Definition and Meaning

Form 990 is a mandatory annual reporting form for tax-exempt organizations in the United States. This form, submitted to the IRS, provides an overview of the organization's finances, activities, governance, and compliance with tax regulations. The primary goal of Form 990 is to ensure transparency and accountability among nonprofit organizations by publicly disclosing valuable information about their operations, which can influence donor decisions and public trust.

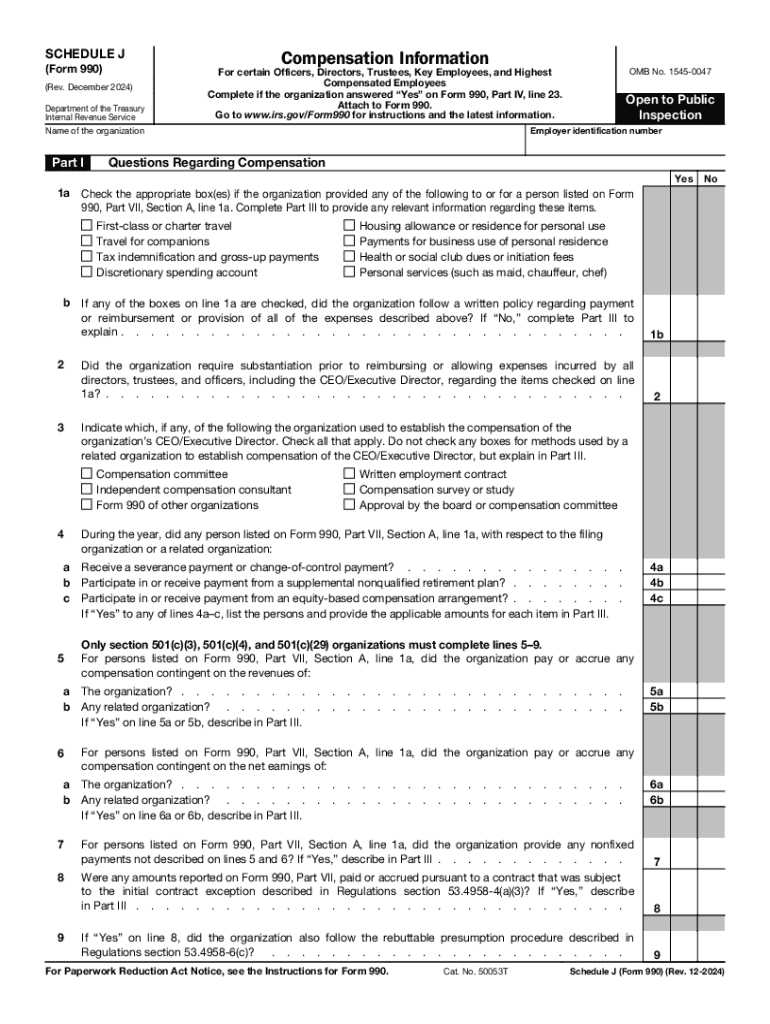

Key Elements of Form 990: A Practical Review

Several important components make up Form 990, each offering different insights into the organization's operations:

- Revenue and Expenses: Details on sources of income and how funds are allocated.

- Board of Directors: Information about the governing body responsible for decision-making.

- Program Service Accomplishments: Details on programs, initiatives, and the impact thereof.

- Compensation: Explanation of compensation for key staff and highest-compensated employees.

- Schedule J: A specific section that outlines executive compensation details and policies.

Steps to Complete the Form 990: A Practical Review

Completing Form 990 involves several critical steps to ensure accuracy and compliance:

- Gather Financial Documents: Collect all necessary financial records, including income statements, balance sheets, and previous tax filings.

- Identify Responsible Parties: Ensure clarity on who is responsible for gathering data and filling out the form.

- Review IRS Instructions: Carefully study the IRS guidelines for the current Form 990 version.

- Complete Relevant Schedules: Fill out additional schedules pertinent to your organization, such as Schedule A or J.

- Review Submission Requirements: Verify all information, ensuring accuracy and completeness.

- Submit by Deadline: File the form with the IRS by the specified deadline, usually the 15th day of the fifth month after the fiscal year-end.

Filing Deadlines and Important Dates

Understanding the timelines for filing Form 990 is crucial to maintain compliance:

- Typical Deadline: The initial deadline is the 15th day of the fifth month after the organization's fiscal year-end. For a calendar year filer, it is typically May 15.

- Extension Options: An automatic three-month extension can be obtained by filing Form 8868, with a potential additional three-month extension if necessary.

Who Typically Uses Form 990: A Practical Review

Form 990 primarily serves as a tool for various key stakeholders:

- Nonprofit Organizations: These include charities, educational institutions, and other 501(c) entities required to disclose financial and operational information.

- Donors and Grantmakers: Individuals and institutions reviewing the credibility and effectiveness of nonprofit organizations.

- Regulatory Bodies: Government agencies ensuring tax compliance and public accountability of charities and nonprofits.

IRS Guidelines

The IRS provides comprehensive instructions to facilitate a correct and efficient filing of Form 990:

- Detailed Line Instructions: A step-by-step guide explaining how to complete each line item in the form.

- Clarifications: Additional information to address common queries and complex situations.

- Schedule Requirements: Specific schedules and forms that must accompany Form 990 depending on varying organization aspects and annual figures.

Legal Use of Form 990: A Practical Review

Form 990 must comply with legal standards established by federal tax laws:

- Disclosure Requirements: Organizations must reveal detailed financial information, including public support, program distributions, and tax-exempt status.

- Public Inspection Requirements: The forms must be made available to members of the public upon request to ensure transparency.

- Compliance and Penalties: Misreporting or non-filing can result in penalties or loss of tax-exempt status.

Penalties for Non-Compliance

Failing to file Form 990 on time or inaccurately can lead to significant repercussions:

- Daily Penalties: Non-filing can incur a daily penalty fee, accumulating until the form is submitted.

- Revocation of Tax-Exempt Status: Repeated failure may result in losing tax-exempt status, impacting donor contributions and contractual obligations.

- Legal Consequences: Persistent negligence may lead to further audits, investigations, or legal actions from the IRS or other regulatory bodies.