Definition and Meaning

The trustee or issuer of your Individual Retirement Arrangement (IRA) plays a crucial role in managing and reporting various aspects of your retirement account. This entity is responsible for maintaining the integrity of the account, ensuring that all transactions comply with IRS regulations. The term "trustee" generally refers to a financial institution or bank that holds the assets in the account, whereas the "issuer" typically pertains to investment firms that offer specific financial products within the IRA.

- Trustee Responsibilities: Includes safeguarding the IRA assets, ensuring compliance with distribution rules, and providing periodic statements.

- Issuer Responsibilities: Involves providing investment options and facilitating transactions such as buys and sells within the IRA.

Understanding who your trustee or issuer is, and their responsibilities can ensure that your retirement plan is managed effectively and meets legal requirements.

How to Use the Trustee or Issuer of Your IRA to Report

Using the trustee or issuer for reporting involves a structured communication process where the institution provides necessary data about your IRA contributions, distributions, and fair market value. Here’s how this typically works:

- Annual Statements: Trustees or issuers send account statements reflecting contributions, distributions, and any earnings accrued during the year.

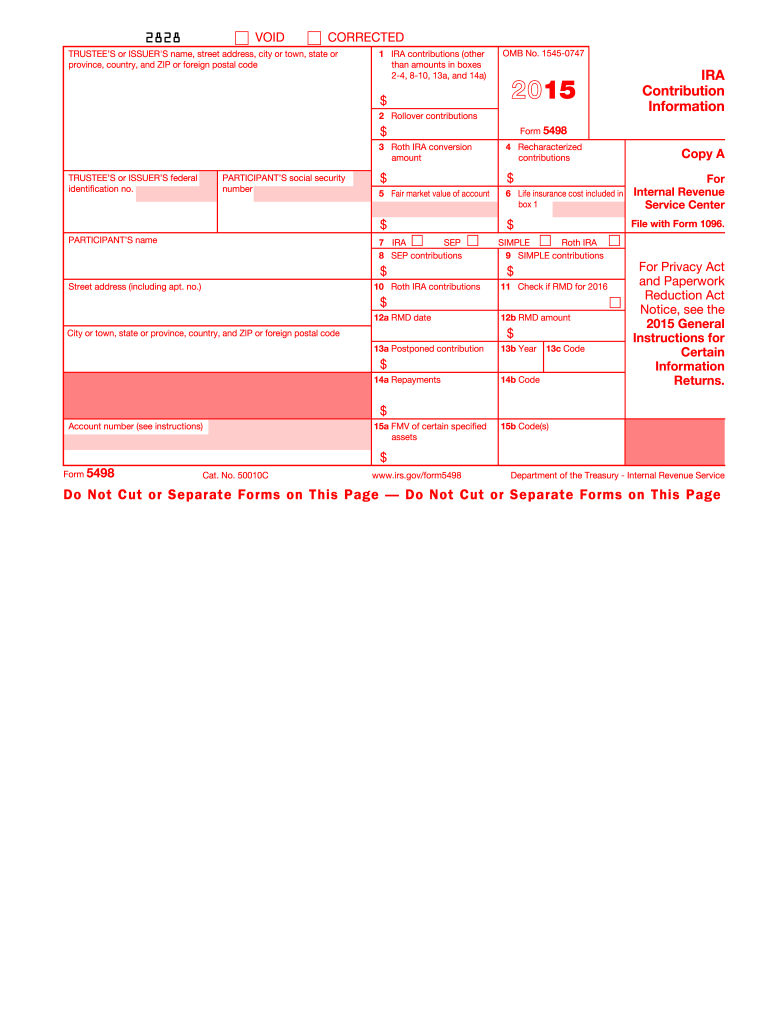

- Form 5498: Issued by the trustee, this form reports contributions to the IRS. It includes details like the type of IRA and the amount contributed.

- Distribution Reporting: If you take money out of your IRA, the trustee reports these distributions to both you and the IRS using Form 1099-R.

These reports enable account holders to ensure their contributions and withdrawals are accurately recorded and comply with tax regulations.

Steps to Complete the Trustee or Issuer of Your IRA to Report

Completing the trustee or issuer report involves several steps to ensure that all information needed by the IRS is accurately prepared:

- Gather Necessary Information: Collect all relevant account details, including contributions, distributions, and account balances.

- Review Forms: Ensure the correctness of the information provided in Form 5498 and Form 1099-R, as these documents carry important tax implications.

- Consult Guidelines: Follow the IRS guidelines for specific reporting requirements concerning different types of IRAs.

- Submission: Ensure that forms are submitted within the required deadlines by confirming these details with your trustee or issuer.

Adhering closely to these steps helps maintain compliance and avoids potential penalties.

Important Terms Related to Trustee or Issuer of Your IRA to Report

Familiarity with key terms associated with IRA reporting is vital for managing your retirement funds efficiently:

- Form 5498: A document the trustee uses to report contributions, rollovers, and conversions.

- Contribution Limits: The maximum amount you can contribute to an IRA annually.

- RMD (Required Minimum Distributions): Withdrawals that must begin at age 73 to avoid IRS penalties.

- Early Distribution Penalty: A 10% additional tax applied to withdrawals made before the age of 59½ without exceptions.

Understanding these terms helps you navigate the complexities of IRA reporting.

Filing Deadlines and Important Dates

Adhering to the filing deadlines is crucial for maintaining compliance with IRS requirements:

- Form 5498 Deadline: Typically due to the IRS by May 31 for the prior year’s contributions.

- RMD Notices: Should be issued by January 31 to inform account holders of their distribution requirements.

- Contributions: Deadline for making contributions to an IRA is April 15 for the prior tax year.

Not meeting these deadlines can result in penalties and complications with the IRS.

Penalties for Non-Compliance

Failure to report IRA transactions accurately can result in significant penalties:

- Excess Contribution Penalty: Imposed when contributions exceed the allowable amount—subject to a 6% tax each year until corrected.

- Failure to Take RMDs: Results in an excise tax of 50% of the required distribution amount not withdrawn.

- Incorrect Reporting: May lead to additional taxes and penalties, including possible IRS audits.

Understanding these consequences emphasizes the importance of diligent reporting and compliance.

Key Elements of the Trustee or Issuer of Your IRA to Report

Several critical components must be present in reports filed by the trustee or issuer of your IRA:

- Account Information: Includes the account number, type of IRA, and responsible financial institution.

- Transaction Details: Comprehensive reporting of contributions, distributions, rollovers, and conversions.

- Compliance with IRS Regulations: Ensures that all reported data aligns with current tax laws and guidelines.

Including these elements ensures thorough and accurate reporting.

IRS Guidelines

The IRS provides specific guidelines for trustees and issuers in managing and reporting IRAs:

- Reporting Standards: Outlines how and when to report contributions and distributions.

- Tax Deduction Eligibility: Details the circumstances under which contributions may be tax-deductible.

- Rollovers and Transfers: Guidelines for tax-free transfers between IRAs and ensuring these transactions are reported correctly.

Following these guidelines helps secure tax advantages and maintains compliance.