Definition & Meaning

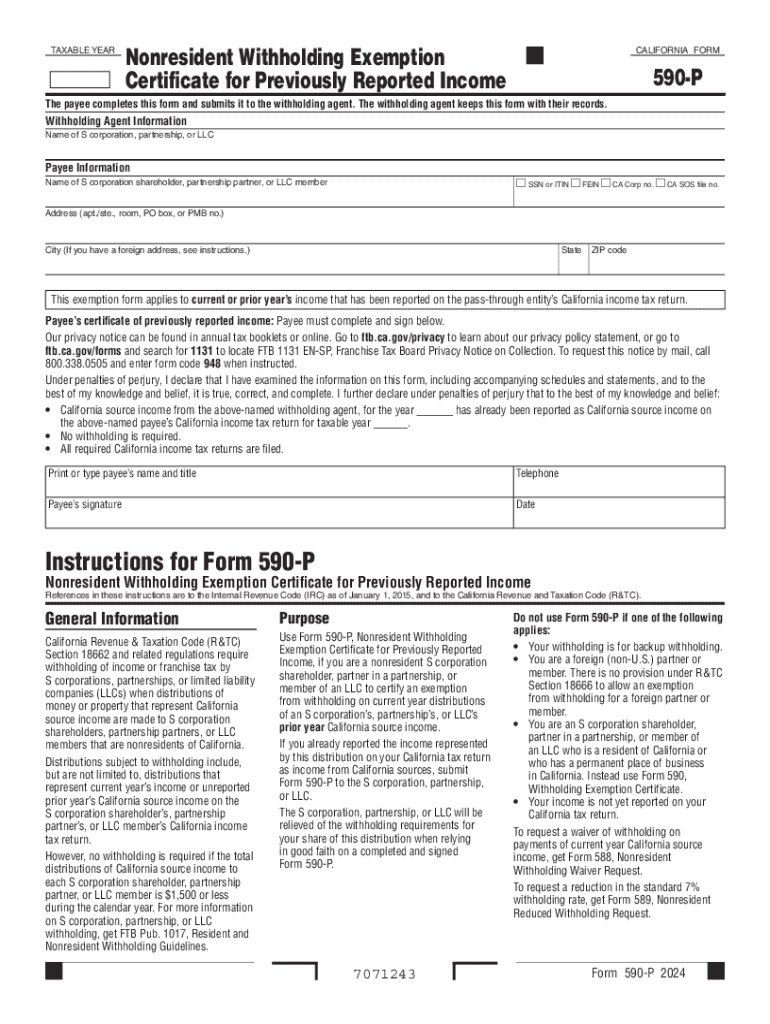

The 2025 Form 590-P, or Nonresident Withholding Exemption Certificate for Previously Reported Income, is a tax form utilized in California. It serves a specific purpose: to allow nonresident S corporation shareholders, partnership partners, or LLC members to certify an exemption from withholding on distributions of prior year California source income that has already been reported on their tax returns. This form is essential for managing tax obligations efficiently and avoiding redundant withholding on income that is not subject to further tax due to prior reporting.

How to Use the 2025 Form 590-P Nonresident Withholding Exemption Certificate for Previously Reported Income

To utilize the 2025 Form 590-P effectively, nonresident taxpayers must fill out the form with accurate information that reflects their share of previously reported income. Once completed, the form must be submitted to the withholding agent responsible for distributions. This agent retains the form for record-keeping purposes, confirming that withholding on the specified income is exempt. Key steps include accurately identifying the taxpayer's share of income, confirming previous reports, and ensuring that all necessary signatures are included.

Important Steps for Completion

- Obtain the Form: Secure a copy from the California Franchise Tax Board or an authorized source.

- Fill Out Personal Information: Enter your name, address, and taxpayer identification number accurately.

- Specify Prior Year Income: Detail your share of California source income that was reported in prior tax years.

- Submit to Withholding Agent: Provide the form to the agent who distributes your income share, ensuring you meet the exemption criteria.

Eligibility Criteria

Eligibility for using Form 590-P centers around nonresident individuals who receive California source income through certain business structures, such as S corporations, partnerships, or LLCs. To qualify for the withholding exemption, individuals must have previously reported the relevant income on applicable tax returns. This ensures that the withheld taxes on income distribution have already been settled. It's crucial to verify eligibility before submitting the form to avoid complications.

Who Typically Uses the 2025 Form 590-P

This form is generally used by nonresident individuals linked to California-sourced income from business entities like:

- S Corporations: Shareholders receiving income distributed as dividends from prior reported sources.

- Partnerships: Partners who have already reported partnership income from California.

- LLCs: Members benefiting from passed-through income allocations previously declared on tax returns.

Key Elements of the 2025 Form 590-P

Understanding the core elements of the form helps ensure correct and complete submission:

- Personal Identification: Name, identification number, and contact details of the nonresident taxpayer.

- Income Verification: Details on the prior year’s income, substantiating exemption claims.

- Withholding Agent Information: Identifying the agent who manages the withholding process.

- Signature and Date: Validates the information provided and confirms agreement to the exemption terms.

Legal Use of the Form

The form's legal use is strictly confined to the exemption from withholding tax on California sourced income reported in previous tax years. It is not a means to avoid tax payment but a tool for ensuring non-duplicative withholding on income distributions. Both taxpayers and agents must adhere to prescribed guidelines to ensure the form is used appropriately without legal repercussions.

State-Specific Rules for the 2025 Form 590-P

California has distinct rules governing the use of Form 590-P, and compliance with these regulations is vital for taxpayers seeking the withholding exemption. California franchise tax laws mandate that only income already reported in prior years is eligible for exemption, preventing tax evasion or avoidance. Nonresidents must understand and comply with these rules to utilize Form 590-P effectively.

Filing Deadlines / Important Dates

While no specific deadline for filing the form exists, it should coincide with the withholding agent's timeline for distributing the applicable income. Submission before or at the time of distribution is ideal to ensure exemption processing goes smoothly. The withholding agent must be in possession of the form before income distribution to activate the exemption.

Penalties for Non-Compliance

Failure to comply with the requirements of Form 590-P can result in penalties. If a nonresident erroneously or fraudulently claims an exemption, they might face financial penalties or legal action from California tax authorities. It's crucial to ensure that all information provided is accurate and truthful to avoid these punitive measures.

Form Submission Methods (Online / Mail / In-Person)

The Form 590-P can be submitted to the withholding agent via several methods. Electronic submission is often available, provided the agent's systems support it. Alternatively, forms can be mailed or directly handed to the agent. Each method requires confirming receipt and ensuring the agent acknowledges the form in their records for proper exemption processing.