Definition & Purpose

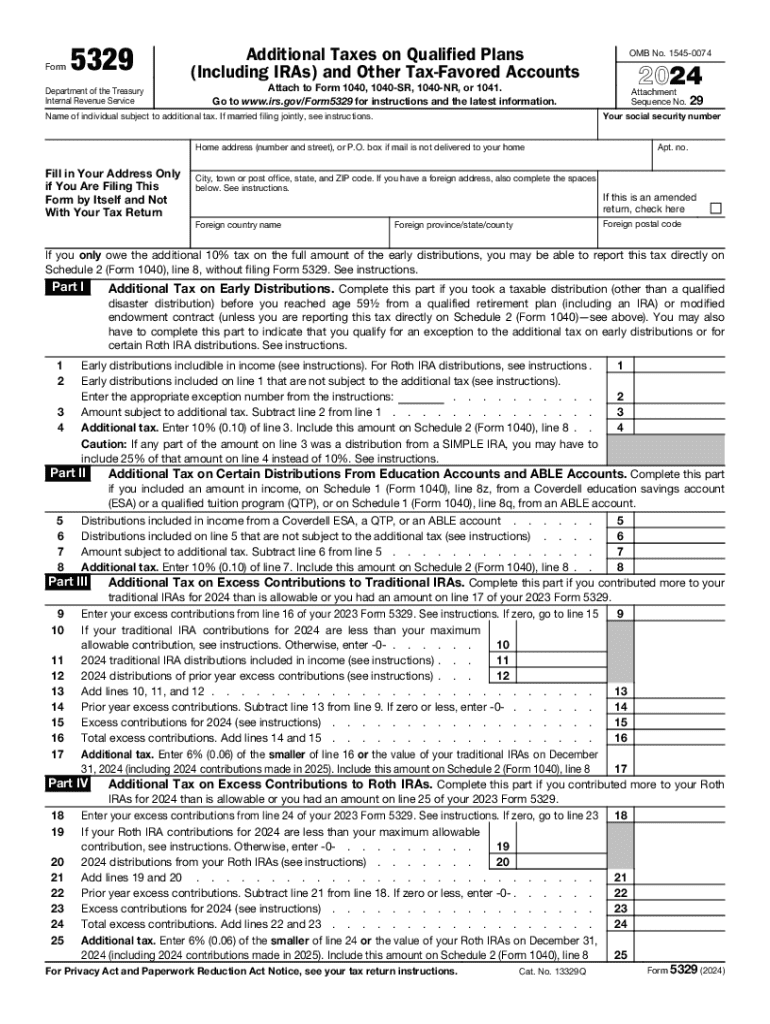

The "2024 Form 5329: Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts" is a form issued by the IRS to facilitate the reporting of additional taxes on retirement accounts like IRAs and other similarly tax-advantaged accounts. It is primarily employed by taxpayers who need to report additional tax liabilities that arise due to early withdrawals, excess contributions, or missed required minimum distributions (RMDs).

Key Functions

- Early Withdrawal Penalties: Users must report additional taxes if they withdraw funds from their retirement accounts before reaching 59 ½ years of age, subject to exceptions like disability or qualified education expenses.

- Excess Contributions: Taxpayers need to declare any contributions that exceed IRS limits for various accounts such as IRAs or 401(k)s.

- Failure to Take RMDs: If minimum distributions are not adequately taken from certain accounts by the IRS-mandated age, the taxpayer faces a 50% penalty on the shortfall.

Steps to Complete the Form

Completing the 2024 Form 5329 involves several precise steps. Accurate completion is necessary to avoid penalties.

-

Personal Information: Enter personal details like your name, Social Security number, and filing status.

-

Section I – Additional Tax on Early Distributions: Here, indicate any early distributions subject to additional taxes.

- Example: A taxpayer withdrawing from a Roth IRA before age 59 ½ would report this here.

-

Section II – Excess Contributions: Report any excess contributions from various tax-advantaged accounts.

- Note: Corrective measures, such as withdrawing the excess amount, should be taken to avoid enduring penalties.

-

Section III – Tax Due on Failure to Take RMDs: Calculate and report penalties if required minimum distributions were not taken.

-

Summarize and Calculate Total: Combine the relevant sections to find total additional taxes owed and transfer them to your primary tax return.

IRS Guidelines

The IRS provides comprehensive guidance on using Form 5329, ensuring individuals are informed of the rules and exceptions about retirement accounts.

Notable IRS Provisions:

- Exceptions to Early Withdrawal Penalties: Recognize scenarios like permanent disability or substantial medical expenses that can qualify for penalty waivers.

- Contribution Limits: Ensure adherence to yearly limit changes for account contributions to avoid excess contribution penalties.

Filing Deadlines

Key Dates:

- Tax Filing Deadline: Typically, April 15 for most taxpayers.

- Extension Availability: Can apply for a filing extension giving until October 15, though any taxes due should still be paid by the original date to avoid interest and penalties.

Required Documents

Being organized with the necessary documentation can streamline the form submission process.

- Account Statements: Provide detailed transaction records from each retirement account.

- Proof of Exceptions: Documentation to substantiate eligibility for exceptions from penalties, such as medical expense receipts or disability awards.

How to Obtain the Form

Obtaining Form 5329 can be done through several channels:

- IRS Website: Directly download a PDF version from the IRS official website.

- Tax Software: Most tax preparation software like TurboTax or QuickBooks offers direct access to Form 5329.

- Professional Assistance: Many tax advisors and accounting professionals can provide the form and help in its completion.

Penalties for Non-Compliance

Non-compliance with the requirements of Form 5329 can result in significant penalties:

Applicable Penalties:

- Early Withdrawal Errors: A 10% tax penalty on unreported early distributions.

- Excess Contribution Penalties: Annual 6% tax until the excess amount is corrected.

- Missed RMD Penalties: Substantial 50% tax on any undistributed required minimums.

Taxpayer Scenarios

Understanding varied taxpayer scenarios can assist in proper form completion:

Common Scenarios:

- Self-Employed Individuals: Often manage multiple retirement plans, making them more susceptible to incorrect excess contributions.

- Retirees: Primarily need to be mindful of RMDs to evade hefty fines.

- Students: Using retirement savings for educational expenses may have exceptions, which should be communicated accurately.

Digital vs. Paper Version

Utilizing the correct version can facilitate compliance and ease.

Considerations:

- Digital Version: Offers convenience with cloud storage and easier sharing, and supports e-filing through tax software.

- Paper Version: May be required for manual filing or records kept with non-digital systems, but ensure timely mailing to avoid late penalties.