Definition & Meaning

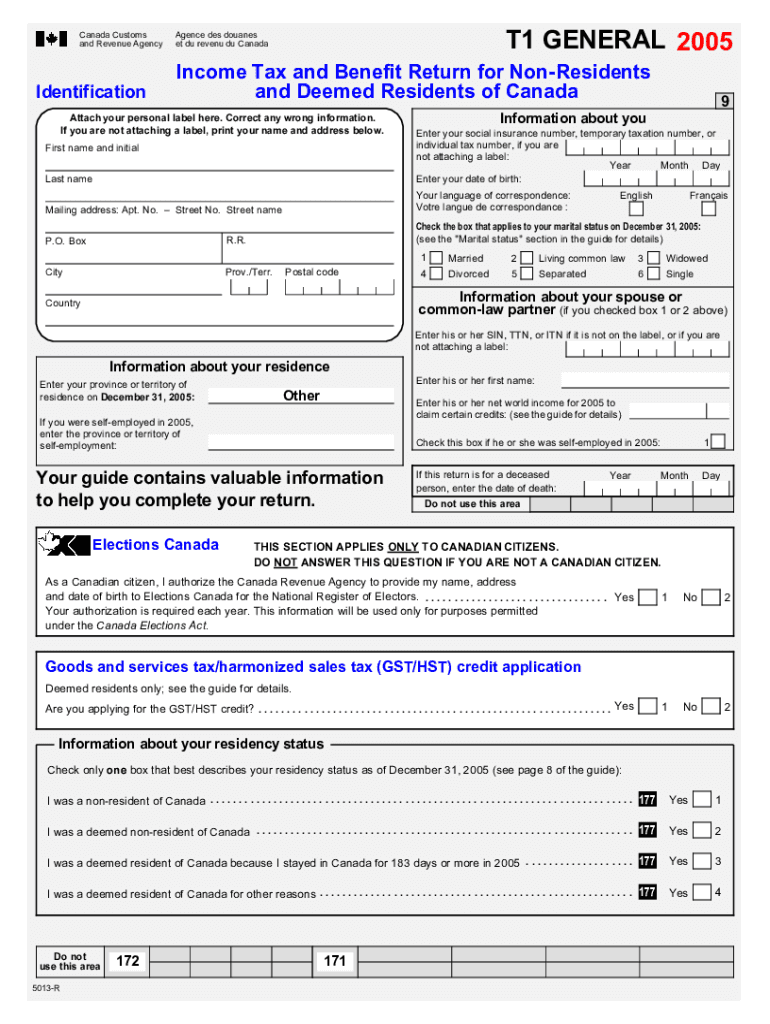

The 5013-R T1 General 2005 - Income Tax Benefit Return for Non-Residents and Deemed Residents of Canada is a tax form issued by the Canada Customs and Revenue Agency. This document is designed to allow individuals who are non-residents or deemed residents of Canada to report their income, claim tax benefits, and declare their residency status for the tax year of 2005. The term “non-resident” refers to individuals who live outside Canada but receive income from Canadian sources, while “deemed residents” are those who are not regularly physically in Canada but meet specific residency criteria set by Canadian law.

Importance of the Form

- Income Reporting: It provides a structured way to disclose various types of income earned that is subject to Canadian tax.

- Benefit Claims: Allows applicants to claim eligible benefits, which is crucial for maximizing financial returns from the Canadian tax system.

- Residency Declaration: Crucially important for determining the tax obligations of individuals concerning their residency status.

Key Elements

The 5013-R T1 General 2005 form is structured to gather detailed information in several essential areas, which include:

- Personal Identification: Name, address, and social insurance number are necessary to uniquely identify the tax filer.

- Residency Status: A declaration of residency status, specifying whether the individual is a non-resident or deemed resident.

- Income Details: A comprehensive section to report all income types such as employment income, dividends, and capital gains from Canadian sources.

- Deductions & Credits: Sections where taxpayers can list eligible deductions and credits to reduce their tax liability.

Deductions You May Claim

- Moving Expenses: If moving to Canada for work, certain costs are deductible.

- Childcare Expenses: Helps reduce taxable income for families.

Steps to Complete the 5013-R T1 General 2005

Filling out the 5013-R T1 General 2005 involves several steps, each important for accurate submission:

- Gather Necessary Information: Collect all income slips, receipts for deductions, and any previous tax documents.

- Complete Personal Information: Fill out the sections requiring personal and residency information accurately.

- Report Income: Use the provided sections to itemize all sources of income received in 2005.

- Calculate Deductions: Enter eligible deductions, which must be backed by documentation.

- Determine Credits: Apply for applicable tax credits that can reduce the payable tax.

- Double Check Entries: Review all entered data for accuracy to avoid processing delays or audits.

- Submit the Form: Choose between mailing the completed form to the designated office or using an electronic submission method if available.

How to Use the Form

Upon acquiring the 5013-R T1, use it to:

- Prepare Tax Documentation: Efficiently gather and organize financial information and supporting documents required for tax filing.

- Assess Tax Liability: Use the form to evaluate annual tax obligations based on the reported income and applicable benefits.

Common Mistakes to Avoid

- Incorrect Residency Status: Ensure accuracy in declaring your residency to prevent tax complications.

- Incomplete Income Reporting: Ensure all Canadian-source income is reported to avoid fines or legal issues.

Who Typically Uses This Form

Typically, this form is used by:

- Expatriates: Canadian citizens working abroad but generating income from Canadian sources.

- Foreign Workers: Individuals residing outside Canada but employed by Canadian companies.

- Seasonal Employees: Those returning to Canada for temporary assignments but do not meet full residency criteria.

Legal Use

The legal use of the 5013-R T1 General 2005 involves using it primarily to fulfill Canadian tax obligations for income earned as a non-resident or a deemed resident.

Compliance Considerations

- Accurate Information: Legally, all information must be correct and backed by documentation.

- Timely Submission: Submission must adhere to Canadian tax deadlines to avoid litigation or penalties.

Filing Deadlines / Important Dates

- Annual Filing: Typically due by the end of April, although specific extensions or deadlines may apply for non-residents.

Consequences of Late Filing

- Penalties and Interest: Late filing may result in financial penalties and interest on unpaid taxes.

Required Documents

To complete the 5013-R T1, you will need:

- Proof of Income: T-Slips and other income statements.

- Expense Receipts: For deductions and credits claimed, such as charity donations or medical expenses.

Document Organization Tips

- Digitize Documents: Keep electronic versions for back-up and easy retrieval.

- Categorize: Group similar documents to streamline the form-filling process.