Definition and Meaning

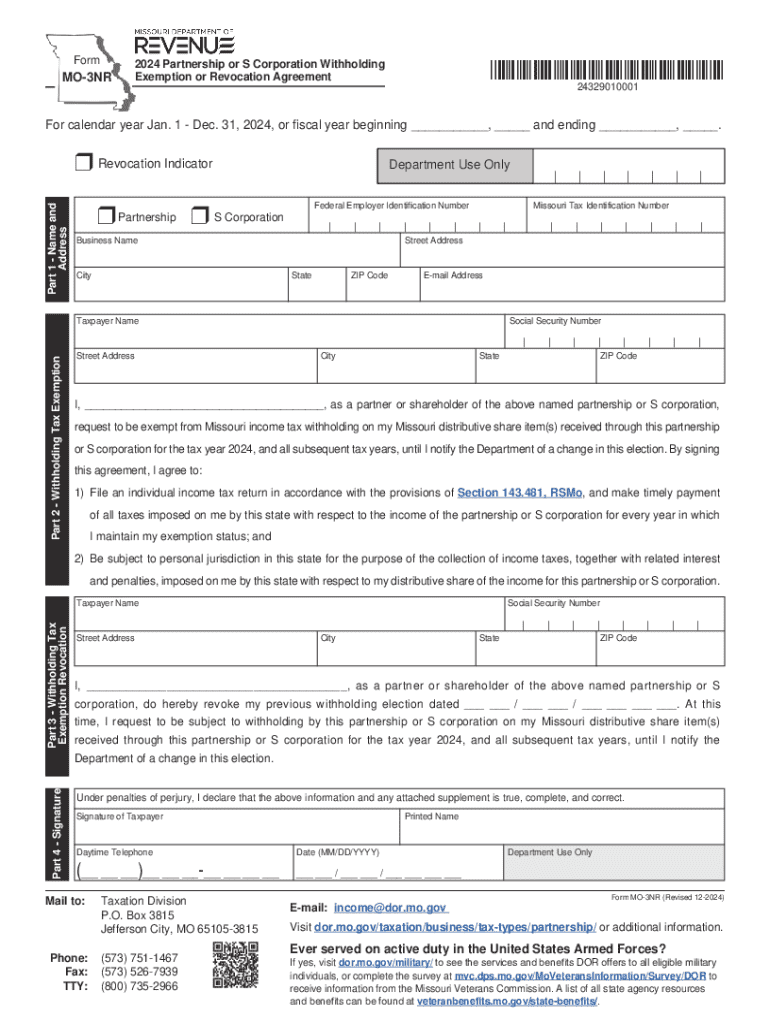

Form MO-3NR, officially titled the "2024 Partnership or S Corporation Withholding Exemption or Revocation Agreement," is a document used for tax purposes in Missouri. It allows nonresident partners or shareholders to either request an exemption from Missouri's income tax withholding on their share of the income or to revoke a previously granted exemption. This form is crucial for businesses structured as partnerships or S corporations with nonresident members, aiming to manage state tax obligations efficiently.

How to Use the Form MO-3NR

Using Form MO-3NR involves detailed steps to either apply for exemption or revoke an existing exemption for nonresident partners or shareholders. Key stages include:

- Identify the Need: Determine whether an exemption from Missouri withholding is beneficial or if an existing exemption no longer applies.

- Gather Required Information: Ensure you have the necessary personal and business details of the partner or shareholder.

- Complete the Form: Fill out the sections relevant to your needs—either the exemption request or revocation.

- Review and Submit: Double-check the completed form for accuracy before submitting it to the Missouri Department of Revenue.

Steps to Complete the Form MO-3NR

Completing the Form MO-3NR requires careful attention to detail:

- Understand the Sections: Familiarize yourself with the form's sections, which include personal details, business information, and a choice between exemption or revocation.

- Complete Personal Information: Fill in the nonresident partner or shareholder's name, address, and taxpayer identification number.

- Business Information: Include the partnership or S corporation's details, such as the name and tax ID.

- Choose Exemption or Revocation: Clearly indicate whether you are requesting an exemption from withholding or revoking an existing exemption.

- Signature and Date: The form must be signed by an authorized individual and dated.

Eligibility Criteria

Eligibility to use Form MO-3NR typically involves:

- Nonresident Status: The partner or shareholder must be a nonresident for Missouri tax purposes.

- Business Structure: The business must be a partnership or S corporation.

- Income Type: The income in question should be eligible for withholding exemption under Missouri law.

Key Elements of the Form MO-3NR

Several critical components make up the form:

- Personal and Business Identification: Accurate input of identifying information ensures proper processing.

- Exemption or Revocation Election: Clear selection between exemption requests or revocation.

- Attestation and Signature: A declaration by the signatory affirming the accuracy of provided information.

Important Terms Related to the Form

Certain terms are pivotal in understanding Form MO-3NR:

- Withholding: The portion of income automatically deducted for state taxes.

- Nonresident: Individuals whose primary domicile is outside Missouri.

- Distributive Share: The partner’s or shareholder’s share of income from the business entity.

State-Specific Rules

Missouri-specific regulations impact the use of this form:

- Tax Rate Considerations: Missouri has specific tax rates affecting the withholding calculations.

- Form-Related Deadlines: Submission deadlines may vary based on tax years and changes in state guidelines.

Filing Deadlines and Important Dates

Awareness of due dates is critical for compliance:

- Annual Filing Requirement: Typically, the form must align with the entity's tax year.

- Amendments and Corrections: Allowance for form updates if situations change mid-year.

Penalties for Non-Compliance

Failure to file or incorrect submissions can lead to:

- Fines or Interest Charges: Non-compliance can result in financial penalties.

- Administrative Delays: Unresolved issues may lead to processing delays and complications in business operations.

Form Submission Methods

Form MO-3NR offers several submission pathways:

- Online Filing: Electronic submission directly through state-tax websites.

- Mail-In Options: Traditional mailing of physical forms to designated state offices.

The comprehensive handling of these aspects ensures that partnerships and S corporations maintain compliance with Missouri tax regulations efficiently, safeguarding against potential legal or financial repercussions.