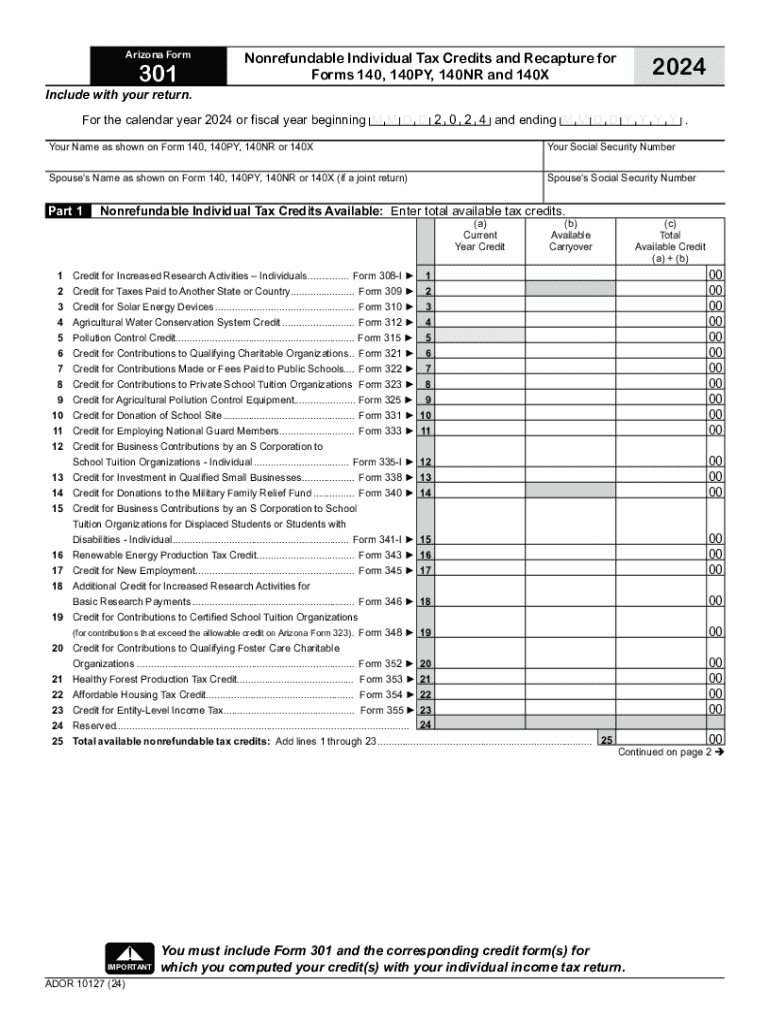

Definition and Meaning of Nonrefundable Individual Tax Credits in Arizona

Nonrefundable individual tax credits refer to the specific types of tax credits in Arizona that reduce the amount of tax owed, but cannot result in a refund if the credits exceed the tax liability. These credits are applicable for numerous activities, such as contributions to charitable organizations or educational expenses. The key aspect of these credits is that they are used to reduce your tax liability, but they do not result in a tax refund if they surpass the owed amount. Understanding these credits, as laid out in Arizona Form 301, can help ensure accurate reporting and compliance for individual taxpayers.

Examples of Nonrefundable Individual Tax Credits

- School Tax Credits: Taxpayers can claim credits for contributions to public and private schools.

- Charitable Organization Tax Credits: Credits for donations to Qualified Charitable Organizations (QCO) or Qualified Foster Care Charitable Organizations (QFCO).

- Renewable Energy Tax Credits: Credits available for investments in renewable energy projects for personal use.

How to Use the Nonrefundable Individual Tax Credits and Recapture Arizona

When utilizing the nonrefundable individual tax credits in Arizona, taxpayers must first identify eligible credits they can claim, gather relevant documentation to substantiate their claim, and accurately report these on the Arizona Form 301. This process involves several key steps:

- Identify Eligible Credits: Determine which specific nonrefundable tax credits are applicable to your financial activities.

- Document Contributions or Expenses: Retain records and receipts that verify your contributions, donations, or qualifying expenditures.

- Complete Arizona Form 301: Enter the required information based on the guidelines provided in the form and calculate your total tax credits.

Critical Considerations

- Always review the specific eligibility criteria for each credit.

- Confirm that your contributions fall within the allowable time period for the tax year.

Steps to Complete the Nonrefundable Individual Tax Credits and Recapture Arizona

Completing the Arizona Form 301 accurately is crucial for benefiting from nonrefundable tax credits. Follow these steps to ensure compliance:

- Gather Necessary Documents: Collect receipts, proof of donations, and any relevant certification documents.

- Access Arizona Form 301: Obtain the latest version of the form from the Arizona Department of Revenue’s website or your tax preparation software.

- Report Each Credit: Enter each qualified credit, along with any recapture amounts if applicable, in the relevant sections of Form 301.

- Calculate Subtotals: Follow instructions to properly calculate any limits or carryforward amounts.

- Submit Form with Your Tax Return: Attach the completed Form 301 to your Arizona state tax return for the respective tax year.

Eligibility Criteria for Nonrefundable Individual Tax Credits in Arizona

Eligibility for nonrefundable individual tax credits in Arizona relies on meeting specific conditions tied to each type of credit. General criteria include:

- Residency: Must be an Arizona resident or part-year resident during the tax year.

- Contribution Verification: Possess valid documentation from recognized institutions or donations.

- Expense Compliance: Ensure all expenses meet the requirements regarding sanctioned purposes or organizations.

Important Terms Related to Nonrefundable Individual Tax Credits and Recapture Arizona

Understanding the terminology associated with Arizona's tax credits can aid in accurately reporting and claiming them:

- Recapture: The process where previously claimed credits must be repaid under certain conditions, such as the non-completion of the required amount of time for a particular project or investment.

- Carryforward: Credit amounts that exceed the current year's tax liability that can be utilized in subsequent years.

- Qualifying Organization: An organization meeting state requirements to receive contributions qualifying for tax credits.

State-Specific Rules for Arizona Tax Credits

Arizona has distinctive regulations governing the use of nonrefundable tax credits:

- Credit Limits: Each type of tax credit has a defined maximum that taxpayers can claim within a tax year.

- Recapture Provisions: Specific situations may necessitate the repayment of credits claimed, often involving moving investments or assets out of state.

IRS Guidelines and Compliance

While nonrefundable individual tax credits are state-specific, they must still align with federal income taxation when reported in conjunction with federal returns:

- Ensure State Credits: Verify that state credits claimed do not conflict with federal tax obligations or the credits' federal deductibility.

- Align Tax Documents: Synchronize state and federal tax documentation to support reported credits.

Penalties for Non-Compliance

Failing to properly file or incorrectly claiming nonrefundable tax credits in Arizona can result in penalties, such as:

- Late Payment Penalties: Applicable if credits claimed do not accurately offset tax liabilities, resulting in undue outstanding taxes.

- Audit Penalties: Misreporting credits may lead to a state audit, which could unveil inconsistencies and invite penalties or mandatory recapture payments.