State Tax Department by a specific date following the transaction. Missing these deadlines can lead to penalties. It is advisable to record important dates and plan submissions ahead of time.

Form Submission Methods

Form DTF-664 can be submitted using various methods:

- Online Submission: Some states and entities may offer electronic filing options, facilitating streamlined and efficient submission processes.

- Mail Submission: Physical copies can be mailed directly to the New York State Tax Department.

- In-Person Delivery: Hand-delivery may be an option in certain jurisdictions, allowing for direct interaction and immediate feedback.

Penalties for Non-Compliance

Failure to comply with the obligations associated with Form DTF-664 can result in significant penalties. Advisors may face fines for nondisclosure, inaccurate reporting, or late submission. Furthermore, non-compliance can attract scrutiny and potential legal action, emphasizing the importance of accuracy and timeliness in filing.

State-Specific Rules

Each state may have additional rules and regulations concerning the disclosure of tax shelters. In New York, compliance with state-specific guidelines in conjunction with federal regulations is crucial. Material advisors must be aware of these differences to ensure both state and federal obligations are met.