Definition and Meaning

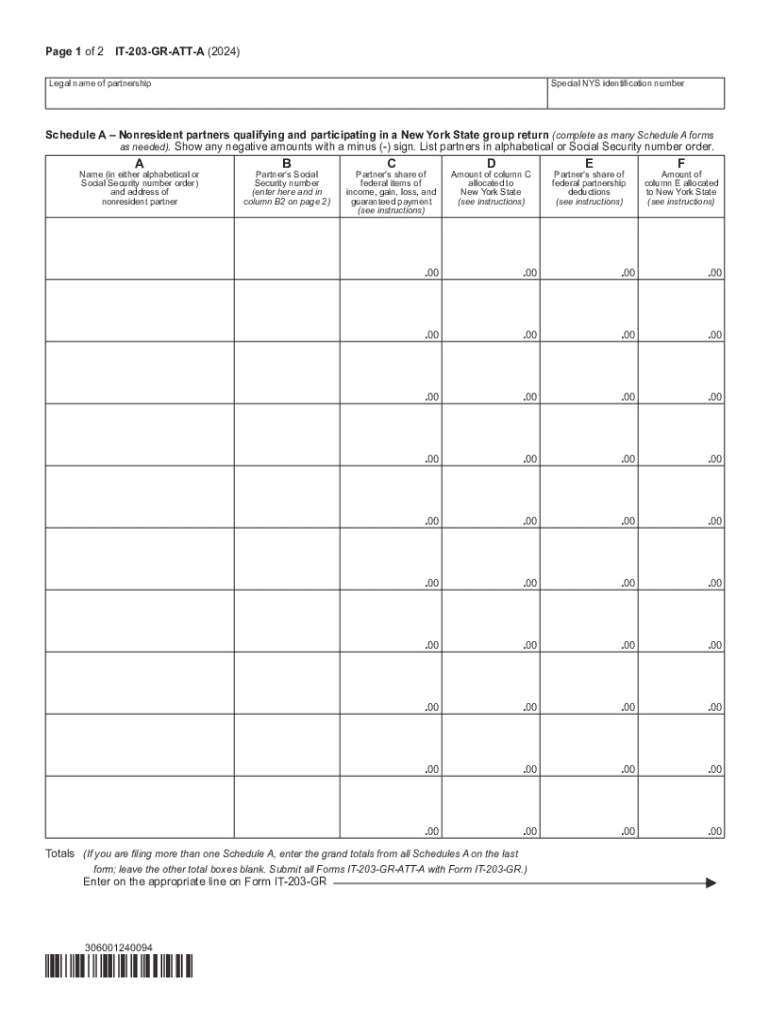

Form IT-203-GR-ATT-A Schedule A, also known as the New York State Group Return for Nonresident Partners for Tax Year 2024, is a tax form used to report the income and deductions of nonresident partners participating in a group filing. This form gathers essential information about each partner, including their federal income shares, allocations to New York State, and calculations for state tax liabilities and overpayments. By consolidating this information into one form, partnerships simplify compliance with state tax laws while accurately representing each partner's tax obligations.

How to Use the Form IT-203-GR-ATT-A Schedule A

To properly use Form IT-203-GR-ATT-A Schedule A, partnerships must first compile a comprehensive list of all nonresident partners eligible for group filing. Each partner’s federal income share must be calculated and recorded alongside New York State-specific allocations. Once all individual details are documented, partnerships must calculate any applicable state tax liabilities or overpayments. After ensuring all entries are accurate, the form is submitted as part of the overall tax filing package.

Detailed Steps for Completion

-

Gather Required Information:

- List all nonresident partners.

- Calculate federal income shares for each partner.

-

Determine State Allocations:

- Allocate each partner’s income to New York State using provided guidelines in the form instructions.

-

Calculate Liabilities:

- Use the form to compute New York State tax liabilities or overpayments based on each partner's allocated income.

-

Review and Finalize:

- Double-check all calculations and ensure all required fields are completed before submission.

Important Terms Related to Form IT-203-GR-ATT-A Schedule A

Understanding key terminology is crucial when filling out Form IT-203-GR-ATT-A Schedule A. Important terms include:

- Nonresident Partner: A partner who does not reside in New York State but participates in a partnership with New York State-based operations.

- Federal Income Share: The portion of income attributed to a partner according to federal guidelines which must be declared for state taxation.

- State Allocation: The process of determining how much of a partner’s federal income share is attributable to activities within New York State.

- Group Filing: A simplified tax filing method allowing partnerships to file a single return on behalf of multiple nonresident partners.

Key Elements of the Form

Several critical sections make up Form IT-203-GR-ATT-A Schedule A, each designed to collect specific information necessary for compliance:

- Partner Information Section: Includes names, addresses, and federal identification numbers.

- Income Allocation Section: Documents each partner’s federal income share and subsequent allocation to New York.

- Tax Computation Section: Calculates tax liabilities based on allocated income.

- Payment and Refund Summary: Provides a concise overview of any amounts due or refunds owed.

State-Specific Rules for Completion

New York State has specific guidelines that must be adhered to when completing the form:

- Allocation Rules: Income must be allocated according to New York State apportionment regulations, which may differ greatly from federal rules.

- Tax Rate Application: Use the state-mandated tax rates and brackets in determining partnership liabilities.

Required Documents

When completing Form IT-203-GR-ATT-A Schedule A, have the following documents handy:

- Federal K-1 Schedules: To accurately report individual income shares.

- Previous Year’s Tax Filings: Useful for confirming historical income trends and allocations.

Eligibility Criteria

Not all partnerships can file Form IT-203-GR-ATT-A Schedule A. Specific eligibility criteria include:

- Nonresident Partners: Only applies to partners living outside New York.

- Active Business in NY: The partnership must conduct a portion of its business operations in New York.

Filing Deadlines and Important Dates

Adherence to specific filing deadlines is essential to avoid penalties:

- Standard Filing Deadline: Typically aligns with federal tax deadlines but always confirm annually with the New York State Department of Taxation and Finance.

- Extensions: Available under certain conditions, although interest on unpaid taxes may accrue.

Penalties for Non-Compliance

Failure to accurately complete or timely file Form IT-203-GR-ATT-A Schedule A can result in:

- Financial Penalties: Fees imposed for late submission or inaccuracies.

- Interest on Unpaid Taxes: Accrued daily based on the total amount owed.

Understanding and meticulously following these guidelines ensures compliance and minimizes potential issues with New York State tax obligations.