Definition and Purpose of the PIT-CFR

The PIT-CFR, or the Personal Income Tax - Claim for Refund, is a form used for claiming a tax refund on behalf of a deceased taxpayer. This form is essential in ensuring that any overpaid taxes can be rightfully reclaimed by the decedent’s estate or the appointed personal representative. Its purpose is to provide a structured method to handle tax refunds, ensuring compliance with tax laws and aiding in the proper management of a decedent's financial matters. By using the PIT-CFR, claimants can efficiently address any outstanding tax issues, ensure that refunds are processed correctly, and maintain clear financial records for the estate.

How to Obtain the PIT-CFR

Securing the PIT-CFR form is straightforward and can be accomplished through several methods, ensuring accessibility for every taxpayer or representative needing to claim a refund. The Delaware Division of Revenue's official website typically provides direct access to download this form. Physical copies might also be available at local tax offices or by request via mail. It is important to check whether any specific version of the form is required, as state regulations may necessitate using the most recent edition. Understanding these access methods ensures that representatives can start the refund process promptly without unnecessary delays.

Steps to Complete the PIT-CFR

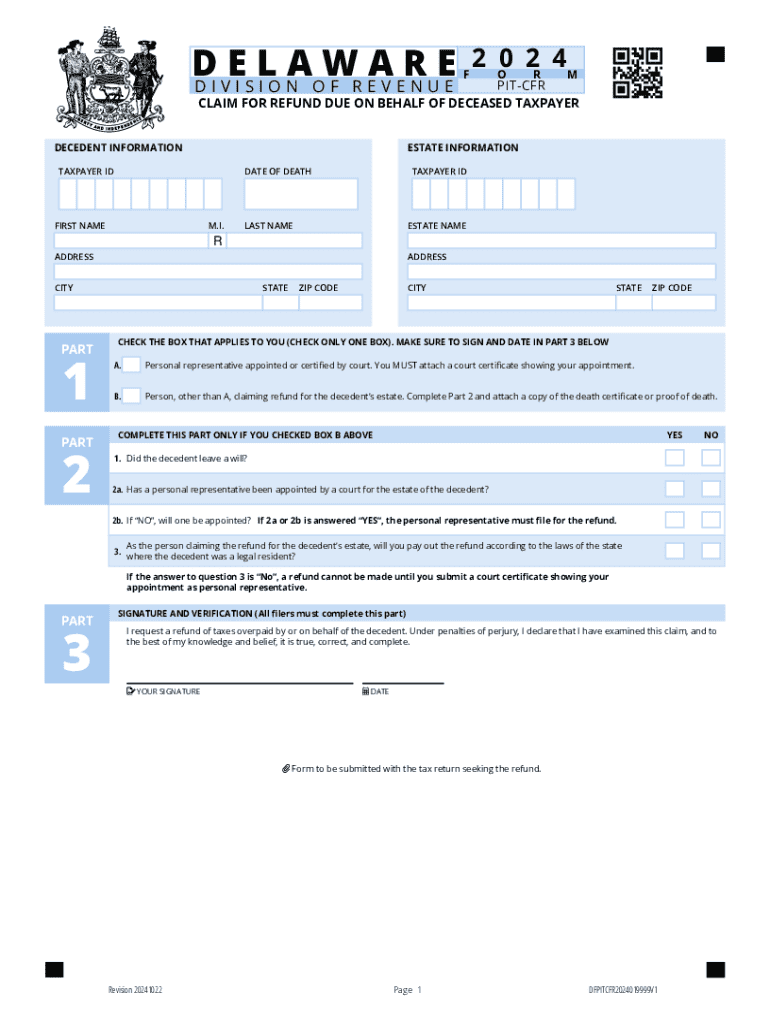

Completing the PIT-CFR involves a series of detailed steps aimed at gathering all necessary information accurately. Here is a structured process to guide you:

-

Enter Decedent Details: Begin by filling out the deceased taxpayer’s full legal name, social security number, and date of death.

-

Provide Estate Information: Include the estate’s name and address if applicable, or stipulate if a personal representative is acting on behalf of the estate.

-

Indicate the Claimant's Identity: Specify whether you are a personal representative, surviving spouse, or another claimant entitled according to legal or document-based authorization.

-

Verification Requirements: Attach necessary verifications such as a death certificate and any required authorization forms that validate the claimant's authority.

-

Submission and Certification: The final step involves reading the declaration statement, signing the document, and confirming that all provided information is accurate under penalty of perjury.

Required Documents for the PIT-CFR

Submitting the PIT-CFR necessitates certain supporting documents to validate the claim. These often include:

- Death Certificate: Essential for verifying the taxpayer’s passing.

- Letters of Administration or Court Appointment: If applicable, these confirm the legal authority of personal representatives.

- Proof of Relationship: For spouses or other close relatives, documentation proving the relationship may be required.

- Prior Year Tax Returns: Offer evidence of overpaid taxes and aid in calculating the refund amount.

The inclusion of these documents helps streamline the review process, reducing the risk of delays or rejections.

Legal Use and Compliance of the PIT-CFR

The PIT-CFR form is governed by specific legal frameworks that determine its correct application and submission. As part of the compliance process, claimants must adhere strictly to state and federal tax laws, including honoring deadlines and accurately presenting all information. For the PIT-CFR, this is governed under both the ESIGN Act and relevant Delaware tax laws to ensure electronic filings are legally valid. Failure to comply with these regulations could result in penalties, denied refunds, or even legal scrutiny.

State-Specific Rules for the PIT-CFR

While the PIT-CFR form is primarily used in Delaware, it is vital to recognize that state-specific rules can influence the process. For instance, Delaware may have distinct filing deadlines different from federal deadlines, which taxpayers must observe religiously to avoid penalties. Understanding variations in state tax regulations is crucial, especially if the decedent had taxable activities or presence in multiple jurisdictions. Familiarizing oneself with these state-specific nuances ensures that the PIT-CFR is filed accurately and on time, effectively minimizing compliance risks.

Filing Deadlines and Important Dates

Filing deadlines for the PIT-CFR can vary, but it generally aligns with the typical tax season timelines. Claimants should be mindful of the following key dates:

- Regular Tax Filing Deadline: Usually April 15, unless extended due to public holidays or administrative decisions.

- Amended Returns: Must be filed within three years from the original filing date or two years from the date of refund payment, whichever is later.

- Estate-Specific Deadlines: Additional deadlines may apply based on the estate's specifics, requiring close attention to ensure timely submission.

Staying aware of these deadlines is vital for safeguarding eligible refunds and avoiding unnecessary legal or financial repercussions.

Software Compatibility and Technology Considerations

Modern tax preparation software, such as TurboTax or QuickBooks, often includes features that support the completion of forms like the PIT-CFR. These platforms can facilitate the calculation of tax refunds and ensure data accuracy by cross-referencing previous tax returns and financial information. It's crucial to verify that the software in use is updated regularly to accommodate tax law changes. For users relying on digital formats, ensuring compatibility with these tools can provide significant time savings and reduce the risk of errors during filing.