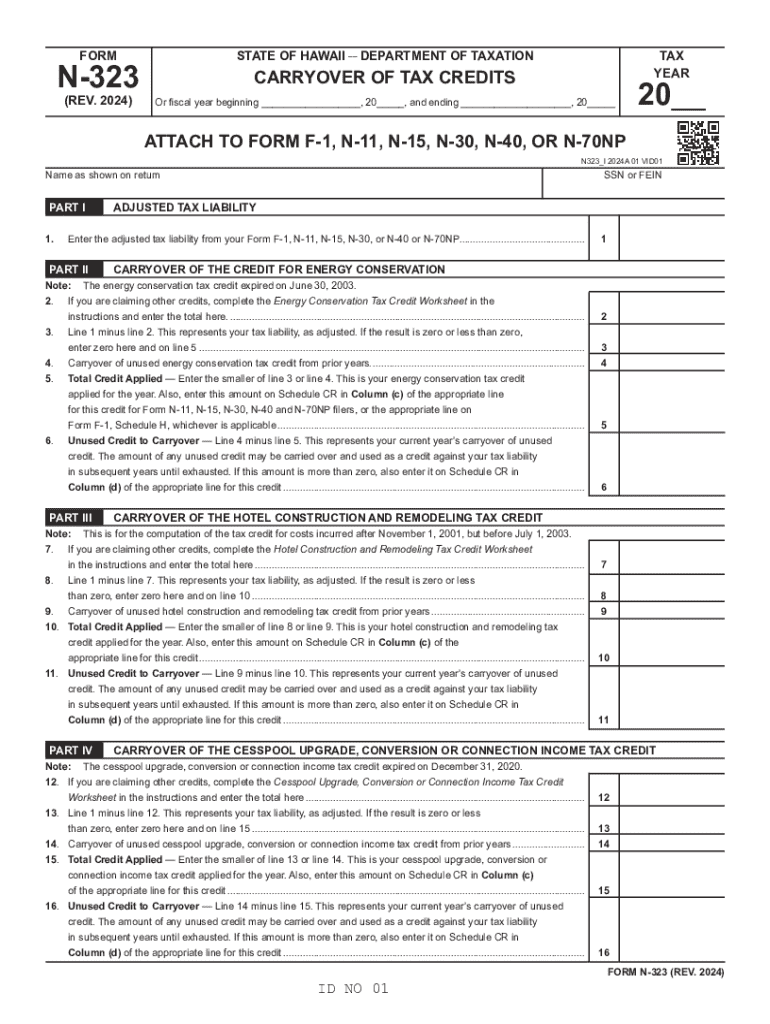

Definition and Purpose of Form N-323

Form N-323, Rev 2024, "Carryover of Tax Credits," is a document issued by the State of Hawaii Department of Taxation. It serves the function of reporting unused tax credits from prior years and applying them to current tax liabilities. The form is specifically tailored for various tax credits, including but not limited to energy conservation, hotel construction and remodeling, cesspool upgrades, renewable energy technologies, and more. The primary purpose is to ensure taxpayers can accurately calculate and claim eligible credits they can carry over, thereby optimizing their tax obligations.

The form facilitates the continuation of certain benefits linked to state-sanctioned initiatives, supporting taxpayers in sectors like renewable energy and organic foods production by allowing them to apply unutilized credits towards future tax periods. This document is essential for any taxpayer in Hawaii aiming to leverage these deferred credits efficiently.

Steps to Complete Form N-323

-

Review Eligibility: Determine which tax credits are eligible for carryover. This includes reviewing credits for energy conservation, residential construction, and technology infrastructure renovation.

-

Gather Required Information: Collect necessary documentation such as prior year tax returns showing unused credits, receipts for eligible expenses, and any official correspondence from the State of Hawaii Department of Taxation.

-

Calculate Adjusted Tax Liability: Use the specific calculations outlined in the form to determine the adjusted tax liability. This involves accounting for all active and deferred tax credits.

-

Complete Form Fields: Fill in the requested information, including personal details, tax identification numbers, and specific sections dedicated to each credit type.

-

Attach Supporting Documents: Enclose any required documentation that supports your eligibility for the credits claimed on the form.

-

Review and Submit: Before submitting, double-check all entered information for accuracy. Submit the form through the designated method, which may include mailing or electronic submission as specified by the State of Hawaii.

Key Elements of Form N-323

-

Personal Information: This section includes taxpayer name, address, and tax ID, ensuring the form is attributed to the correct individual or entity.

-

Carryover Details: Specific sections where taxpayers detail each type of credit carried over, including amounts and years of origin.

-

Credit Calculation: Instructions and fields for recalculating your adjusted tax liability and applying carryover credits.

-

Verification and Signature: A crucial part requiring review and signature to affirm the accuracy and completeness of the provided information.

Understanding these elements is crucial for proper form completion.

Eligibility Criteria for Tax Credit Carryover

To qualify for carrying over tax credits via Form N-323, taxpayers must meet specific criteria set out by the Department of Taxation. These include:

- Ensuring the credits applied are from qualifying categories such as renewable energy technologies or organic food production.

- Verifying the credits were unusable in the year they were originally claimed due to limits in tax liability.

- Complying with any project-specific requirements, such as maintaining renewable energy equipment or participating in designated conservation efforts.

Taxpayers must review the conditions carefully each year as legislation and criteria can change.

Examples of Using Form N-323

A practical example involves a taxpayer who invested in renewable energy technologies and earned sizable tax credits. Suppose the taxpayer's tax liability was insufficient to utilize the full credit in the year earned. In that case, Form N-323 allows the rolling forward of unused portions into subsequent years, thus providing ongoing financial relief and incentivizing continued investment in renewable technologies.

Another example is a hotel owner undertaking major renovations to improve energy efficiency. While substantial upfront costs can create initial tax burdens, the ability to carry over credits diminishes these burdens over several years.

Filing Deadlines and Important Dates

Taxpayers must note that Form N-323 must be filed with the state income tax return by the applicable deadline. In Hawaii, personal and corporate tax returns are generally due by the 20th of the fourth month after the close of the taxable year (e.g., April 20 for calendar-year taxpayers).

It's crucial to file by this deadline to avoid penalties. Taxpayers should also watch for any state-issued extensions or amendments to standard due dates.

How to Obtain Form N-323

The form can be procured from the Hawaii Department of Taxation website. Alternatively, physical copies may be available at any of the department's offices. To ensure access to the latest version, Rev 2024, check for updated versions or notices on the official site to avoid obsolete filings.

Who Typically Uses Form N-323

Form N-323 is predominantly utilized by:

- Individual taxpayers investing in renewable energy or infrastructure improvements.

- Small to medium-sized businesses engaging in eco-friendly practices or contributing to local economic development through construction and renovation.

- Corporations involved in technological advancements or community betterment projects.

Understanding which taxpayers and businesses commonly use this form can provide insights into its utility and significance within certain industries in Hawaii.

Important Terms Related to Form N-323

- Carryover: Refers to the ability to apply unused credits from prior tax years to current or future liabilities.

- Tax Credit: A rebate or reduction in owed tax, given for participating in approved activities, such as energy conservation.

- Adjusted Tax Liability: The recalculated tax owed after applying eligible credits.

These key terms enhance comprehension of the form's provisions, ensuring accurate completion and filing.