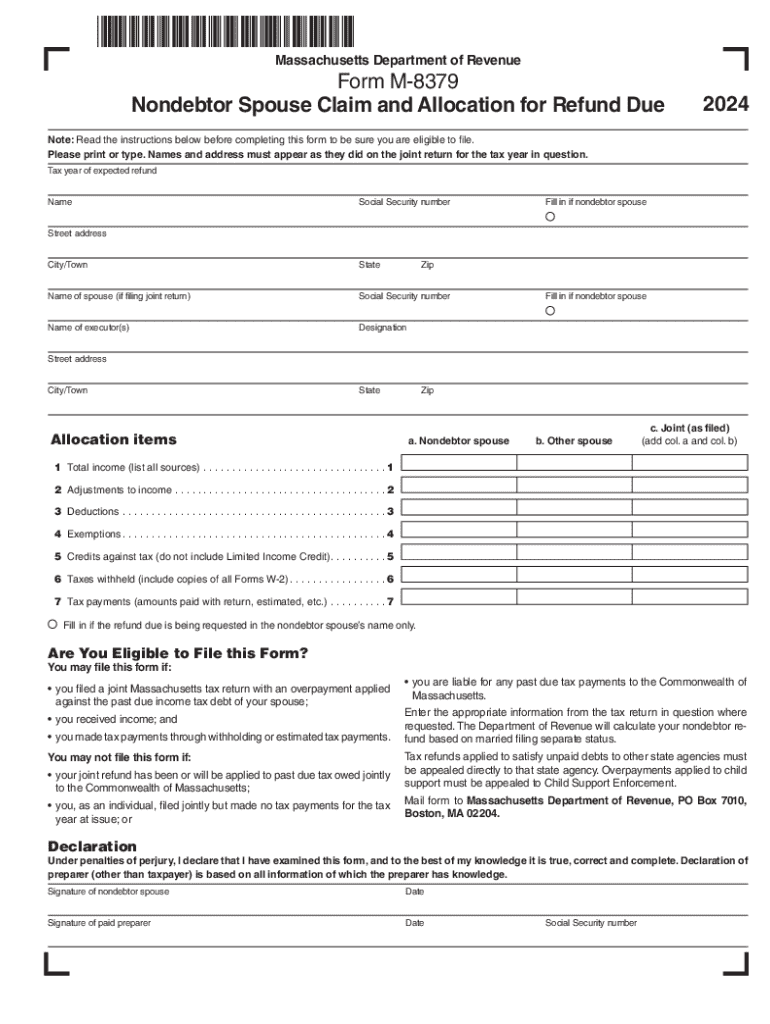

Definition and Purpose of M-8379

The M-8379 form is issued by the Massachusetts Department of Revenue for nondebtor spouses seeking to claim and allocate tax refunds from a joint tax return. This form directs the allocation of a joint tax refund when a portion or the entirety is applied to a spouse's past due tax debt. Its primary purpose is to ensure the nondebtor spouse receives their fair share of the tax refund.

Eligibility Criteria for M-8379

For a taxpayer to file the M-8379, specific eligibility criteria must be met. The key requirement is that the refund has been used to offset a spouse's tax liabilities. The nondebtor spouse must have filed jointly and be able to prove their share of the overpayment or tax refund was wrongly allocated. It’s pertinent to be aware of these criteria to prevent unnecessary filing.

Important Terms Associated with M-8379

- Nondebtor spouse: The spouse not originally owing the tax debt.

- Joint tax return: A tax return filed together by married couples.

- Refund allocation: The method of splitting the tax refund between spouses.

- Overpayment: Payment exceeding the tax liability resulting in a refund.

Steps to Complete M-8379

-

Gather Necessary Information: Collect personal data, including Social Security numbers and details of the joint tax return.

-

Fill Personal Details Section: Enter information such as names, addresses, and tax year in the designated field on the form.

-

Income and Withholdings Sections: Provide a breakdown of each spouse’s income and withholdings from the tax year in question.

-

Calculate Refund Allocation: Calculate and document the nondebtor spouse's rightful portion of the refund.

-

Signing the Declaration: Both spouses must sign the declaration at the end of the form, validating the provided information.

Common Mistakes During Completion

- Failing to provide supporting documentation.

- Incorrectly calculating the refund allocation.

- Omitting mandatory information in the personal details section.

How to Obtain M-8379

The M-8379 form is available through multiple channels to ensure accessibility for all eligible taxpayers:

- Online: Download directly from the Massachusetts Department of Revenue website in PDF format.

- Local Tax Office: Visit a local office for a physical copy and possible assistance in completion.

- Request by Mail: Contact the Massachusetts Department of Revenue for a paper version via postal services.

Filing Deadlines and Important Dates

Timeliness is critical when filing the M-8379. The deadline generally aligns with the tax filing period, typically April 15, unless extensions are announced. Be aware of state-specific deadlines which may differ from federal timelines.

Filing Methods for M-8379

- Online Submission: The fastest method, utilizing the Massachusetts Department of Revenue e-filing system.

- By Mail: Send to the designated PO Box as indicated on the form. Ensure timely postage to avoid late filing penalties.

- In-Person Filing: Some taxpayers may prefer handing in the form at a local Department of Revenue office for verification.

Legal Use and Compliance

The M-8379 form is legally binding once signed and submitted. It is recognized under state law for determining refund allocation. Non-compliance or misrepresentation on the form may result in penalties, such as fines or additional tax liabilities.

Penalties for Non-Compliance

- Misstating facts or failing to file could lead to audits and financial penalties.

- Intentionally providing false information might incur legal prosecution.

Examples and Scenarios of Using M-8379

Consider a scenario where a couple has filed jointly, and one spouse has past-due state tax liabilities. The M-8379 allows the nondebtor spouse to request that their part of the refund is not used towards the debtor's liabilities. For instance, if they contributed significantly to the taxes paid but did not incur the debt.

Practical Case Studies

- Case Study 1: Jointly filed, the husband's tax refund was used for the wife's prior debt. She files M-8379 to reallocate her entitled refund portion.

- Case Study 2: The wife's wages fully funded overpayments, but the husband's overdue taxes seized the complete refund. Filing M-8379 restores the wife's rightful refund share.

Edge Cases and Variations

Occasionally, non-standard situations arise, such as partial offsets or changes in tax statuses between filing and allocation, requiring careful consideration of financial records and tax advice.

Understanding how to effectively utilize the M-8379 form not only ensures compliance but also secures the rightful financial standing of a nonliable spouse.