Definition & Meaning

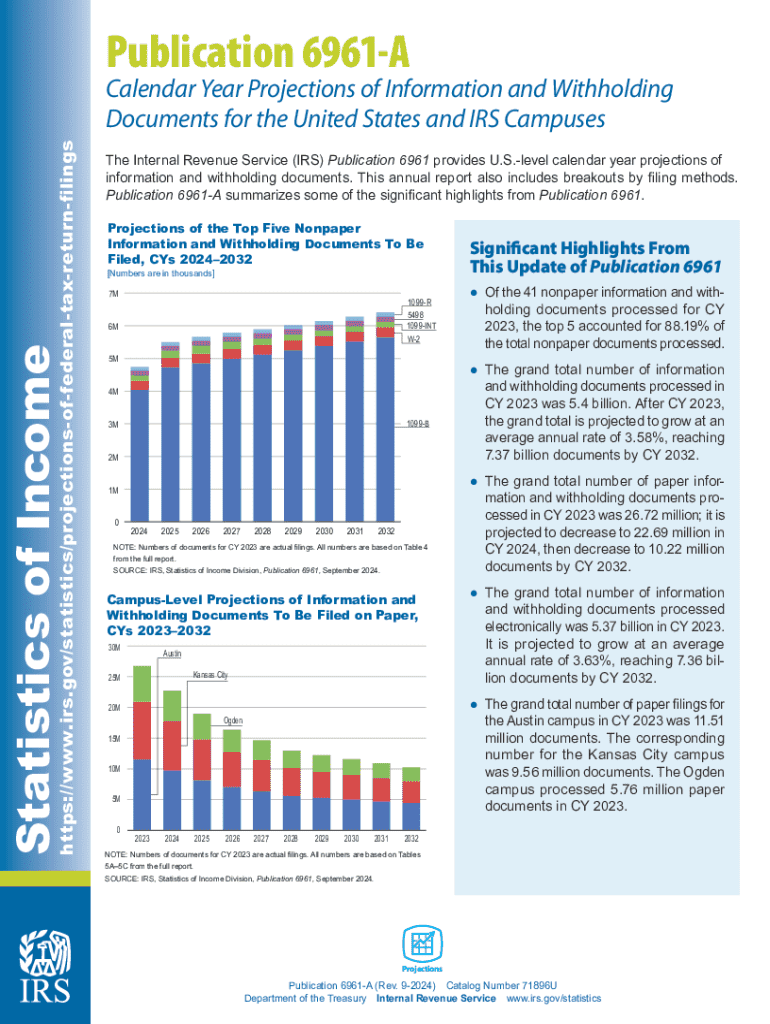

Publication 6961-A (Rev 9-2024) serves as a comprehensive document outlining projections for information and withholding documents filed with the IRS from the calendar years 2024 to 2032. It highlights trends in both nonpaper and paper filings, with a significant emphasis on the anticipated growth of electronic document submissions. This publication provides insights into how document processing is expected to evolve, focusing on both the types and volumes of documents the IRS is projected to handle.

- Projections: The report forecasts the number of documents expected to be processed, indicating a shift from paper to electronic submissions.

- Trends: The publication outlines trends in document types, showcasing which formats are becoming more prevalent.

- IRS Use: Primarily used by the IRS to streamline processing and adapt to changing submission patterns.

How to Use the Publication 6961-A

Utilizing Publication 6961-A effectively requires understanding its structured data and projections. This document can be used by tax professionals and businesses to anticipate changes in document submission processes and requirements, align their internal processes accordingly, and ensure compliance with future IRS expectations.

- Review the Projections: Analyze the types and volumes of documents expected and adjust your document filing practices.

- Adopt E-File Practices: Given the trend towards electronic filings, ensure that systems are in place to facilitate nonpaper submissions.

- Stay Informed: Use the data to anticipate regulatory changes and prepare for increases or declines in filing requirements.

Steps to Complete the Publication 6961-A

Completing the information in Publication 6961-A requires a pragmatic approach:

- Gather Relevant Data: Compile necessary information relevant to withholding and information documents.

- Analyze IRS Guidelines: Ensure understanding of the guidelines related to document projection, particularly for your sector.

- Utilize Data Tools: Employ analytics tools to accurately fill out expected information applicable to your filings.

Key Elements of the Publication 6961-A

Publication 6961-A consists of critical components aimed at delivering comprehensive data:

- Document Types: Identification of major document types and their submission statistics.

- Processing Data: Detailed campus-level data related to the processing of different document types.

- Trend Analysis: Insights into which document types dominate filings and forecasted shifts in submission practices.

IRS Guidelines

The IRS provides guidelines within Publication 6961-A to facilitate a smooth transition from paper to electronic files:

- Compliance: Adhering to these guidelines ensures conformity with IRS standards and helps avoid potential penalties.

- Submissions Standards: Clear understanding of the standards helps businesses align their document processing approaches.

- Adaptation: Emphasis on adaptability to growing reliance on electronic filing methods.

Filing Deadlines / Important Dates

Key filing deadlines and important dates are central to proper use of Publication 6961-A:

- March 31: Final electronic filing due date for most tax documents.

- April 15: Traditional tax deadlines should also be considered for non-electronic filings.

- Adjustments Announcements: Keep abreast of any announcements from the IRS regarding deadline changes or extensions.

Penalties for Non-Compliance

Failure to comply with the guidelines in Publication 6961-A may result in penalties, including:

- Late Filing: Penalties accrue if deadlines are missed without an IRS-approved extension.

- Incorrect Filing: Submission of incorrect or incomplete data can lead to fines.

- Non-Submission: Significant penalties for failure to submit required documents.

Digital vs. Paper Version

The transition from paper to digital submissions is heavily emphasized in Publication 6961-A:

- Digital Advantages: Convenience, faster processing times, and lower error rates are benefits of digital submissions.

- Paper Filings: While still accepted, these are declining and may face extended processing times.

- Adoption Guidance: Recommendations for transitioning from paper to digital to help organizations efficiently manage their document workflows.