Definition & Meaning

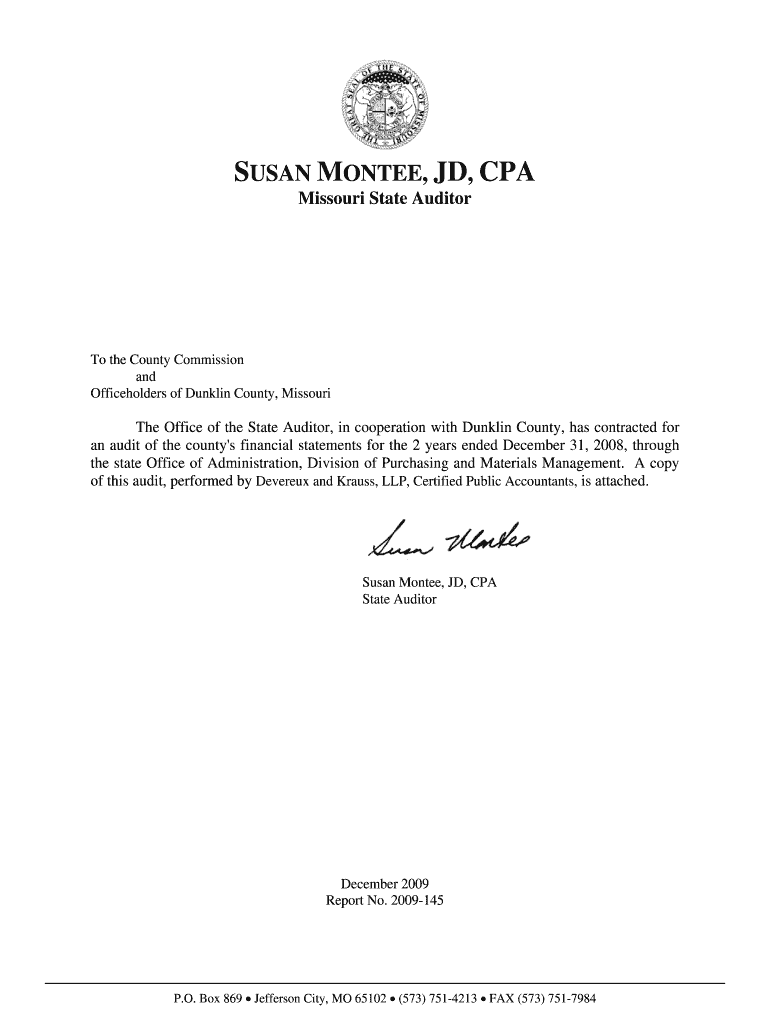

The "Dunklin County Financial Statements 18-29-00-2009-145 - auditor mo" refers to an audit report that examines the financial operations of Dunklin County, Missouri, for specific fiscal years. It includes an independent auditor's opinion which assesses the county's adherence to financial reporting standards and compliance with federal program requirements. This report is crucial for understanding the financial health and management practices of Dunklin County, highlighting areas such as budgetary procedures, internal controls, and legal compliance.

Key Elements of the Financial Statements

The report typically includes several key components such as:

- Balance Sheets: Illustrates the county's assets, liabilities, and fund balances.

- Income Statements: Provides insights into revenues and expenditures.

- Cash Flow Statements: Details cash inflows and outflows over the reporting period.

- Compliance Reports: Audits the county's adherence to financial laws and regulations.

Comprehending these elements helps stakeholders evaluate the financial position and performance of the county during the specified periods.

How to Use the Dunklin County Financial Statements

Understanding how to utilize the report involves several key steps:

- Review the Auditor's Opinion: Start by examining the auditor's opinion for insights into the county's compliance and financial condition.

- Analyze Financial Data: Look at financial statements to assess their budgetary practices, net income, and cash flows.

- Evaluate Compliance: Check for any noted deviations from legal and regulatory frameworks.

- Implement Recommendations: Identify and act on the suggestions made for improving financial practices.

Individuals responsible for fiscal management use these reports to guide budgeting, policy formulations, and operational adjustments.

Steps to Complete the Form

For those involved in preparing or completing the financial documents and audit report, the following steps can guide them:

- Gather Financial Data: Collect all financial data covering the fiscal period.

- Prepare Financial Statements: Draft balance sheets, income, and cash flow statements.

- Compliance Check: Ensure all financial activities adhere to relevant federal and state regulations.

- Submit to Auditor: Provide documents to an independent auditor for examination.

- Review Auditor's Findings: Analyze the auditor's report, focusing on findings and recommendations.

Key Elements of the Audit Report

The audit report contains critical sections such as:

- Summary of Auditor's Findings: Main outcomes and observations from the audit process.

- Recommendations: Suggested improvements for financial practices.

- Compliance Assessment: Evaluation of legal and policy adherence.

- Review of Previous Findings: Analysis of how previous issues have been addressed.

These elements offer a comprehensive view of the financial landscape and guide corrective measures.

Legal Use of the Financial Statements

Legal implications are significant when dealing with these financial statements. They are used to:

- Ensure Compliance: Verify adherence to financial reporting standards and legal mandates.

- Satisfy Transparency Requirements: Provide transparent financial disclosure to stakeholders.

- Identify Legal Risks: Highlight areas of potential legal concern or non-compliance.

Accurate and diligent use of these statements assists in fulfilling regulatory obligations and enhancing fiscal accountability.

State-Specific Rules for Missouri

The audit and reporting requirements for Dunklin County are guided by Missouri state laws and regulations which:

- Define Filing Requirements: Specify deadlines and types of documents required.

- Set Compliance Standards: Establish levels of compliance required by local entities.

- Mandate Audits: Ensure regular independent reviews of financial statements.

Understanding these state-specific demands is essential for compliance and accurate financial reporting.

Examples of Using the Financial Statements

Case studies from Dunklin County's previous audits illustrate the practical application of these reports:

- Budget Reallocation: Adjustments were made based on under-utilized funds identified.

- Operational Changes: Recommendations led to enhanced internal control systems.

- Compliance Corrections: Identified deviations and implemented corrective measures for federal program compliance.

These examples demonstrate the utility of the audit in promoting effective and lawful financial management.

Who Typically Uses the Dunklin County Financial Statements

Various stakeholders benefit from these financial statements, including:

- County Administrators: For strategic planning and budgeting.

- Auditors and Financial Analysts: To evaluate financial performance and compliance.

- State Officials: To ensure adherence to state and federal regulations.

- Public and Taxpayers: To understand fiscal management and accountability.

These users rely on accurate financial statements to make informed decisions and foster transparent governance.