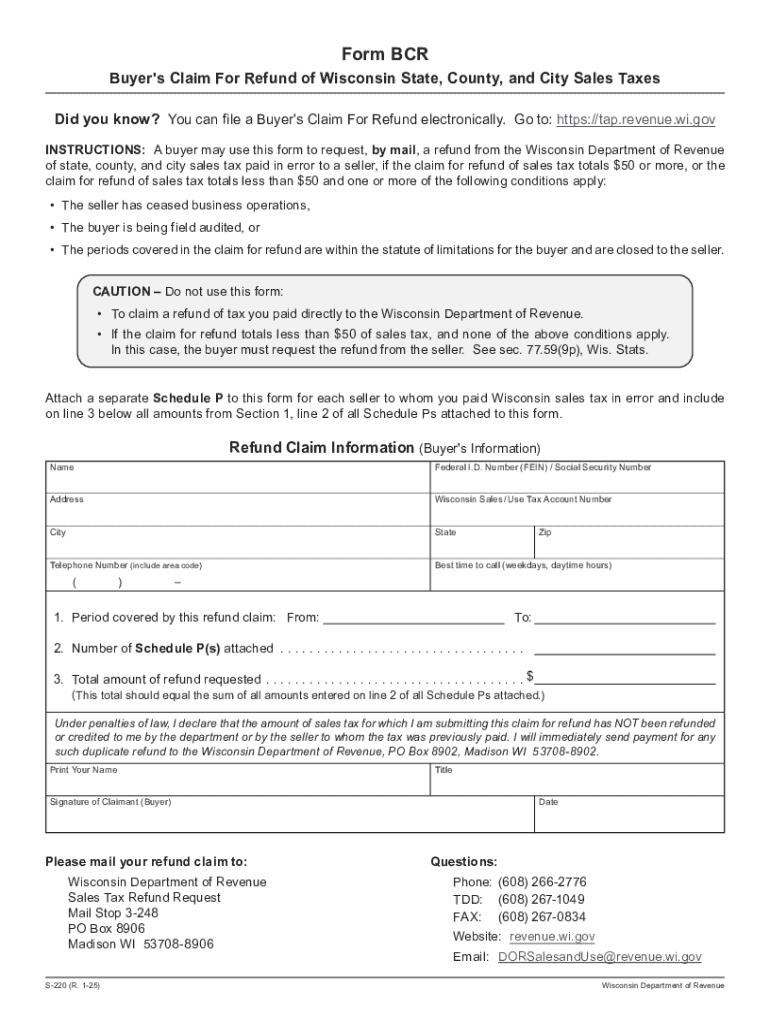

Definition & Meaning

The January 2025 S-220 Form BCR is specifically designed for buyers seeking a refund on sales taxes paid within Wisconsin. These taxes may include state, county, and city sales taxes applicable at the time of purchase. The form essentially allows individuals and businesses to reclaim funds paid erroneously or excessively on qualifying transactions. This is particularly relevant when purchases are exempt from sales tax, but tax was still collected at the point of sale.

How to Use the January 2025 S-220 Form BCR

To effectively utilize the form, applicants must accurately report personal information, outline the nature of their refund claim, and offer supporting documentation. Detailed record-keeping is crucial, including receipts and proof of tax paid, to substantiate claims. The form also requires applicants to detail each transaction on a seller-specific basis, ensuring transparency and accuracy in the process.

Steps to Complete the January 2025 S-220 Form BCR

-

Gather Documentation: Collect all sales receipts and proof of payment showing sales tax charges.

-

Fill Personal Information: Provide your name, address, and tax identification number, ensuring all details align with tax records.

-

Specify Refund Details: Clearly explain each purchase’s tax refund claim, including seller details and the specific tax amounts paid.

-

Attach Schedules: For multiple sellers, attach schedules outlining individual claims for each seller.

-

Review and Submit: Double-check all entries for accuracy before mailing the form to the specified tax authority address.

Eligibility Criteria

Eligibility for a sales tax refund is contingent upon several factors, including the classification of the buyer and the nature of goods or services purchased. Claims under $50 are subject to simplified submission processes, while exemptions for certain goods like raw materials often qualify for refunds if incorrectly taxed.

Key Elements of the January 2025 S-220 Form BCR

Key components of the form include sections for personal identification, transaction details, and declarations of refund claims. Each part requires accurate and comprehensive data input to avoid discrepancies or rejection. The form also necessitates attachments, such as itemized purchase receipts and detailed descriptions of the tax amounts in question.

State-Specific Rules for the January 2025 S-220 Form BCR

Wisconsin has unique stipulations regarding sales tax claims, including regulations on refund timeliness and documentation requirements. Claimants must also be aware of Wisconsin's distinct tax classifications affecting eligibility, like specific exemptions for non-profits or educational institutions.

Form Submission Methods

The S-220 Form BCR can be submitted through various avenues:

-

Online Submission: Ensures faster processing and may offer step-by-step guidance through an electronic portal.

-

Mailing In: Traditional submission via postal service, requiring thorough documentation to be enclosed.

-

In-Person Submission: Direct delivery to a state tax office, allowing for immediate confirmation of receipt.

Required Documents

Mandatory documents include copies of relevant receipts, proof of purchase, seller agreements outlining tax collection, and identification documentation. These will bolster the claim’s authenticity and facilitate a smoother review process by the tax authorities.

Filing Deadlines / Important Dates

Applicants must be conscientious of state-imposed deadlines for tax refund filings to prevent forfeit. Typically, these deadlines align with annual tax reporting dates; however, distinct circumstances such as amendments may have extended timelines. It's imperative to verify specific submission cutoffs for each tax year to ensure compliance and eligibility.

Legal Use of the January 2025 S-220 Form BCR

The form is legally binding, requiring claimants to provide truthful information under penalty of perjury. Misrepresentation or fraudulent claims can result in legal action, fines, or penalties. Proper and ethical use of the form is crucial not only for personal integrity but also to uphold systemic fairness in tax administration.