Definition & Meaning

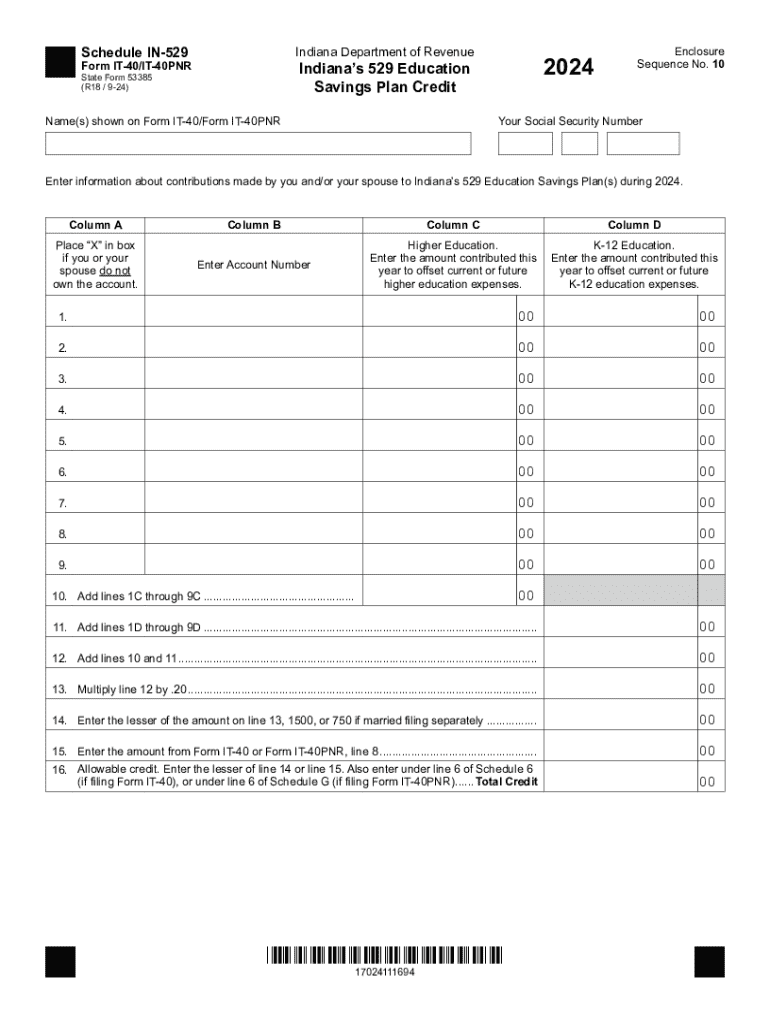

Schedule IN-529 is a tax form used by residents of Indiana to claim a tax credit for contributions made to the state's 529 Education Savings Plan. The 529 Plans were established to help families save for future educational expenses in a tax-advantaged manner. By contributing to an Indiana 529 Plan, donors may be eligible for a state income tax credit, thereby incentivizing investment in educational savings. The form is essential for accurately reporting these contributions and claiming the associated tax benefits.

How to Use the Schedule IN-529

Using Schedule IN-529 involves documenting your contributions to Indiana's 529 Education Savings Plan during the tax year. Taxpayers should use the form to calculate the allowable tax credit, which is typically a percentage of the total contributions up to a specified limit. This credit directly reduces the state income tax liability, potentially resulting in tax savings. Familiarizing yourself with the instructions and detailed completion steps on the form will ensure accurate reporting and maximize your tax benefits.

Important Steps in Form Completion

- Record Contributions: Keep detailed records of each contribution made to your 529 Plan throughout the year.

- Calculate Credit: Use the form guidelines to compute the allowable credit based on your contribution amounts.

- Verify Eligibility: Ensure all contributions meet the program's requirements to qualify for the credit.

- Review Form Instructions: Carefully follow each step on the Schedule IN-529 to ensure all information is accurate.

Steps to Complete the Schedule IN-529

Completing Schedule IN-529 requires some careful data entry and calculation. Start by reviewing your contribution records and confirming the correct amounts. Calculate the tax credit you anticipate claiming by multiplying your eligible contributions by the prescribed rate. You are advised to consult the form's instructions for specific guidance on each section. After filling out the form, ensure all data inputs are accurate before attaching it to your state tax return.

Detailed Steps to Fill Out the Form

- Gather Documentation: Collect statements and receipts for all contributions made to the Indiana 529 Plan.

- Complete Identification Information: Enter your personal details as required by the form.

- Enter Contribution Details: Insert the total contribution amount in the specified fields.

- Compute the Credit: Utilize the provided calculation guide to determine your total tax credit.

- Attach and Submit: Attach the completed Schedule IN-529 to your Indiana state tax return for submission.

Eligibility Criteria

To qualify for the tax credits offered via Schedule IN-529, certain conditions must be met. You must be a resident of Indiana and have made contributions to the state's 529 Plan. Contributions must remain within the maximum allowable limits to be eligible for tax credits. Additionally, the contributed funds must be used for qualifying educational expenses, which typically include college tuition, certain K-12 expenses, books, and necessary supplies.

Factors Affecting Eligibility

- Residency Requirements: Only Indiana residents qualify for this specific tax credit.

- Qualified Expenses: Funds must be intended for use on qualifying educational costs.

- Contribution Limits: Compliance with state-imposed maximum contribution thresholds is essential.

Key Elements of the Schedule IN-529

The Schedule IN-529 form includes several key elements that must be accurately completed for a successful tax credit claim. These elements include personal identification data, specifics on the 529 Plan contributions, instructions on tax credit calculations, and a signature section. Ensuring the accurate completion of these elements is vital to claiming the tax benefits associated with your 529 Plan contributions.

Components of the Form

- Personal Information: Your full name, Social Security number, and other identifying details.

- Contribution Details: Sum total of annual contributions to the Indiana 529 Plan.

- Credit Calculation Section: Space for determining your eligible tax credit.

- Signature and Date: A mandatory section to validate the form.

State-Specific Rules for the Schedule IN-529

The Schedule IN-529 form adheres to state-specific regulations unique to Indiana taxpayers. These rules include a cap on the maximum credit that can be claimed and detailed definitions of what constitutes qualified educational expenses. Indiana residents need to familiarize themselves with these rules to make informed decisions about their educational savings plans and associated tax benefits.

Noteworthy Regulations

- Credit Cap: A maximum credit amount is specified by the state of Indiana.

- Qualified Expenses: Only expenses recognized by Indiana law are applicable for usage under the 529 Plan.

Required Documents

To accurately fill out Schedule IN-529, taxpayers should prepare and organize necessary documentation beforehand. Required documents typically include contribution statements from your 529 Plan provider, Indiana state tax forms, and previous tax returns for reference. Having these documents readily accessible will help cross-check information, enhancing accuracy and reducing errors.

Document Checklist

- 529 Plan Statements: Regular statements from your plan provider.

- Tax Forms: Indiana state tax forms for the current tax period.

- Prior Year Returns: If needed, to reference past contribution and credit details.

Legal Use of the Schedule IN-529

Schedule IN-529 serves as a legally recognized document for claiming state tax credits related to education savings contributions in Indiana. It’s essential for residents who seek to offset their tax liabilities through such contributions. The form ensures that participants accurately report their financial activity and claim the legal benefits provided by state law.

Compliance and Legal Implications

- Legal Recognition: The form is officially recognized for tax credit claims.

- Compliance: Adhering to the guidelines ensures legal and financial compliance.

- Accuracy Obligations: Correctly completing the form is necessary to avoid penalties.