Definition and Meaning of Form 941-X

Form 941-X, also known as the Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund, serves a critical role for employers who need to make corrections to their originally submitted IRS Form 941. This form is utilized to address discrepancies such as overreporting or underreporting of taxes, wages, withholdings, and corrections to previously filed quarters. By submitting Form 941-X, employers can correct their filed data to reflect accurate federal tax responsibilities and claim any potential refunds or adjustments needed.

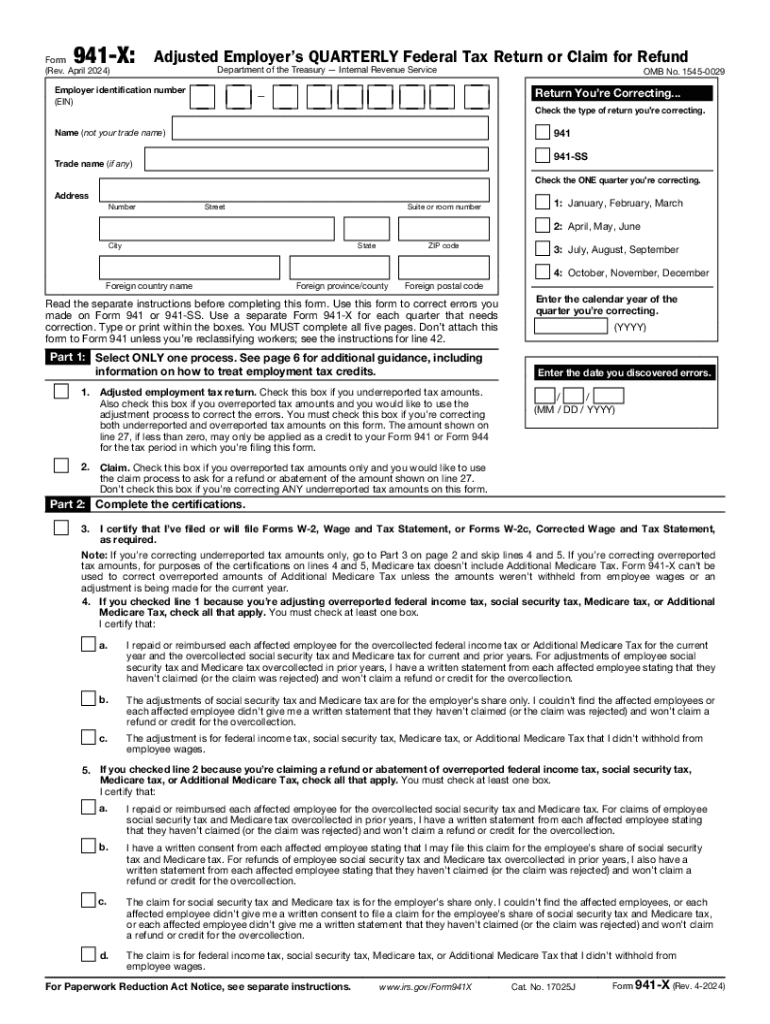

Obtaining Form 941-X (Rev April 2024)

Employers can access the Form 941-X through several straightforward channels. Primarily, it can be downloaded directly from the IRS website. This updated version is also available through tax software programs like TurboTax and QuickBooks, which often include the most current tax forms. Additionally, printed versions are obtainable from IRS office locations, ensuring diverse access methods for different user preferences.

Steps to Complete Form 941-X

-

Review Original Submission: Start by reviewing the previously filed Form 941 to identify specific mistakes or adjustments needed.

-

Fill Out Identification Information: Include employer details such as name, address, and Employer Identification Number (EIN).

-

Detail the Adjustments: Utilize the appropriate lines to describe corrections for wages, tax amounts, or withholdings.

-

Provide Supporting Documentation: Attach necessary documents that substantiate the claims and corrections made.

-

Certify and Sign: Ensure the form is signed by an authorized individual, confirming the accuracy of the adjustments provided.

-

Submission: Decide between mailing the document to the IRS or submitting it electronically via supported software.

Why Use Form 941-X

Using Form 941-X is vital for maintaining compliance with federal tax regulations. Employers must correct any errors to avoid penalties, interest, or other legal actions from the IRS. Accurate adjustments can result in significant financial recoveries, such as taking advantage of eligible tax credits or receiving refunds due to overpaid taxes. This ensures that both past and future tax filings are based on precise data, reflecting true financial statuses.

Typical Users of Form 941-X

The primary users of Form 941-X include employers, payroll personnel, and tax professionals responsible for managing payroll taxes for businesses. This form is essential for correcting reported earnings and taxes, especially for entities with complex payrolls that might experience frequent changes or errors in reporting. It is also frequently used by organizations shifting their payroll service providers or those undergoing audits which uncover past discrepancies.

Key Elements of Form 941-X

- Identification Information: Accurate completion of employer details, including the tax period being corrected.

- Error Descriptions: Detailed explanation of discrepancies and the reasons for adjustments.

- Adjusted Figures: New, accurate calculations distinct from the originally filed amounts.

- Certifications: Signed declarations affirming the revised information's accuracy.

- Supporting Documents: Necessary for validating any claims or corrections, such as copies of employee payroll records or prior tax documents.

Filing Deadlines and Important Dates

While there are no strict deadlines for submitting Form 941-X, it is generally advisable to file it as soon as an error is identified. Employers looking to claim a refund must file the form within three years of the original filing date or within two years of the payment of the tax, whichever is later. This ensures that corrections are made promptly and potential refunds or credits are secured.

Form Submission Methods

Form 941-X can be submitted to the IRS either by mail or electronically. Mailing the form involves sending it to the designated IRS address for the employer's location, while electronic submissions can be completed using IRS-approved e-file providers or compatible tax preparation software. Electronic submissions are recommended for their efficiency and security.

Penalties for Non-Compliance

Failure to file Form 941-X when necessary can lead to significant penalties. Employers may incur fines for incorrect tax filings or face heightened scrutiny from the IRS during audits. Additionally, not correcting overreported taxes could result in missed opportunities for refunds. Employers are encouraged to proactively submit this form whenever payroll discrepancies are discovered to maintain compliance and avoid unnecessary penalties.