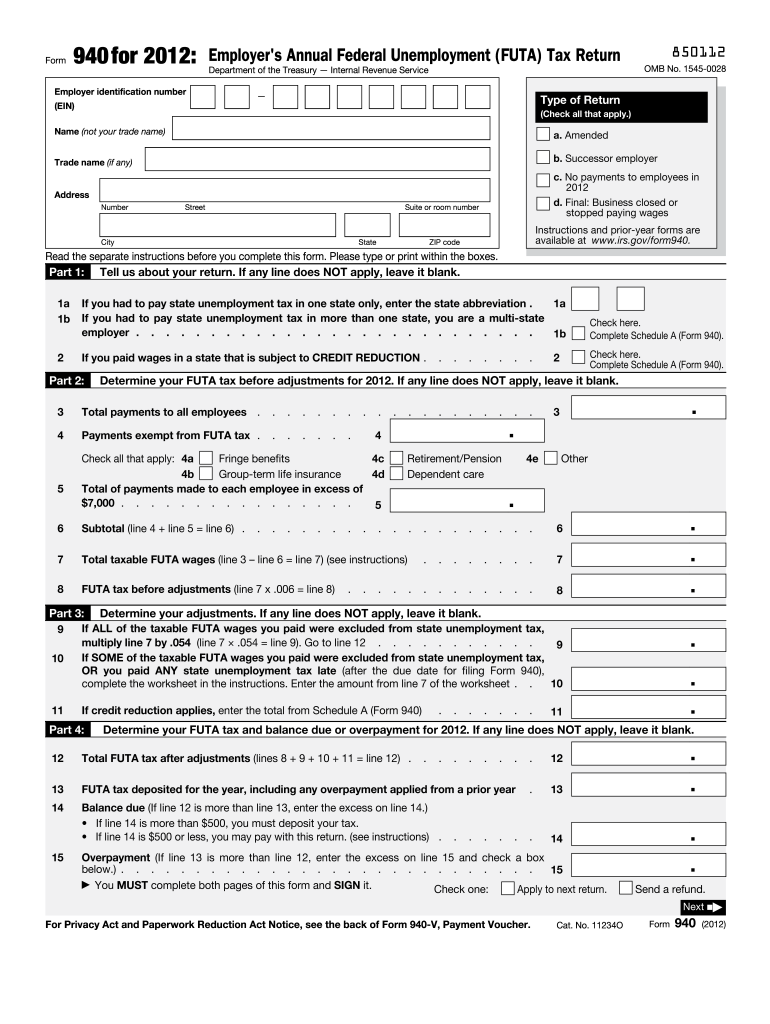

Definition and Purpose of Form 940 for 2012

Form 940 for 2012, officially titled the Employer's Annual Federal Unemployment (FUTA) Tax Return, is a tax form required by the IRS for employers in the United States. This form is used to report and calculate the federal unemployment tax employers owe, based on wages paid to employees within the tax year. Its primary purpose is to fund state workforce agencies, providing unemployment compensation to workers who have lost their jobs.

- The FUTA tax rate for 2012 was 6.0% on the first $7,000 paid to each employee annually. Employers can claim credits for state unemployment taxes paid, usually reducing the effective FUTA rate to 0.6%.

- Form 940 ensures that employers fulfill their obligations to contribute to unemployment funds, supporting unemployed individuals while they seek new employment.

How to Use Form 940 for 2012

Employers need to use Form 940 to sum up their total FUTA tax liability and report any adjustments or amendments. The process entails calculating the total payment subject to FUTA, applying any tax credit reductions, and computing the final tax owed.

Steps to Use Form 940

-

Gather Employee Wage Records: Compile annual gross payments made to each employee. Only the first $7,000 of each employee’s wages is subject to the FUTA tax.

-

Calculate Total Taxable Wages: Deduct any exempt wages from the total to find the taxable amount.

-

Compute FUTA Tax and Adjustments: Use the calculations for the 6% FUTA tax rate and subtract any state tax credits.

-

Complete Additional Adjustments: Account for any discrepancies or corrections that might have accumulated during the year.

How to Obtain Form 940 for 2012

Form 940 for the tax year 2012 can be obtained directly from the IRS website or through software platforms that provide such documents.

- Online Availability: The IRS provides downloadable PDF versions of Form 940. It is essential to ensure you download the correct version for 2012 since there are yearly updates to the form.

- Request by Mail: Employers may also request paper copies from the IRS directly, although this process can take longer.

Steps to Complete Form 940 for 2012

A precise, step-by-step approach is recommended for completing Form 940 to ensure accuracy and compliance.

Detailed Process for Completion

-

Complete Employer Identification Information: Fill out personal and business details at the top of the form.

-

Calculate Adjustments: Determine any adjustments to line 7 using credit reduction states if applicable.

-

List Prior Payments: Report any FUTA payments made throughout the year and apply these against the total tax.

-

Finalize the Calculation: The final section involves adding or subtracting any remaining balance, leading to the net amount due or any potential refunds.

-

Review and Sign: Make sure to check all numbers for accuracy, sign the document, and add the date.

Who Typically Uses Form 940 for 2012

Form 940 primarily applies to employers who pay wages to at least one employee, totaling $1,500 or more within a calendar quarter.

- Corporate Employers: Those structured as corporations are most commonly associated with the filing of this form due to their regular hiring and payroll operations.

- Non-Profit Organizations: Certain non-profits might be exempt but typically must file if engaging in substantial reimbursable employment.

IRS Guidelines and Compliance

Consistent adherence to IRS guidelines is crucial to avoid penalties and ensure the correct completion of Form 940.

Essential IRS Guidelines

- Record Keeping: Employers must maintain thorough payroll records for at least four years to substantiate FUTA tax payments.

- Line Item Instructions: Follow IRS instructions precisely to ensure each section of the form is filled out as per current year rules.

Filing Deadlines and Important Dates

Timely filing of Form 940 is crucial to avoid interest charges or penalties imposed by the IRS.

Key Filing Dates

- Annual Due Date: The general due date for filing is January 31 of the following year. For example, Form 940 for 2012 must be filed by January 31, 2013.

- Quarterly Tax Payments: If an employer's liability is more than $500, quarterly payments are necessary, each due on the last day of the month following the end of the quarter.

Penalties for Non-Compliance

Employers who fail to file accurately or on time may face various penalties from the IRS.

Specific Penalties

- Late Filing Penalties: Up to 5% of the tax due for each month the return is late, not exceeding 25% of the due tax.

- Late Payment Penalties: An added charge of 0.5% of the tax owed for each month unpaid, with a cap, but interest might also apply.

State-Specific Rules for Form 940

Employers should be aware of state rules that might interact with federal requirements on the Form 940.

Considerations

- Credit Reduction States: Some states may have specific reductions affecting credit that employers need to factor into their federal tax calculations.

- State-specific Tax Forms: Coordinating state unemployment tax filings with the federal FUTA return may help prevent questions or discrepancies.

Required Documents and Information

To complete Form 940 correctly, employers typically need several critical documents.

- Employee Wage Statements: Total wages paid, including amounts exempt from FUTA.

- FUTA Tax Deposits Receipts: Any records of electronic or paper payment submissions made under the FUTA system.