Definition & Meaning

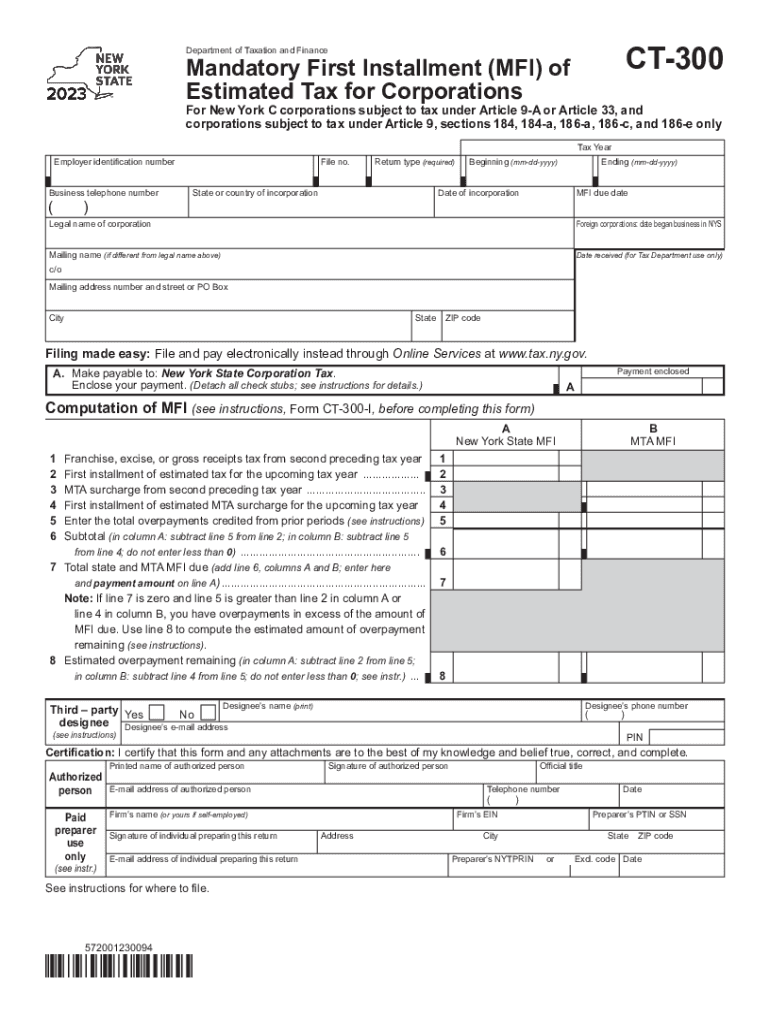

The Mandatory First Installment (MFI) of Estimated Tax for Corporations refers to an initial tax payment required from certain corporations to prepay a portion of their state or federal tax liabilities. This installment serves as a proactive financial obligation ensuring that corporations meet a portion of their tax responsibilities throughout the fiscal year. The MFI is computed using a percentage of a corporation's prior year tax liability or an estimated amount based on current projections. The goal is to align the tax payments with actual earnings, thus minimizing the risk of underpayment.

Steps to Complete the Mandatory First Installment (MFI)

-

Determine Eligibility: Verify if your corporation meets the criterion for MFI payment. Typically, corporations with significant tax liabilities in the previous year are required to make this prepayment.

-

Calculate the MFI Amount: Use either the prior year's tax liability or current year's projections. Tools like tax software can aid in the precise calculation by considering all applicable tax factors.

-

Prepare the Required Documentation: Gather necessary financial records, business identification numbers, and any official notices received regarding tax obligations.

-

Submit Payment: Choose an accepted method – online submission through the official tax portal, mailing a check with appropriate documentation, or in-person registration where applicable.

-

Verify Submission: Obtain confirmation from the respective tax authority for future records and compliance verification.

Key Elements of the MFI

-

Payment Structures: Corporations must be aware of different payment structures such as percentage-based obligations versus fixed amounts determined by the state or IRS.

-

Financial Impact: Understanding how the MFI impacts cash flow helps in strategic financial planning throughout the fiscal year.

-

Compliance Requirements: Adhering to submission guidelines and retaining records ensures that corporations remain compliant and avoid penalties.

IRS Guidelines

The IRS mandates the MFI for corporations by providing clear instructions on calculating, reporting, and paying estimated taxes. These guidelines often include:

-

Safe Harbor Provisions: Protects corporations from penalties if they have paid a substantial percentage of their total tax liability.

-

Quarterly Payment Instructions: Specifying the timeline for submitting payments across four quarters to smooth the tax paying process.

-

Use of EFTPS: Encourages the use of the Electronic Federal Tax Payment System for secure payment processing.

Filing Deadlines / Important Dates

-

Quarterly Deadlines: Corporations must adhere to specific due dates, often aligning with the fiscal calendar quarters, to prepay installments accurately.

-

Annual Reconciliation: At the end of the fiscal year, a reconciliation process evaluates if the previous MFI payments align with the actual tax liability, allowing adjustments or refunds.

-

State-Specific Requirements: States may set varied filing deadlines, demanding additional attention to local jurisdiction guidelines.

Who Typically Uses the MFI

The MFI is predominantly used by:

-

Large Corporations: Entities with substantial annual income, making consistent payments necessary to meet tax obligations.

-

S Corporations and C Corporations: These corporate structures often meet the threshold requiring MFI due to their revenue size and state-specific obligations.

-

Businesses with Seasonal Income: Estimates allow staggered payments adjusted periodically to reflect actual income patterns.

Penalties for Non-Compliance

Corporations that miss MFI deadlines or underpay face potential fines and increased scrutiny from tax authorities. Penalties typically involve:

-

Interest Charges: Applying interest on underpaid amounts from the due date until payment is made.

-

Fixed Penalties: Certain states impose fixed fines for non-compliance, increasing operational costs unnecessarily.

-

Increased Audit Risk: Non-compliant businesses may attract closer inspections and audits by tax authorities.

Digital vs. Paper Version

-

Electronic Filing Advantages: Offers speed, real-time updates, and minimized errors through automated checks, essential for modern tax management.

-

Paper Form Use: While less common, paper filings can cater to businesses with limited digital access, albeit with higher risk of human errors and longer processing time.

Important Terms Related to MFI

Understanding key concepts is crucial for effective MFI management, such as:

-

Estimated Tax Base: The foundational amount from which installments are calculated.

-

Overpayment Credits: Any excess from previous payments available for credit against future liabilities.

-

Submission Authentication: Verifying identity through secure mechanisms, especially when digital portals are used.

Software Compatibility

Corporations often rely on software like TurboTax and QuickBooks for computations and processing. These platforms provide:

-

Automated Calculations: Ensuring accurate tax estimations based on entered data.

-

Filing Support: Streamlining the electronic filing process by integrating with secure payment systems.

-

Recordkeeping: Facilitating comprehensive documentation necessary for compliance and audit purposes.