Definition & Purpose of the Annual Information Return

An Annual Information Return is a mandated tax form required by the State of Oklahoma to report payments made during the calendar year by various payors such as corporations, partnerships, and individual taxpayers. This document primarily serves to ensure accurate income tax reporting and compliance. It delineates the types of payments that must be reported and outlines the specific guidelines for both residents and nonresidents. Understanding the purpose of this form is essential to ensure its correct completion and submission.

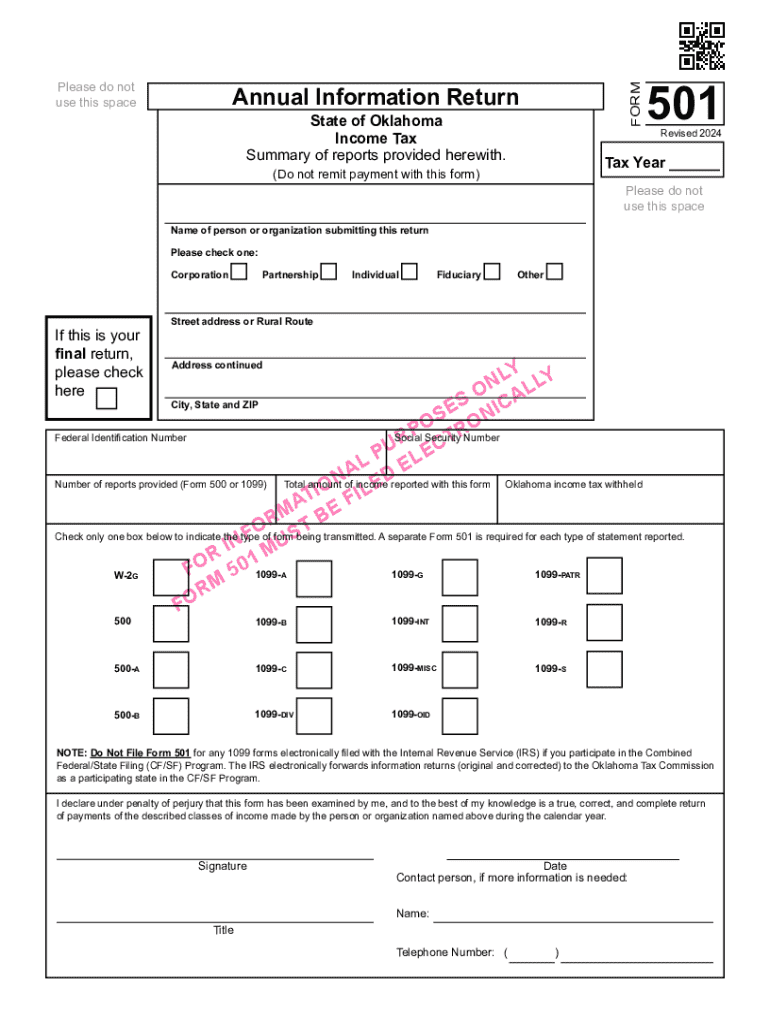

Reporting Requirements

- Payors: Includes corporations, partnerships, and individuals.

- Types of Payments: Covers employee compensations, interest, dividends, rents, and other payments.

- No Payment Submission: The form is strictly for reporting purposes and no remittances should accompany it.

- Penalties: There are potential penalties for non-compliance or incorrect submissions.

Steps to Complete the Annual Information Return

Completing an Annual Information Return requires careful attention to detail to ensure compliance with state law. The following steps provide a structured guide:

- Gather Necessary Documents: Collect all relevant financial records, including payment details and recipient information.

- Identify Reportable Payments: Determine which payments meet the criteria for reporting.

- Complete the Form Sections: Ensure all sections of the form are accurately filled out, including taxpayer identification and payment types.

- Review Instructions: Carefully review the form's instructions to avoid common errors and omissions.

- Verify Information: Double-check all entered data for accuracy and completeness.

- Submit Before Deadline: Ensure the form is submitted by the specified due date to avoid penalties.

Important Considerations

- Verify the inclusion of all necessary payor information.

- Thoroughly check guidelines for any state-specific variations.

Important Terms Related to the Annual Information Return

Understanding the terminology involved with the Annual Information Return is crucial for correctly completing the document. Here are some key terms:

Key Definitions

- Payor: The entity responsible for making reportable payments.

- Recipient: The individual or entity receiving payments from the payor.

- Nonresident Reporting: Special considerations for payors making payments to nonresidents.

State-Specific Rules for Completing the Form

The Annual Information Return for Oklahoma has specific rules unique to the state, such as:

- Resident vs. Nonresident Status: Different handling for payments based on residency.

- Deadline for Submission: All forms must be submitted by the due date specific to Oklahoma policymakers.

- Form Availability: Can be generally obtained from the Oklahoma Tax Commission.

Common Errors

- Misclassifying the residency status of the recipient.

- Failing to adhere to state-specific payment thresholds.

Legal Implications and Compliance

Non-compliance with the requirements of the Annual Information Return can lead to legal repercussions, including fines and penalties imposed by the state.

Legal Requirements

- Timely Submission: Meeting deadlines is crucial.

- Correct Data Entry: Accurate information is mandatory to prevent penalties.

- Retain Copies: Keeping copies for record purposes is advisable in case of audits or reviews.

Filing Deadlines and Important Dates

The Annual Information Return includes strict deadlines that must be adhered to:

- Calendar Year Reporting: Covers payments made within the calendar year.

- Submission Date: Typically due early in the following year, often by January 31 or similar deadlines established by the state.

Consequences of Missing Deadlines

- Incur penalties or interest on late submissions.

- Potential for legal action by the state for continued non-compliance.

Required Documents and Information

Proper documentation is critical for completing the Annual Information Return accurately:

- Payment Records: Detailed accounts of all reportable financial transactions.

- Recipient Contact Information: Including names, addresses, and taxpayer identification numbers.

- Identification Numbers: Both for the payor and recipient where applicable.

Document Checklist

- Financial statements

- Past returns for reference

- Communication records with recipients

Penalties for Non-Compliance

Failing to comply with the requirements of the Annual Information Return can lead to substantial penalties:

- Fines for Late Submission: Financial penalties that increase with the duration of delay.

- Incorrect Information: Penalties for submitting incorrect data or information.

- Failure to Report: Serious penalties for not filing when required.

Avoiding Penalties

- Submit early to allow for processing delays.

- Seek professional advice when necessary for complex financial situations.

Who Typically Uses the Annual Information Return

This form is primarily used by those responsible for disbursing payments that fall under the tax report requirements:

Typical Users

- Corporations: Required for dividends, interests, and other corporate payments.

- Partnerships: Reporting distributions and other payments relevant to partners.

- Individual Payors: Especially those managing large-scale payouts affecting taxation.

Understanding these users is not only important for recognizing who is responsible but also for contextualizing the types of payments that are significant in this form.