Definition and Meaning

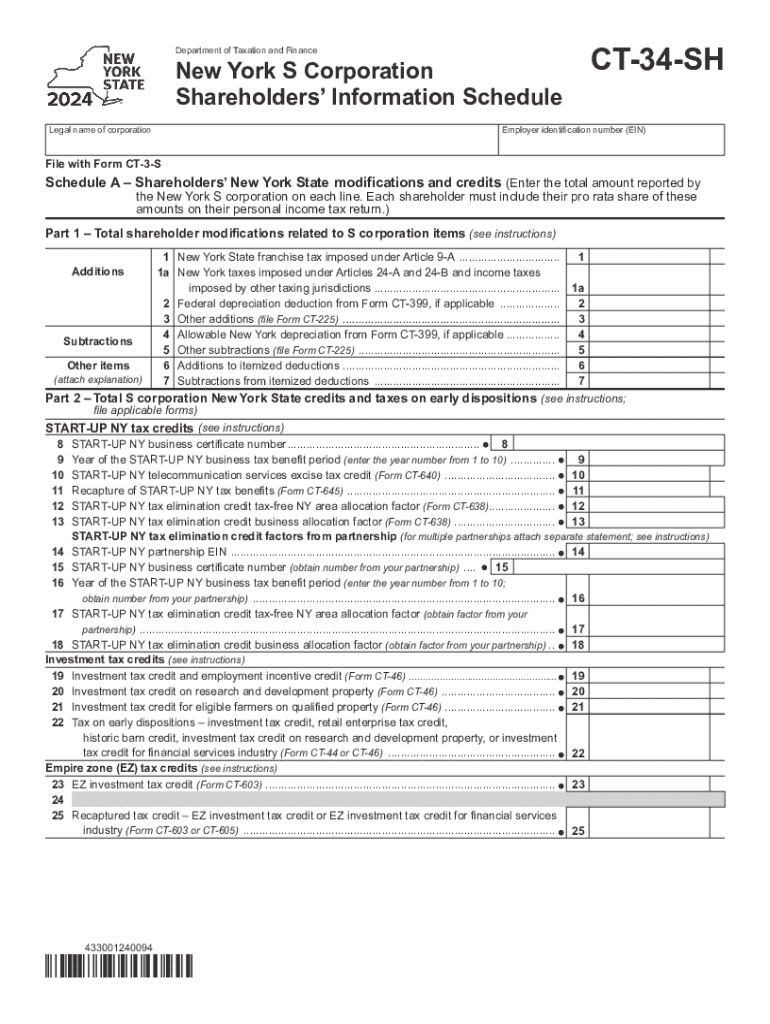

The New York S Corporation Shareholders' Information Schedule, commonly known as Form CT-34-SH, is a crucial tax document for S corporations operating within New York State. This form provides a structured breakdown of the items that shareholders must report on their personal income tax returns. It encompasses details regarding income, modifications, credits, and taxes connected to S corporation activities. The aim is to ensure that shareholders accurately reflect their share of the corporation's income or losses, in compliance with New York tax regulations.

How to Use the Instructions for Form CT-34-SH New York S Corporation

Understanding the instructions for Form CT-34-SH is essential for accurate tax filing. The instructions guide users through each section of the form, explaining how to report income and losses derived from the S corporation. The document clarifies the calculation of modifications and tax credits, ensuring that shareholders account for all necessary adjustments. Users must follow the form's sequential order, as the instructions are designed to systematically address different tax components related to S corporations.

Steps to Complete the Instructions for Form CT-34-SH New York S Corporation

-

Gather Necessary Documents: Before starting, collect all relevant financial statements and records of the S corporation’s income, deductions, and credits.

-

Review the Modification List: Identify any modifications to federal amounts as required by New York State tax laws.

-

Calculate Shareholder Income: Use the form to compute each shareholder’s share of the corporation's income or losses, integrating any required modifications.

-

Apply Tax Credits: Carefully apply any eligible tax credits, following the instructions to ensure proper allocation to each shareholder.

-

Complete Each Section: Methodically complete each section of Form CT-34-SH using the detailed instructions as a guide.

-

Verify Information: Double-check all entries for accuracy, ensuring compliance with both federal and state tax regulations.

Important Terms Related to Instructions for Form CT-34-SH

- S Corporation: A type of corporation that passes income directly to shareholders, avoiding double taxation on earnings.

- Modifications: Adjustments necessary to align federal tax amounts with New York State insurance requirements.

- Tax Credits: Deductions that reduce overall tax liability, specific to activity within the S corporation.

- Shareholder: An individual or entity owning shares in the corporation, thus required to report a proportionate share of income.

Key Elements of the Instructions for Form CT-34-SH

- Adjustments to Income: Guidelines for adjusting federal figures to meet state-specific tax rules, ensuring total income reported conforms to New York's standards.

- Credit Calculations: Detailed methods for computing tax credits, essential for reducing taxable income both at the state and personal level.

- Income Reporting: Clear instructions on translating corporate income into shareholder personal income, including provisions for both gains and losses.

Filing Deadlines and Important Dates

Understanding the timeline for submission is critical. Form CT-34-SH follows the tax year calendar, with filing typically due by March 15 of the year following the end of the tax year, unless an extension has been granted. Adhering to these deadlines ensures compliance and avoids penalties.

Penalties for Non-Compliance

Failure to accurately file Form CT-34-SH can lead to significant penalties. Common penalties include fines for late submissions or for omitting crucial information, which can impact the corporation and its shareholders. Accurate comprehension and timely completion of the form mitigate these risks.

Form Submission Methods (Online / Mail / In-Person)

Form CT-34-SH can be submitted electronically, by mail, or in-person. Electronic filing is encouraged for its speed and convenience, providing immediate confirmation of receipt. Mailed submissions must be postmarked by the deadline, and in-person submissions are accepted at designated New York State tax offices, each offering distinct procedural steps for processing.

State-Specific Rules

New York's tax rules for S corporations are distinct from federal regulations, emphasizing the importance of adhering to state-specific requirements. This includes variations in income modifications and how credits are applied. Understanding New York's tax landscape is crucial for fiduciary compliance, ensuring all reporting aligns with local statutes and remains accurate for fiscal review.

Examples of Using the Instructions for Form CT-34-SH

Consider a scenario where a shareholder needs to report income adjustments based on varying state laws. The instructions for Form CT-34-SH help delineate these requirements, furnishing real-life examples to illustrate correct application. This might include a walkthrough of claiming specific credits or the accurate depiction of pass-through income, offering clear procedural steps to emulate when engaging with real-world tax submissions.