Definition & Meaning

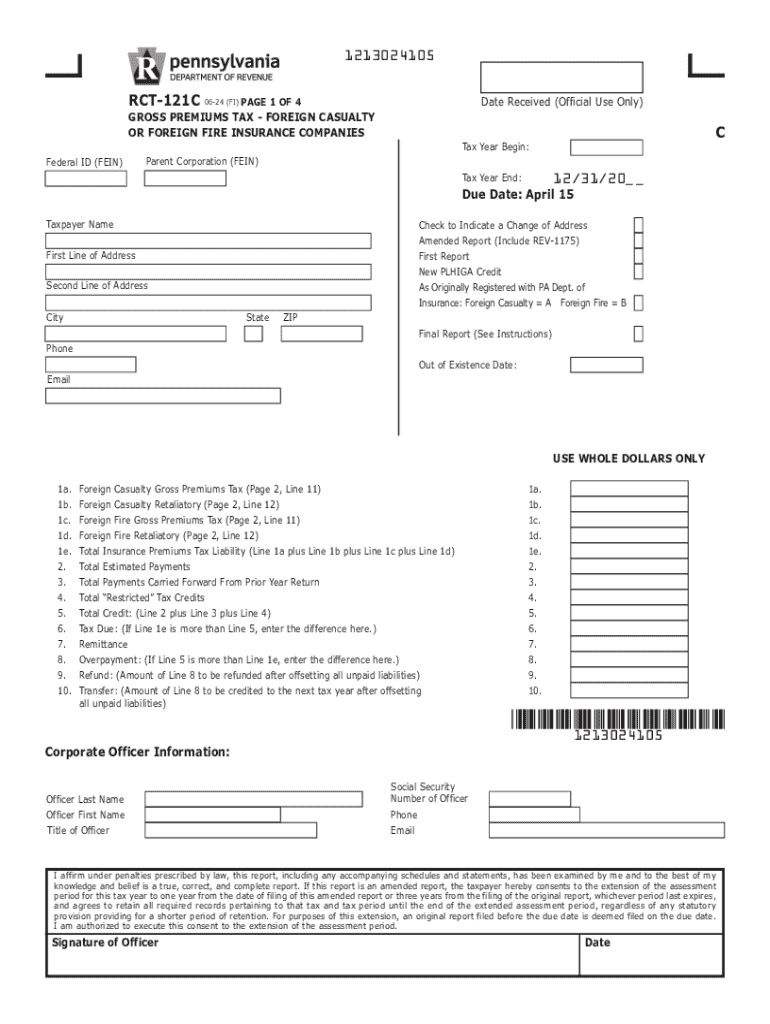

The Gross Premiums Tax - Foreign Casualty or Foreign Fire Insurance Companies (RCT-121C) is designed for foreign insurance entities operating within Pennsylvania. This form is integral for reporting and calculating taxes based on gross premiums collected from policyholders. It specifically applies to foreign casualty and fire insurance companies, ensuring they comply with state tax obligations. The RCT-121C form facilitates the state's ability to levy taxes proportionally to the premiums collected, thus funding public services and infrastructure through these collections.

Important Terms Related to RCT-121C

Understanding the terminology is crucial when dealing with the RCT-121C form. Key terms include:

- Gross Premiums: The total revenue collected from insurance policyholders before deductions for reinsurance or ceding commissions.

- Foreign Insurance Company: An insurance entity domiciled outside of Pennsylvania but authorized to conduct business within the state.

- Tax Liabilities: The obligations that arise from the collection of premium revenues, which are subject to state tax regulations.

- PLHIGA Credit: The Pennsylvania Life and Health Insurance Guaranty Association credit, available for certain policyholders and insurance entities, allowing for possible tax deductions under specific circumstances.

Eligibility Criteria

Entities that need to utilize the RCT-121C form must meet specific eligibility criteria:

- Must be an insurance company operating under the casualty or fire insurance domains.

- The entity must be foreign, meaning it is established outside Pennsylvania but authorized to conduct business within the state.

- Should have gross premiums collectable within the fiscal year from Pennsylvania residents or businesses.

Entities meeting these conditions must annually file the RCT-121C form to remain compliant and avoid penalties.

Steps to Complete the RCT-121C Form

Filing the RCT-121C form involves several meticulous steps to ensure accuracy and compliance with state regulations:

- Gather Relevant Information: Collect details on all gross premiums received during the fiscal year, making note of any reinsurance agreements that might affect gross totals.

- Complete the Form: Fill in the RCT-121C form with the appropriate financial details along with other mandatory sections, such as entity identification information.

- Calculate Tax Liabilities: Using the provided schedules and instructions, calculate the applicable taxes due based on the gross premium totals.

- Review and Attach Supporting Documents: Include all necessary documentation, such as financial statements and evidence of presumed tax credits like the PLHIGA credit.

- Submit the Filled Form: Depending on preference, submit the form electronically or through mail, ensuring it is filed by the state’s tax deadlines.

Filing Deadlines / Important Dates

Timely filing is critical for the RCT-121C form:

- The form must be filed annually, generally aligning with the fiscal year's end.

- Filing and payment deadlines typically coincide with the beginning of the new fiscal year, though specific dates should be confirmed yearly.

- Late filing can lead to penalties; therefore, it is recommended to begin preparation well in advance of the deadline.

Required Documents

To ensure compliance, several documents should accompany the RCT-121C form:

- Financial statements detailing gross premiums and any deductions or credits claimed.

- Documentation supporting any tax credits or deductions, such as the PLHIGA credit.

- Any relevant reinsurance contracts impacting the gross premium totals.

Including these documents helps in verifying the accuracy of the reported information and reducing the risk of audit or penalties.

State-Specific Rules for RCT-121C

While RCT-121C generally applies uniformly across Pennsylvania, there are state-specific guidelines:

- The definition of "foreign insurance company" is strictly adhered to, impacting eligibility.

- Tax rates and credit availability, such as the PLHIGA credit, must comply with Pennsylvania regulations, impacting calculations.

- Any state-imposed surcharges or additional tax requirements should be incorporated into the final reported amounts.

Penalties for Non-Compliance

Non-compliance with RCT-121C filing requirements can lead to various penalties:

- Monetary fines for late submissions or inaccuracies in reported premiums.

- Possible interest charges accruing on unpaid taxes following deadlines.

- Additional fees resulting from failure to provide necessary documentation or corrected filings following discrepancies.

Entities should ensure thorough and timely filings to avoid these penalties.

Who Issues the Form

The RCT-121C form is issued by the Pennsylvania Department of Revenue. This administrative body regulates the collection of taxes from foreign insurance companies and oversees compliance with state tax laws. They provide updates, changes in tax codes, and any modifications to form requirements.

Digital vs. Paper Version

Entities have the choice between digital and paper submissions for the RCT-121C form:

- Digital Filing: Offers speed and immediate confirmation of receipt, reducing mailing delays and processing time. Electronic filing may provide tools that automatically calculate liabilities, increasing accuracy and efficiency.

- Paper Submission: Traditional and allows for manual filing, which some companies may prefer due to familiarity. However, this process is slower and can lead to potential delays in processing.

Opting for digital filing is generally recommended for promptness and reduced risk of error.