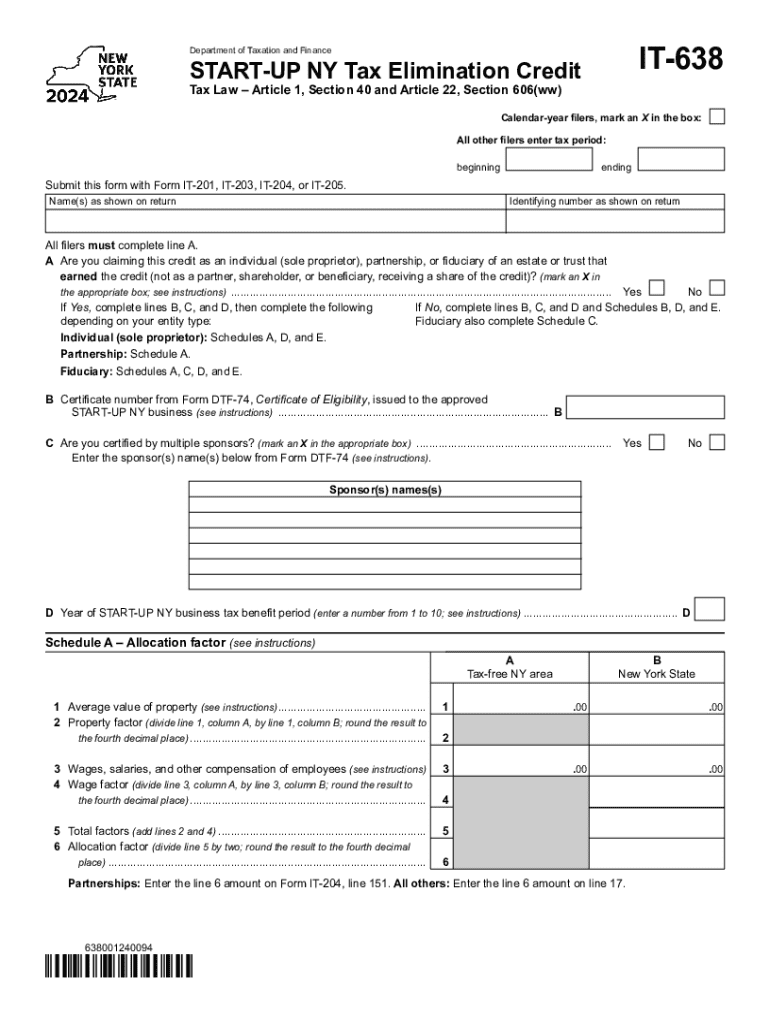

Definition & Meaning

The "part 106 credits against New York State personal income tax" are a specific type of taxation credit applicable within the state of New York. This credit allows individual taxpayers to reduce their overall state personal income tax liability by accounting for specific credits associated under part 106 of New York State tax law. These credits could arise from various eligible activities or expenditures recognized by the State as deserving of tax incentives. Understanding these credits can be vital for maximizing tax savings during the filing process.

Distinction from Other Credits

- Part 106 credits differ from federal tax credits, as they are applied only at the state level.

- These credits typically address state-specific incentives or policies which may not align with federal tax credits.

How to Use the Part 106 Credits Against New York State Personal Income Tax

Claiming part 106 credits involves several key steps, ensuring that the taxpayers meet all requirements and conditions set by New York State.

-

Determine Eligibility: Review the specific criteria for each credit under part 106 to confirm eligibility.

- Check if the activities or investments that qualify for the credit were completed within the tax year.

- Assess any residency requirements or other state-specific conditions.

-

Calculate the Credit Amount: Accurately calculate the potential credit amount based on the applicable criteria.

- Ensure all calculations are detailed and supported by relevant financial records or documentation.

-

Document Compliance: Maintain comprehensive documentation showing adherence to all qualifying activities.

- Gather invoices, receipts, and proof of payments related to eligible expenditures.

How to Obtain the Part 106 Credits

Obtaining these credits involves proactively engaging with the relevant processes to ensure compliance and entitlement.

- Familiarize with State Tax Law: Understand the specific statutes or administrative bulletins outlining part 106 credits.

- Consult a Tax Professional: Engaging with a professional who specializes in New York State tax law ensures proper handling of the credits.

- Stay Updated on Changes: Monitor any legislative changes affecting part 106 credits, as state policies may evolve annually.

Steps to Complete the Part 106 Credits Against New York State Personal Income Tax

To correctly claim the credit on your tax return, follow these structured steps:

-

Gather Necessary Documentation:

- Collect records of all expenses or investments related to the credit.

-

Accurate Tax Form Completion:

- Use the specific New York State tax forms to report part 106 credits.

- Double-check all entries for accuracy to avoid errors that may lead to non-compliance.

-

Review Filing Instructions:

- Adhere to the latest instructions from New York State for the current tax year.

-

Submit Completed Forms:

- Ensure all forms and supporting documents are submitted by the designated deadline to facilitate timely processing.

Important Terms Related to Part 106 Credits

Understanding specific terms can provide clarity and enhance the effective claiming of these credits:

- Tax Liability: The total amount of tax owed to the state government before applying credits or deductions.

- Qualifying Expenditure: Expenses that meet designated criteria under state tax law to be eligible for credits.

- Credits Carryforward: Some credits may be carried forward to future tax years if unused in the current year.

Key Elements of the Part 106 Credits

Identifying the primary components helps streamline the navigation and application of these credits:

- Eligible Activities: These might include investments in state-approved projects or contributions to certain state programs.

- Credit Limitations: Some credits may have caps on the amount that can be claimed.

- Timeframe for Application: Specific periods during which credits can be claimed, generally aligning with annual tax return timelines.

State-Specific Rules for the Part 106 Credits

Navigating New York's specific regulations plays a critical role in effectively claiming these credits:

- These rules may include residency requirements or stipulate that eligible activities occur within New York State.

- Rules can change annually, necessitating regular review and updates.

Examples of Using the Part 106 Credits

Understanding real-world examples illuminates practical applications and maximizes credit utilization:

- Case Study: A taxpayer invests in a New York-based renewable energy project, qualifying for a relevant credit.

- Scenario Analysis: Comparison of tax liability with and without the credits, illustrating potential savings.

Filing Deadlines and Important Dates

Adhering to deadlines is crucial for credit claims:

- Standard Filing Deadline: Aligns with the New York State tax filing date, typically in April.

- Extension Filings: Information on how credits interact with state-permitted filing extensions.